Timberville, VA (June 30, 2025) — F&M Bank has announced a strategic realignment of its leadership team, positioning the organization for its next phase of growth and enhanced customer experience.

Building on the success of a multi-year operational transformation, the bank has experienced strong financial performance and improved efficiencies across its business lines. This leadership evolution is the next step in ensuring that F&M remains well positioned to meet the needs of its customers, communities, and shareholders, and drive growth.

“These changes are about playing to our strengths, and we’re fortunate to have depth and breadth of leadership across the organization to help propel F&M forward,” said Mike Wilkerson, CEO of F&M Bank. “Over the past two years, we’ve built a solid operating foundation, and this realignment allows us to better leverage our leadership team’s talents to accelerate our momentum and long-term growth.”

Leadership Changes Include:

Barton Black, President, will expand his responsibilities to include oversight of Retail Banking, in addition to his current focus on Operations, Automotive Dealer Finance, and Risk Management.

Lisa Campbell, Chief Financial Officer, will add oversight of non-interest income lines of business, including Mortgage, Title, and Wealth Management, alongside her finance responsibilities.

Paul Eberly, formerly Chief Development Officer, transitions to Chief Lending Officer, leading Commercial and Agricultural loan and deposit growth across the bank’s footprint.

Charles Driest, formerly Chief Experience Officer, becomes Chief Operations Officer, overseeing Deposit and Loan Operations, Marketing, and Technology.

John Sargent, formerly Northern Market Executive, steps into the role of Retail Banking Director, responsible for the bank’s retail network and customer growth strategies.

Jonathan Reimer has been promoted to Market Executive, North Shenandoah Valley, leading commercial business development and community engagement in the Winchester/Frederick market.

“This team has already delivered measurable results, and I’m confident these moves will strengthen our ability to serve customers and deepen our community impact,” added Wilkerson.

F&M Bank remains committed to delivering personalized, community-focused financial services across the Shenandoah Valley and beyond.

About F&M Bank

F&M Bank, headquartered in Timberville, Virginia, has been serving the Shenandoah Valley since 1908. With a network of branches and a long history of community partnership, F&M Bank remains committed to helping individuals and businesses grow and thrive.

https://www.fmbankva.com/wp-content/uploads/2025/06/Screenshot-2025-06-30-093427.jpg396641Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2025-06-30 08:56:082025-06-30 09:35:48F&M Bank Announces Organizational Leadership Realignment to Support Continued Growth

Celero Commerce is pleased to announce Farmers & Merchants (F&M) Bank in Virginia as the recipient of the East Coast Region Partner of the Year award at our inaugural Celero Partner Awards.

The company held our first Celero Partner Awards on Feb. 14 and recognized bank partners in the West, East, and Central regions. F&M Bank has demonstrated a strong and collaborative partnership with Celero over the past five years, making them an obvious choice for this prestigious award.

F&M Bank’s understanding of the value of merchant solutions and commitment to educating their team on Celero’s offerings have contributed to significant non-interest income growth. They consistently identify and pursue quality opportunities, increasing revenue for both organizations.

They enhance Celero’s market presence with co-created campaigns, internal employee recognition programs, and strategic integration of Celero’s sales team into bank-hosted events. Notably, they facilitated introductions between our Celero Account Executive and every branch within their network, strengthening our presence and credibility in the community as a trusted resource for merchant solutions.

“F&M Bank is honored to receive this recognition from Celero. Our partnership has allowed us to provide innovative merchant solutions that empower small businesses in our community. By working closely with Celero’s team, we’ve been able to enhance our offerings, drive growth, and support the entrepreneurial spirit that fuels our local economy. We look forward to building on this success and continuing to deliver meaningful solutions to our business customers” said John Sargent, Senior Vice President at F&M Bank.

“We have valued our partnership with Mike Wilkerson and the entire F&M VA team,” said Jacqueline Porthouse, Vice President of Merchant Sales, Financial Institution Channel at Celero. “Their community first approach to banking paired with their passion for Main Street America small and medium-sized businesses has created an ideal alignment with Celero. I have been welcomed into the F&M family with open arms and look forward to our relationship growing in the future to better support the Shenandoah Valley.”

F&M Bank’s dedication to growth, collaboration, and innovation has distinguished them as a leader within our financial institution partnership program. We are honored to recognize F&M Bank as our East Coast Region Partner of the Year and look forward to our continued collaboration.

About Celero Commerce

Headquartered in Nashville, Celero Commerce is a full-service, integrated electronic commerce solutions provider powered by leading-edge technology, strategic partnerships, and business intelligence. Celero offers small and medium-sized businesses payment processing services, business management software, and data intelligence, empowering them to drive growth and profitability. Celero is a top-ten non-bank processor of electronic payment transactions in the world. Visit https://www.celerocommerce.com/ to learn more.

About F&M Bank

F&M Bank Corp. (OTCQX: FMBM) proudly remains the only publicly traded organization based in Rockingham County, VA, and since 1908, has served the Shenandoah Valley through its banking subsidiary F&M Bank, with full-service branches and a wide variety of financial services, including home loans through F&M Mortgage, and real estate settlement services and title insurance through VSTitle. Both individuals and businesses find the organization’s local decision-making and up-to-date technology provide the kind of responsive, knowledgeable, and reliable service that only a progressive community bank can.

https://www.fmbankva.com/wp-content/uploads/2025/03/Celero-Partner-of-the-Year.jpeg16411320Jacob Mowry/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgJacob Mowry2025-03-04 11:25:102025-03-04 11:28:05Celero Recognizes F&M Bank as East Coast Region Partner of the Year

[Timberville, VA] – [December 3, 2024] – At F&M Bank, #GivingTuesday is more than just a day—it’s a reflection of our values and commitment to building stronger communities. This global movement, celebrated annually on the Tuesday after Thanksgiving, inspires people and organizations to transform their communities through generosity, collaboration, and collective impact.

