F & M Bank Corp. Announces Branch Closures, First Quarter Earnings And First Quarter Dividend

F & M Bank Corp. (OTCQX:FMBM), parent company of Farmers & Merchants Bank, announces three branch closures, its financial results for the first quarter ending March 31, 2019 and first quarter dividend to shareholders.

F&M Bank Corp. has worked diligently during the COVID-19 global pandemic to meet the needs of our customers by providing Paycheck Protection Plan (PPP) loans through the Small Business Administration, processing loan deferrals and continuing to operate our core services while practicing social distancing. As of April 27, 2020, we have processed 531 PPP loans for a total of $51.5 million, processed 683 deferrals and continued to operate our branches in a drive-thru only capacity daily, with courier pickup and by appointment account opening.

We are far from seeing an end to the effects of the pandemic on our businesses and economy, however the efforts of our management and staff to support our communities has been tremendous and is a testament to community banking. This includes an early initiative to fund $100,000 in small business grant programs to support our community in the Shenandoah Valley managing through the impacts of COVID-19. .

As part of our ongoing strategic efforts to reduce overhead, we have made the difficult decision to consolidate three of our branch locations in Craigsville, Grottoes and Luray, VA. While these physical locations will close on July 31, 2020, client accounts will remain supported at neighboring offices. Impacted employees from these branches will be offered comparable positions within the organization.

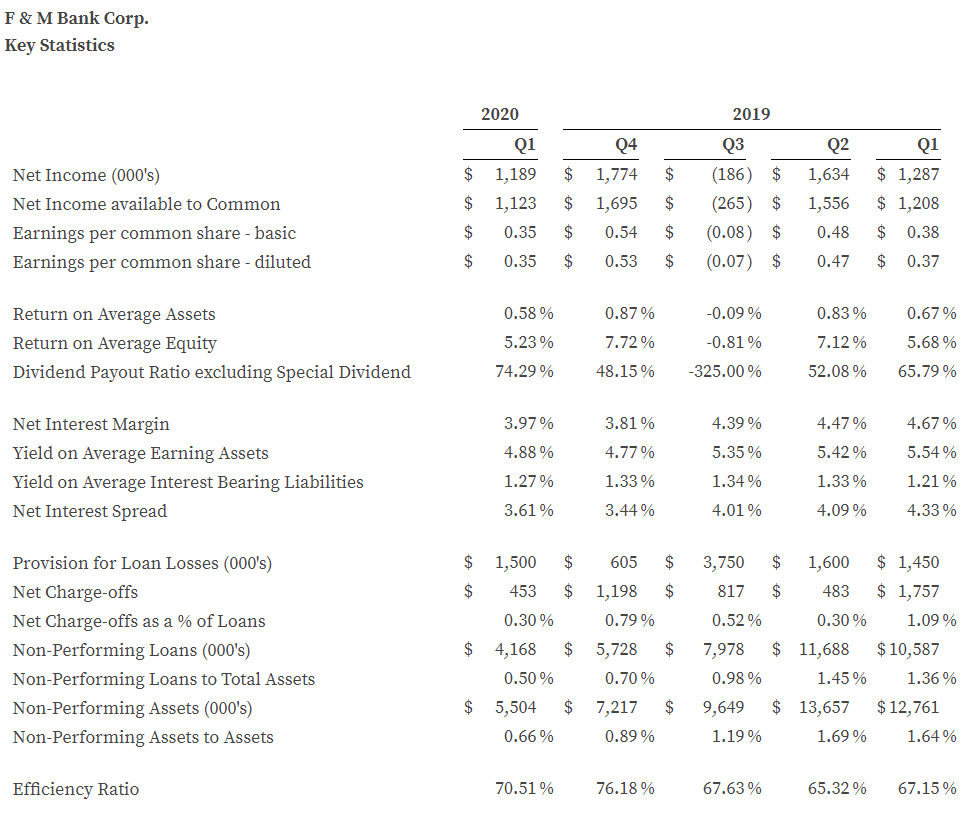

Selected financial highlights for the quarter include:

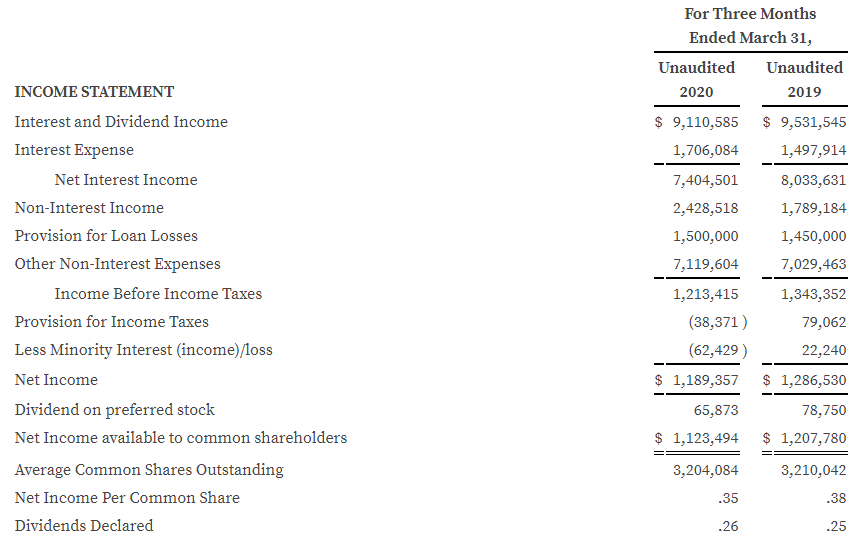

- Net income of $1.19 million.

- Net interest margin of 3.97%.