Guided by our brand pillars of sustenance, security, and enrichment, F&M Bank is proud to participate in Giving Tuesday by supporting three exceptional local nonprofits:

Each of these organizations champions community needs across our market area, embodying the true spirit of Giving Tuesday. Their dedication to serving others mirrors our own commitment to fostering stronger, more vibrant communities.

“We are incredibly grateful to our team members for nominating these impactful organizations,” said Holly Thorne, Director of Marketing. “The work these nonprofits do changes lives, and we are honored to support their missions.”

F&M Bank encourages others to join us in celebrating Giving Tuesday by giving back to the organizations that make our communities thrive. Together, we can continue growing stronger communities.

https://www.fmbankva.com/wp-content/uploads/2024/12/stacked-color.png10801080Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2024-12-03 16:10:192024-12-03 16:13:28F&M Bank Joins the Global #GivingTuesday Movement to Support Local Nonprofits

Karen and Amanda stand out among women in community banking

Timberville, VA, October 30, 2024 – F&M Bank announced today that Karen Rose and Amanda Hensley were named recipients of the 2024 Banking on Brilliance Awards, powered by KlariVis.

The Banking on Brilliance Awards recognize remarkable women in community banking who have demonstrated outstanding leadership in driving transformation through innovation and data. Karen and Amanda were selected due to her excellence in innovation and data-driven leadership.

F&M Bank’s CEO, Mike Wilkerson commented, “F&M takes great pride in our employees. Karen and Amanda are shining examples and exceptional people and professionals. They work diligently each date putting their deep industry knowledge and operational curiosity to work. Through their “Brilliance” they consistently deliver innovative solutions across the bank and to our customers.”

Karen Rose is the Senior Vice President of Deposit Operations- F&M Bank, with 36 years of experience in the banking industry, Karen Rose has cultivated a diverse career that began as a traditional bank teller. Throughout her journey, she has embraced every opportunity to learn and grow, benefiting from the guidance of exceptional mentors and managers. Her extensive background spans various areas of banking, including the Loan Department, Human Resources, Compliance, and Retail. Karen has found her true calling in Deposit Operations, where her passion for solving puzzles and preventing fraud flourishes. She is particularly excited about the latest advancements in money movement, as new systems for faster payments and instant fund delivery channels become standard in day-to-day banking. Karen is dedicated to providing innovative cash flow solutions for business customers, ensuring their needs are met in an ever-evolving financial landscape.

Amanda K. Hensley is a dedicated Systems Administrator at F&M Bank in Timberville, VA with over 24 years of banking industry experience. Amanda’s career path includes roles from teller to branch management, eventually leading a new accounts team in Deposit Operations. She has excelled in implementng workflow automation, integrating over 40 workflows that streamline operations, enhance data accuracy, and reduce manual processes. Her technical leadership in workflow integrations has optimized core banking functions, improving efficiency and service delivery bank-wide.

“The women we’ve recognized are changing the game in community banking. Their commitments to driving innovation are remarkable not only for their banks, but for each customer they serve,” says Kim Snyder, KlariVis founder and CEO. “It is incredibly encouraging to be in an industry where women are leading the charge in such an exceptional way, and I look forward to seeing what each of these women continues to accomplish.”

Created by veteran community bank executives, KlariVis enables banks of any size to accelerate growth by leveraging the data that is locked in its siloed banking systems. Developed on a modern technology stack, KlariVis lets banks see data in a way that empowers their teams and customers to live and work better. With the time saved on analysis, banks can put their new insights to work towards building a better bank. For more information, visit www.KlariVis.com.

Founded in 1908, F&M Bank is headquartered in the Shenandoah Valley, with a network spanning the I-81/64 corridor from Winchester to Waynesboro and beyond. The only publicly traded organization based in Rockingham County, the Company’s core values drive its corporate philanthropy, volunteerism, and local decision-making. We support clients with a robust digital banking suite, full-service branches, and essential services like mortgage loans, title services, wealth management, business banking, and agricultural lending. Find F&M Bank Corp, a publicly traded organization on the OTC Market Index: #FMBM.

F&M Bank Contact

Holly Thorne

Director of Marketing

https://www.fmbankva.com/wp-content/uploads/2024/11/klarivis.jpg8842000Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2024-11-01 11:33:212024-11-01 11:33:21F&M Bank’s Karen Rose and Amanda Hensley Named to 2024 Banking on Brilliance Awards

Houff is President of Houff Corporation, which is headquartered in Weyers Cave, Virginia.

TIMBERVILLE, VA / ACCESSWIRE / October 25, 2024 / The Board of Directors of F&M Bank Corp. (the “Company” or “F&M”), (OTCQX:FMBM), the parent company of Farmers & Merchants Bank (“F&M Bank” or the “Bank”), has appointed Neil A. Houff as a member of the Board.

Regarding the appointment, Mike Wilkerson, CEO of F&M Bank and a member of the F&M Bank Corp. Board of Directors, said, “Neil’s expertise and years of experience in agriculture and as a business leader will be invaluable to our Board and to the Bank. He knows how important it is for businesses and individuals here to have a strong, local bank . . . a bank that understands both local opportunities and challenges. As that bank for the Shenandoah Valley, F&M Bank is working hard today and preparing for our next 115 years of service to the people here. We’re excited that Neil will be part of that future.”

Houff joined Weyer’s Cave, VA-headquartered Houff Corporation in 1985 following his graduation from Virginia Tech and has served as its president since the early 1990’s, leading the company through a period of growth and expansion. More recently, he added the role of transloading operations manager for the company to his resume. Founded in 1975 on a Shenandoah Valley family farm, Houff Corp. specializes in agronomy, supply chain solutions, transloading, and biosolids management, and provides agricultural and industrial services to clients across Virginia. The company is held by Railside Enterprises, an ESOP company, which also holds IDM Trucking. Mr. Houff has served the Commonwealth of Virginia as a member of the Board of Agriculture and Consumer Services.

Chairman of the Board Michael Pugh said, “On behalf of my fellow board members, I am pleased to welcome Neil as a director. Our Board is comprised of experienced individuals who have set themselves apart in being part of and serving the Shenandoah Valley. Neil will fit right in and will be a help to us right from the start.”

“It is an honor to join F&M Bank Corp.’s Board,” Houff said. “This bank has its hands on the pulse of what is happening in the Valley and what matters to people here. Most importantly, they care. Because of that, joining the Board was an easy decision for me. I hope I can help them serve this area in the years ahead and be part of the growth I know they will experience.”

Other members of the F&M Bank Corp. Board include Ray Burkholder, Hannah Hutman, Anne Keeler, Chris Runion, Daphyne Saunders Thomas, John Willingham, Dean Withers, and Peter Wray. On June 30, 2024, F&M had total assets of $1.31 billion, total loans of $826.3 million, and total deposits of $1.19 billion.

ABOUT US

F&M Bank Corp. is an independent, locally owned, financial holding company offering a full range of financial services through our subsidiary, Farmers & Merchants Bank’s (F&M Bank) fourteen banking offices in Rockingham, Shenandoah, and Augusta counties, Virginia, and the cities of Winchester and Waynesboro, Virginia. The Company also owns F&M Mortgage, a mortgage lending subsidiary, and VSTitle, a title company subsidiary. Founded in 1908 as a community venture to serve the farmers and merchants of the Shenandoah Valley, where both the Company and the Bank are headquartered, F&M Bank remains more committed than ever to the success of the agricultural industry, small business ventures, and the nonprofit sector.F&M’s values, which are gregarious, resolute, original, and wholehearted (G.R.O.W.), combined with our brand pillars of sustenance, security, and enrichment, shape the Company’s decision-making, philanthropy, and volunteerism. The only publicly traded organization based in Rockingham County, we offer a diverse suite of financial products and services, and a strong team dedicated to living our mission of being the financial partner of choice in the Shenandoah Valley, both today and tomorrow, as we have been since 1908. Additional information may be found by visiting our website, fmbankva.com.

FORWARD-LOOKING STATEMENTS

This press release may contain “forward-looking statements” as defined by federal securities laws, which are subject to significant risks and uncertainties. These include statements regarding future plans, strategies, results, or expectations that are not historical facts, and are generally identified by the use of words such as “believe,” “expect,” “intend,” “anticipate,” “will,” “estimate,” “project” or similar expressions. These statements are based on estimates and assumptions, and our ability to predict results, or the actual effect of future plans or strategies, is inherently uncertain. Our actual results could differ materially from those contemplated by these forward-looking statements. Factors that could have a material adverse effect on our operations and future prospects include, but are not limited to, changes in local and national economies or market conditions; changes in interest rates; regulations and accounting principles; changes in policies or guidelines; loan demand and asset quality, including values of real estate and other collateral; deposit flow; the impact of competition from traditional or new sources; and other factors. Readers should consider these risks and uncertainties in evaluating forward-looking statements and should not place undue reliance on such statements. We undertake no obligation to update these statements following the date of this press release.

https://www.fmbankva.com/wp-content/uploads/2024/10/Neil-A-Houff-FM-Bank-Corp-Director-e1730217020713.jpg12131332Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2024-10-29 11:46:522024-10-29 11:49:10The F&M Bank Corp. Board of Directors Has Appointed Neil A. Houff As A Member of the Board

F&M Bank Welcomes Craig Morcom as New Commercial Relationship Manager in Winchester Market

Timberville, VA (10/04/2024) FOR IMMEDIATE RELEASE— F&M Bank is pleased to announce the addition of Craig Morcom, II to its growing lending team as a Vice President and Commercial Relationship Manager. With over 15 years of experience in various areas of banking and a deep commitment to supporting local businesses, Craig brings a diverse skill set and a track record of success to the Winchester market.

Craig began his career in banking after graduating from Hampden-Sydney College in 2008. With a banking background in his family, his early experience began in Richmond, VA. In 2011, Craig relocated to Winchester and served as a Branch Manager for a local financial institution until 2016, when he transitioned into commercial lending. Over the next several years, Craig gained extensive experience in commercial credit, loan documentation, and treasury management.

“I’m excited to join the commercial team here in Winchester and I am excited about the local resources and full-service banking services we can offer our customers,” Craig shared.

In his role as Commercial Relationship Manager, Craig will partner with local businesses to identify financing and deposit solutions best suited for their operational and growth needs.

John Sargent, Senior Vice President and Northern Valley Market Executive, expressed his enthusiasm for Craig’s addition to the team, stating: “We are thrilled to welcome Craig to our Winchester Commercial Team. His passion for customer service and unwavering commitment to client success make him an exceptional addition. Craig embodies the values and vision that drive our organization, and we are confident his expertise will greatly benefit F&M, as well as the Winchester and surrounding communities. We look forward to the positive impact he will make.”