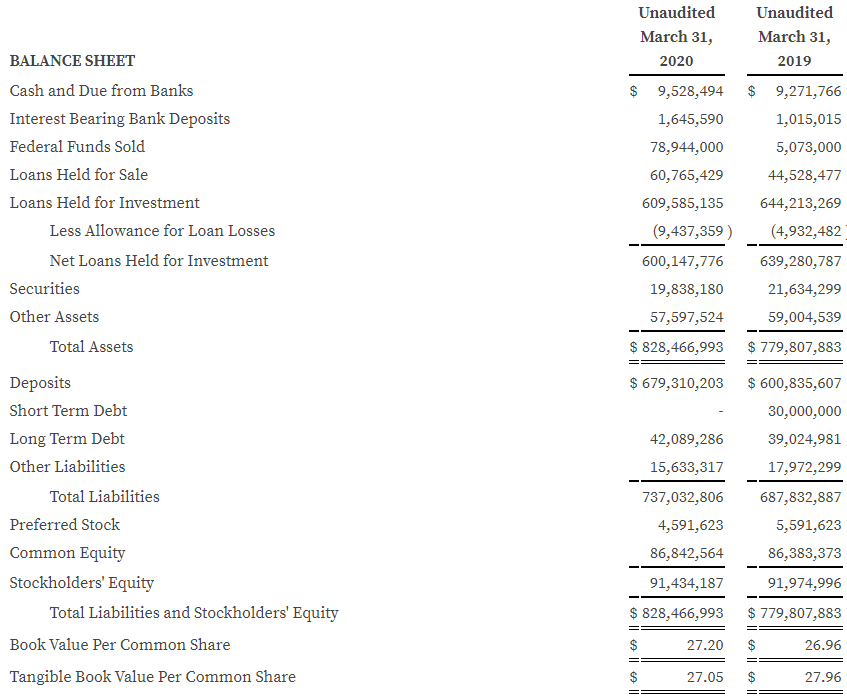

- Loans held for investment increased $6.2 million for the quarter

- Total deposits increased $37.6 million and $78.5 million, respectively for the quarter and for the trailing 12 months.

- Nonperforming loans decreased to 0.50% at the end of the quarter from 0.70% of total assets on 12/31/2019 and 1.36% on 6/30/2019.

Mark Hanna, President, commented “Our first quarter earnings of $1.19 million were weighed down by an increase in our provision for loan losses due to economic factors related to COVID-19. These results are similar to first quarter of 2019, despite the sale of a portion of our dealer portfolio and a correction to the expensing of dealer commissions. Our net interest margin of 3.97% shows a historical decline but still remains strong in the current environment. Our balance sheet liquidity has increased significantly over the last two quarters and we are implementing strategic solutions to leverage these assets.”

Mr. Hanna continued, ‘Nonperforming loans have improved dramatically over prior year, decreasing $6.4 million since first quarter of 2019, and also decreasing $1.6 million since year end 2019. Efforts continue to maintain our goal of 0.50% of total assets.

On April 24, 2020 our Board of Directors declared a first quarter dividend of $.26 per share to common shareholders. Based on our most recent trade price of $17.25 per share this constitutes a 6.03% yield on an annualized basis. The dividend will be paid on June 1, 2020, to shareholders of record as of May 15, 2020.”

Highlights of our financial performance are included below.

F & M Bank Corp. is an independent, locally-owned, financial holding company, offering a full range of financial services, through its subsidiary, Farmers & Merchants Bank’s fourteen banking offices in Rockingham, Shenandoah, Page and Augusta Counties, Virginia. The Bank also provides additional services through a loan production office located in Penn Laird, VA and through its subsidiaries, F&M Mortgage and VSTitle, both of which are located in Harrisonburg, VA. Additional information may be found by contacting us on the internet at www.fmbankva.com or by calling (540) 896-8941.

This press release may contain “forward-looking statements” as defined by federal securities laws, which may involve significant risks and uncertainties. These statements address issues that involve risks, uncertainties, estimates and assumptions made by management, and actual results could differ materially from the results contemplated by these forward-looking statements. Factors that could have a material adverse effect on our operations and future prospects include, but are not limited to, changes in interest rates, general economic conditions, legislative and regulatory policies, and a variety of other matters. Other risk factors are detailed from time to time in our Securities and Exchange Commission filings. Readers should consider these risks and uncertainties in evaluating forward-looking statements and should not place undue reliance on such statements. We undertake no obligation to update these statement

s following the date of this press release.

- The net interest margin is calculated by dividing tax equivalent net interest income by total average earning assets. Tax equivalent interest income is calculated by grossing up interest income for the amounts that are nontaxable (i.e. municipal securities and loan income) then subtracting interest expense. The tax rate utilized is 21%. The Company’s net interest margin is a common measure used by the financial service industry to determine how profitable earning assets are funded. Because the Company earns nontaxable interest income from municipal loans and securities, net interest income for the ratio is calculated on a tax equivalent basis as described above.

- The efficiency ratio is not a measurement under accounting principles generally accepted in the United States. The efficiency ratio is a common measure used by the financial service industry to determine operating efficiency. It is calculated by dividing non-interest expense by the sum of tax equivalent net interest income and non-interest income excluding gains and losses on the investments portfolio and Other Real Estate Owned. The Company calculates this ratio in order to evaluate how efficiently it utilizes its operating structure to create income. An increase in the ratio from period to period indicates the Company is losing a greater percentage of its income to expenses.

CONTACT: Carrie Comer, EVP/Chief Financial Officer; 540-896-8941 or ccomer@fmbankva.com

SOURCE: F&M Bank Corp