Craig’s addition underscores F&M Bank’s commitment to supporting the Winchester business community by providing expert financial guidance and building long-term partnerships. With a deep history in the region and a steadfast dedication to client success, Craig is poised to help F&M Bank continue its tradition of exceptional service and community involvement.

F&M Bank Corp. is an independent, locally owned, financial holding company offering a full range of financial services through our subsidiary, Farmers & Merchants Bank’s (F&M Bank) fourteen banking offices in Rockingham, Shenandoah, and Augusta counties, Virginia, and the cities of Winchester and Waynesboro, Virginia. The Company also owns F&M Mortgage, a mortgage lending subsidiary, and VSTitle, a title company subsidiary. Founded in 1908 as a community venture to serve the farmers and merchants of the Shenandoah Valley, where both the Company and the Bank are headquartered, F&M Bank remains more committed than ever to the success of the agricultural industry, small business ventures, and the nonprofit sector.F&M’s values, which are gregarious, resolute, original, and wholehearted (G.R.O.W.), combined with our brand pillars of sustenance, security, and enrichment, shape the Company’s decision-making, philanthropy, and volunteerism. The only publicly traded organization based in Rockingham County, we offer a diverse suite of financial products and services and a strong team dedicated to living our mission of being the financial partner of choice in the Shenandoah Valley, both today and tomorrow, as we have been since 1908. Additional information may be found by visiting our website, fmbankva.com.

https://www.fmbankva.com/wp-content/uploads/2024/10/Blog-header-2.jpg6281200Jacob Mowry/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgJacob Mowry2024-10-04 09:51:202024-10-04 10:30:41F&M Bank Welcomes Craig Morcom as New Commercial Relationship Manager in Winchester Market

Partnering for Banking Connectivity That Helps F&M Meet Your Needs

By Glo Fiber Business

At Glo Fiber Business, we know partnerships that support the mission to serve customers with vital connectivity tools and services form the basis of better-than-ever experiences. That’s why we love working with organizations like F&M Bank — and in this case, our work was complemented by a strong partnership that grew out of shared roots right here in the Shenandoah Valley.

As F&M Bank remains committed to improving service availability, bandwidth, consistency and flexibility for all of its branches, we are happy to be the partner who provides high-speed networking and fiber solutions to keep you, your families and your businesses connected to your financial services.

Today, a range of financial organizations like F&M Bank must entrust their operations to stable, consistent, high-performance optical fiber connectivity that delivers added security, reliability and agility to support the future of banking and finance. In turn, this helps customers like you feel confident in your trusted relationship with providers like F&M Bank — and in today’s digital world, this kind of trust and security matters more than ever.

To learn more, be sure to watch this video case study.

About Glo Fiber Business

Glo Fiber Business provides advanced data and voice services for businesses, municipalities and educational institutions via a MEF-certified network with over 9,300 route miles of fiber. Services include fiber-optic connectivity, dedicated internet access, VoIP, managed services and network security options that are customized based on customers’ needs. As part of Shenandoah Telecommunications Company (Shentel) (Nasdaq: SHEN), Glo Fiber Business delivers cost-effective, quality internet and data solutions to commercial customers of all sizes in VA, PA, MD, WV and KY.

https://www.fmbankva.com/wp-content/uploads/2024/09/glofiber-FM-Bank.png585804Jacob Mowry/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgJacob Mowry2024-09-06 08:18:112024-09-06 12:50:41Partnering for Banking Connectivity That Helps F&M Meet Your Needs

F&M Bank is pleased to announce the promotion of Calan Jansen to the position of Senior Vice President. With over 20 years of wealth experience, Calan holds her Series 66, 63, SIE, 7, and 6 licenses, has been an invaluable asset to F&M Bank for the past 8 years, and is an Osaic Institutions Wealth Advisor with F&M Financial Services.

Throughout her career, Calan has consistently demonstrated excellence and has been recognized as one of the top 20 advisors nationally within Osaic Institutions, Inc. Her exceptional skills and expertise have also earned her the distinction of being the leading female advisor within the state of Virginia.

Calan is known for her personalized approach to financial planning, understanding that each individual has unique aspirations, circumstances, and risk tolerances. Her thoughtful and tailored strategies have set her apart in the industry, earning her the trust and confidence of her clients.

When asked about her promotion, Calan stated, “I am honored and excited to take on this new role as Senior Vice President at F&M Financial Services. I look forward to continuing to serve our clients with dedication and expertise, helping them achieve their financial goals and secure their future.”

F&M Bank CEO, Mike Wilkerson, expressed his confidence in Calan’s abilities, saying, “Calan has consistently demonstrated outstanding performance and exceptional leadership throughout her tenure at F&M Bank. Her promotion to Senior Vice President is well-deserved, and I have no doubt that she will excel in this expanded role, further contributing to the success of our organization.”

In addition to her professional achievements, Calan’s team recently achieved a significant milestone by winning the Gold award in the Shenandoah Valley Best contest. This community-voted contest, hosted annually by the Harrisonburg Radio Group, recognizes the excellence and dedication of local businesses within the Shenandoah Valley.*

For more information about F&M Financial Services and to get in touch with Calan Jansen, please visit www.fmbankva.com/calan-jansen.

* F&M Financial Services was awarded Gold in the 2024 Shenandoah Valley Best Contest’s Wealth Management category. The nomination and voting period occurred in March 2024, with results announced publicly in May 2024. Results can be viewed at www.shenandoahvalleybest.com/categories/2024

Investment and insurance products and services are offered through Osaic Institutions, Inc., Member FINRA/SIPC. F&M Financial Services is a trade name of F&M Bank. Osaic Institutions and F&M Bank are not affiliated.

Securities and Insurance Products:

Not Guaranteed by the Bank | Not FDIC Insured | Not a Deposit | Not Insured by Any Federal Government Agency | May Lose Value Including Loss of Principal

F&M Bank Corp. (OTCQX: FMBM) proudly remains the only publicly traded organization based in Rockingham County, VA, and since 1908, has served the Shenandoah Valley through its banking subsidiary F&M Bank, with full-service branches and a wide variety of financial services, including home loans through F&M Mortgage, and real estate settlement services and title insurance through VSTitle. Both individuals and businesses find the organization’s local decision-making and up-to-date technology provide the kind of responsive, knowledgeable, and reliable service that only a progressive community bank can.

https://www.fmbankva.com/wp-content/uploads/2024/08/jcansen-bench.jpg20001500Jacob Mowry/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgJacob Mowry2024-08-20 08:44:092024-08-20 08:44:09F&M Bank and F&M Financial Services Announce the Promotion of Calan Jansen to Senior Vice President

Celebrating F&M Bank’s Birthday: Honoring Our Legacy and Embracing the Future

As F&M Bank celebrates another milestone this month, we reflect on our rich history, core values, community involvement, and robust product offerings. From our inception in 1908 through today, F&M Bank has remained dedicated to supporting the Shenandoah Valley and beyond. We’ve grown a lot in the last 116 years, and F&M Bank is the bank it is today because of the community we serve!

A Legacy of Growth and Community Support

1908: Farmers and Merchants Bank was founded by business owners and farmers in Timberville, marking the beginning of our journey to support local communities.

1910: We launched our first public relations campaign with 500 Christmas postcards, establishing our commitment to community engagement.

1956: Under Chairman Lawrence Hoover, Sr., F&M Bank announced growth to $5 million at the annual shareholders meeting, demonstrating our financial stability and trustworthiness.

1973-1979: We expanded our reach by opening branches in Elkton and Broadway, enhancing our ability to serve more customers in the Shenandoah Valley.

1983: The State Corporation Commission approved the formation of F&M Bank Corp, including TEB Life Insurance Company, solidifying our presence in the financial sector.

1995-2008: Our growth continued with the acquisition of branches in Woodstock and Edinburg, the opening of new branches in Bridgewater and Harrisonburg, and the majority interest purchase in F&M Mortgage.

2012-2014: We expanded our services with a loan production office in Fishersville, an automotive dealer finance division in Harrisonburg, and announced record earnings following stock offerings, leading to new branch openings in Staunton.

2015-2019: F&M Bank continued its expansion with new branches in Staunton, Harrisonburg, Timberville, and Stuarts Draft, reflecting our commitment to accessibility and customer service.

2021-2023: Reaching $1 billion in assets, we expanded into Winchester and Frederick County, opened branches in Waynesboro and Old Town Winchester, renovated our Woodstock Branch, and celebrated our 115th anniversary.

Mid- 2024: We reached $1.3 billion in assets. This year, we launched refreshed core values focusing on GROW.

Core Values: GROW with Us

Our core values—Gregarious, Resolute, Original, and Wholehearted—are the foundation of everything we do.

Gregarious: We cultivate a sense of community and inclusivity, fostering meaningful engagement and leaving a positive impression in every interaction.

Resolute: Our steadfast commitment to accountability, resilience, and continuous improvement drives us to achieve excellence.

Original: We celebrate authenticity and creativity, empowering our team to think outside the box and contribute innovative solutions.

Wholehearted: Our deep sense of purpose, passion, and dedication ensures that we fully embrace our mission and make a lasting impact.

Community Involvement: Building a Brighter Future

F&M Bank’s commitment to the community extends beyond financial services. Our philanthropic efforts and community engagement are at the core of our mission. We’ve launched our pillars that help guide our community impact.

Educational Initiatives: We support financial literacy in schools, offer scholarships, and provide unique opportunities like the “day in the life of a banker” program for high school students.

Volunteer Efforts: Our team actively participates in community events, such as document shred days, and supports local food and agricultural initiatives.

Partnerships and Sponsorships: We build lasting relationships with organizations like the JMU Alumni Association and Big Brothers Big Sisters, contributing to the enrichment and well-being of our community.

Innovative Services: Meeting Modern Needs

F&M Bank remains at the forefront of innovation, offering robust digital banking solutions tailored to meet the needs of our customers. Our services include cash management, merchant services, and a comprehensive suite of banking products designed to support both personal and business financial goals.

Our commitment to technology and security ensures that our customers can bank with confidence, knowing their transactions and personal information are protected. We strive to provide accessible and responsive service, whether in-person or online, to ensure a seamless banking experience.

Looking Ahead: A Future of Promise and Potential

As we celebrate F&M Bank’s birthday, we reflect on our past achievements and look forward to a future filled with promise and potential. Thank you for being a part of our journey. Together, we will continue to grow, thrive, and make a positive impact on the Shenandoah Valley.

F&M continues strong start to 2024 with solid second quarter results.

See associated, unaudited summary consolidated financial data for additional information.

TIMBERVILLE, VA / ACCESSWIRE / July 29, 2024 / F&M Bank Corp. (the “Company” or “F&M”), (OTCQX:FMBM), the parent company of Farmers & Merchants Bank (“F&M Bank” or the “Bank”), today reported results for the quarter and six months ended June 30, 2024.

Net income was $3.0 million or $0.86 per share for the quarter ended June 30, 2024, compared to $1.2 million or $0.35 per share for the linked quarter ended March 31, 2024, and compared to $241,000 or $0.07 per share for the prior year quarter ended June 30, 2023. For the six months ended June 30, 2024, net income was $4.2 million or $1.21 per share, which exceeds net income of $1.3 million, or $0.37 per share, for the same period in 2023. Net income for the six months ended June 30, 2023, included $810,000 in after-tax, one-time expenses, including severance accruals for former bank officers.

On June 30, 2024, the Company had total assets of $1.31 billion, total loans of $826.3 million, and total deposits of $1.19 billion, reflecting growth in second quarter 2024 of $468,000 in total loans and $28.9 million in total deposits. Our loan portfolio consists of a mix of loan types, intended to hedge against risks associated with concentrations in any particular type of loan.

Also noteworthy, the Company’s tangible book value per common share has increased to $22.621 at June 30, 2024 from $21.551 on December 31, 2023. Tangible book value per common share is a non-GAAP financial measure. Further information can be found under the heading “Non-GAAP Financial Measures” and in the footnotes to the table accompanying this release.

“I am pleased to share F&M’s financial results for second quarter and year-to-date 2024,” said Mike Wilkerson, chief executive officer. “During the second quarter, we continued to achieve positive trends in increased revenue and interest income, controlled operational expenses, experienced solid growth in both deposits and loans, and benefited from strong asset quality.

“These results reflect our focus on generating ‘sufficient and sustainable profit,’ which is our number one priority. They also show our focus on the Company’s future, as the execution of our strategic plan continues and as the results from that plan are realized. Across the board, these outcomes and growth are a team effort, with each area and business line of F&M stepping up and contributing. It is through this team effort, for which we are all grateful, that we will continue to grow as a Company and in our ability to serve the people and businesses of the Shenandoah Valley.”

SECOND QUARTER INCOME STATEMENT COMPARISON

Overview

Net income for second quarter 2024 was $3.0 million or $0.86 per share, compared to $1.2 million or $0.35 per share for first quarter 2024, an increase of $1.8 million or $0.51 per share. Return on average assets was 0.93% and return on average equity was 15.59% for the three months ended June 30, 2024. Both ratios are higher than those reported for first quarter 2024. The improvement in net income is attributed primarily to a recovery of credit losses of $458,000 in the second quarter compared to a provision of $824,000 in the first quarter. Also contributing to the improvement, net interest income is $70,000 higher than in the linked quarter. Additionally, noninterest income increased by $644,000 to just under $3.0 million in the second quarter and noninterest expenses declined by $275,000. Due to the improved results, income tax expense increased by $472,000.

Net income increased by $2.8 million or $0.79 per share from the $241,000 or $0.07 per share reported for second quarter 2023. Return on average assets increased by 0.85% and return on average equity increased by 14.26%. The improved results reflect an increase of $422,000 in net interest income, a decrease of $997,000 in the provision for credit losses, an increase of $79,000 in noninterest income and a reduction of $2.2 million in noninterest expenses. Results for second quarter 2023 included a pre-tax severance accrual of $773,000 which lowered net income by $611,000.

Net Interest Income and Net Interest Margin

For second quarter 2024, net interest income totaled $8.2 million, an increase of $70,000 from first quarter 2024, as a $143,000 increase in interest income outpaced a $73,000 increase in interest expense. Net interest margin for the quarter was 2.72%, up eight basis points on a linked quarter basis. Higher loan balances and repricing of adjustable-rate loans contributed to a $142,000 increase in loan interest income, which comprised most of the increase in interest income and increased the earning asset yield by twelve basis points to 5.19%. Cost of funds increased by six basis points to 2.51%. Total interest expense increased by $73,000, a combination of a $614,000 increase in interest expense on deposits and a $542,000 decrease on interest expense on short-term debt. The increase in interest expense on deposits resulted from growth in time deposit balances and higher rates paid on new time deposits. This was partially offset by the decrease in interest expense on short-term debt as Federal Home Loan Bank advances declined from $60.0 million on March 31, 2024, to $20.0 million on June 30, 2024.

Compared to second quarter 2023, net interest margin increased by seven basis points as the earning asset mix shifted from cash and investments to loans. Loans as a percentage of earning assets increased to 68% in second quarter 2024 from 65% in second quarter 2023. Interest income increased $2.1 million, and the earning asset yield increased by 0.55% due to higher average balances and interest rates on loans, federal funds sold and interest-bearing cash balances. Interest expense grew by $1.7 million due to growth in both the average balances of and rates paid on time deposits causing the cost of funds to increase by 0.76%.

Provision for (Recovery of) Credit Losses

During second quarter 2024, the Bank recorded a $458,000 recovery of credit losses compared to an $823,000 provision for credit losses in first quarter 2024 and a $539,000 provision in second quarter 2023. The current quarter recovery was the result of the release of $608,000 in reserves related to the improvement in the collateral value on a $4.2 million individually evaluated loan relationship, net loan charge-offs of $179,000, slower loan growth and an improvement to the experience, depth and ability of lending management qualitative factor used in the Bank’s Allowance for Credit Losses on Loans (“ACLL”) model. By comparison, net charge-offs were $807,000 in first quarter 2024 and $344,000 in second quarter 2023. Also, gross loans grew more during those periods, by $3.8 million in first quarter 2024 and $19.3 million in second quarter 2023. On June 30, 2024, the ACLL totaled $7.8 million or 0.95% of gross loans outstanding.

Noninterest Income

Noninterest income, which includes gains and losses, totaled $3.0 million for second quarter 2024, an increase of $644,000 from first quarter 2024. Several categories of noninterest income increased on a linked quarter basis. Service charges on deposits increased by $18,000, investment services and insurance income increased by $48,000, mortgage banking income increased by $375,000, title insurance income increased by $124,000, and ATM and check card fees increased by $75,000. The other categories of noninterest income combined to increase noninterest income by $5,000.

Compared to second quarter 2023, noninterest income increased by $79,000. The increase resulted from increases of $17,000 in service charges on deposit accounts, $272,000 in investment services and insurance income, $236,000 in mortgage banking income, and $68,000 in title insurance income. There was a decrease of $436,000 in income from bank owned life insurance due to a gain received upon the death of a retired bank officer in 2023. Also, other operating income declined by $90,000. Smaller year-over-year changes in other categories netted to increase noninterest income by another $12,000.

Noninterest Expenses

Noninterest expenses totaled $8.2 million for second quarter 2024, compared to $8.4 million in first quarter 2024 a decrease of $275,000. During second quarter 2024, the Bank recognized $577,000 in gains from lump sum pension distributions, which drove a decrease in employee benefits expense of $514,000. There were decreases of $69,000 in ATM and check card fees, and $12,000 in legal and professional fees. These decreases offset increases of $65,000 in salary expense, $27,000 in occupancy expenses, $33,000 in equipment expense, $21,000 in other real estate owned expenses, $19,000 in telecommunications and data processing expenses, $24,000 in directors’ fees and $126,000 in other operating expenses. There were other changes in noninterest expense categories that combined to increase total noninterest expenses by $5,000.

Compared to the same quarter in 2023, noninterest expenses declined $2.2 million. As a result of the voluntary early exit plan that was implemented in 2023, salary expense declined by $1.2 million. Employee benefits expense declined by $684,000 due to the combination of the voluntary early exit plan and gains received from pension lump sum distributions. There were decreases of $46,000 in equipment expense, $141,000 in advertising expense, $71,000 in legal and professional fees, $88,000 in ATM and check card fees, and $144,000 in other operating expenses. Offsetting these decreases were increases of $88,000 in occupancy expense, $89,000 in FDIC insurance expense, and $41,000 in bank franchise tax expense. The remaining categories combined to increase noninterest expenses by $8,000.

YEAR-TO-DATE INCOME STATEMENT COMPARISON

Overview

Net income for the six months ended June 30, 2024 was $4.2 million or $1.21 per share, compared to $1.3 million or $0.37 per share for the same period in 2023, an increase of $2.9 million or $0.84 per share. Return on average assets was 0.65% and return on average equity was 10.96% for the first half of 2024. Both ratios are higher than those reported for the first six months of 2023. The improvement in net income is attributed primarily to lower noninterest expenses, which declined by $2.8 million to $16.6 million. Net interest income and noninterest income also improved by $709,000 and $231,000, respectively. The year-to-date provision for credit losses decreased from $539,000 in 2023 to $366,000 in 2024.

Net Interest Income and Net Interest Margin

In the first half of 2024, net interest income totaled $16.3 million, an increase of $709,000 from 2023, as a $4.7 million increase in interest income outpaced a $4.0 million increase in interest expense. Net interest margin was 2.71%, up two basis points from the 2.69% reported for the first half of 2023. Higher loan balances and repricing of adjustable-rate loans contributed to a $4.5 million increase in loan interest income, which comprised most of the increase in interest income and increased the earning asset yield by sixty-one basis points to 5.18%. Cost of funds increased by fifty-eight basis points to 2.49%. Total interest expense increased by $4.0 million, due to growth in both the average balances of and rates paid on time deposits.

Provision for Credit Losses

During the first six months of 2024, the Bank recorded a $366,000 provision for credit losses compared to a $539,000 provision for credit losses in the same period in 2023. The provision was the result of $986,000 in net charge-offs, which were partially offset by the release of $608,000 in reserves related to improvement in the collateral value of a $4.2 million individually evaluated loan relationship.

Noninterest Income

Noninterest income, which includes gains and losses, totaled $5.3 million for the first half of 2024, an increase of $231,000 from the first half of 2023. Several categories of noninterest income increased on a year-over-year basis. Service charges on deposit accounts increased by $66,000, investment services and insurance income increased by $345,000, mortgage banking income increased by $92,000, title insurance income increased by $136,000, and ATM and check card fees increased by $39,000. Income on bank owned life insurance declined by $434,000 due to the gains received in 2023. Other categories of noninterest income combined to decrease noninterest income by $13,000.

Noninterest Expenses

Noninterest expenses totaled $16.6 million for first six months of 2024, compared to $19.4 million for the same period of 2023, a decrease of $2.8 million. Salary expense declined by $1.7 million due to cost savings associated with a voluntary early exit plan implemented in fourth quarter 2023. Employee benefits expense declined by $919,000 due to a combination of the voluntary early exit plan, $577,000 in gains from lump sum pension distributions, and a refund of $162,000 received in March 2024 due to better than projected group health insurance claims in 2023. There were declines of $228,000 in advertising expense, $145,000 in other operating expense, $80,000 in ATM and check card fees, and $62,000 in directors’ fees. There were increases of $132,000 in occupancy expenses, $201,000 in FDIC insurance expense and $63,000 in bank franchise tax expense. There were other changes in noninterest expense categories that combined to decrease total noninterest expenses by $3,000.

BALANCE SHEET REVIEW

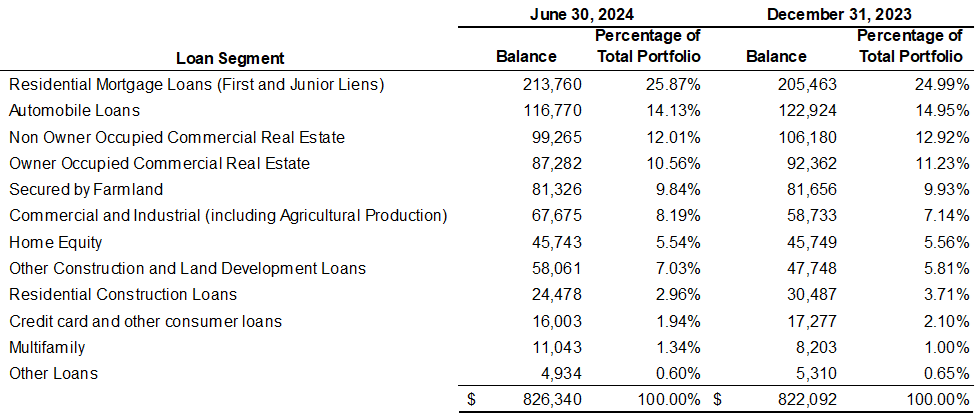

On June 30, 2024, assets totaled $1.31 billion, an increase of $15.0 million over December 31, 2023. Total loans increased by $4.2 million to $826.3 million, including increases of $8.3 million in residential mortgage loans, $10.3 million in other construction and land development loans, $8.9 million in commercial and industrial loans, and $2.8 million in multifamily loans. These increases were offset by decreases of $6.2 million in automobile loans, $6.0 million in residential construction loans, $1.3 million in credit card and other consumer loans, and $12.0 million in commercial real estate loans.

Investment securities decreased by $23.6 million due to paydowns on U.S. Agency mortgage-backed securities and expected bond maturities, combined with a decrease of $907,000 in unrealized loss on the bond portfolio. On June 30, 2024, the unrealized loss was $39.3 million compared to $40.2 million on December 31, 2023.

Total deposits on June 30, 2024, were $1.19 billion, an increase of $52.0 million from the end of 2023, due to growth of $46.0 million in interest bearing deposits, specifically time deposits, and an increase of $6.0 million in noninterest bearing deposits. On June 30, 2024, 11.34% of the Bank’s total deposits were uninsured.

Shareholders’ equity increased by $3.3 million to $81.6 million due to net income of $4.2 million, a decrease in accumulated other comprehensive loss of $717,000, and $102,000 in shares issued. These increases were offset by $1.8 million in dividends paid to shareholders. Tangible book value per common share has increased to $22.621 from $21.551 on December 31, 2023. Tangible book value per common share is a non-GAAP financial measure. Further information can be found under the heading “Non-GAAP Financial Measures” and in the footnotes to the table accompanying this release.

LIQUIDITY

The Company’s on-balance sheet asset liquidity includes cash and cash equivalents, unpledged investment securities, and loans held for sale, which totaled $200.1 million on June 30, 2024, up from $178.0 million on December 31, 2023.

The Bank had access to off-balance sheet liquidity through unsecured Federal funds lines totaling $90.0 million on June 30, 2024, and December 31, 2023. The Bank has a secured line of credit with the Federal Home Loan Bank (FHLB) with available credit of $150.0 million as of June 30, 2024, and $90.1 million as of December 31, 2023. The FHLB line of credit is secured by a blanket lien on qualifying loans in the residential, commercial, agricultural real estate, and home equity portfolios. The Bank also pledged $206.6 million in securities to the Federal Reserve discount window which may be used for overnight borrowings.

The Bank is scheduled to receive $74.6 million from bond paydowns and maturities by the end of 2024 which can be used to fund future loan growth and for other purposes.

LOAN PORTFOLIO

The Company’s loan portfolio is diversified with its largest segment being residential mortgage loans originated through its subsidiary F&M Mortgage that represents 25.87% of total loans. Total commercial real estate loans, both owner and non-owner occupied constitute $186.5 million or 22.57% of the loan portfolio. Automobile loans originated by its dealer finance division total $116.8 million and 14.13% of the portfolio. Following is a breakdown of the loan portfolio composition as of June 30, 2024, and December 31, 2023 (dollars in thousands):

ASSET QUALITY AND ALLOWANCE FOR CREDIT LOSSES

Nonperforming loans (NPLs) as a percentage of total assets were 0.58% on June 30, 2024, compared to 0.50% on December 31, 2023. Net charge-offs as a percentage of average loans were 0.09% for the quarter ended June 30, 2024, down 0.30% from the linked quarter March 31, 2024, and down 0.09% from second quarter 2023. Year-to-date net charge-offs for 2024 were 0.24% compared to 0.14% for the first six months of 2023.

The current quarter recovery was the result of the release of $608,000 in reserves related to improvement in the collateral value of a $4.2 million individually evaluated loan relationship, net loan charge-offs of $179,000, slower loan growth, and an improvement to the experience, depth and ability of lending management qualitative factor used in the Bank’s ACLL model. By comparison, net charge-offs were $807,000 in first quarter 2024 and $344,000 in second quarter 2023. Gross loans grew by $500,000 in second quarter 2024 and $4.2 million in first quarter 2024. On June 30, 2024, the ACLL totaled $7.8 million or 0.95% of gross loans outstanding compared to $8.3 million or 1.01% of gross loans outstanding at December 31, 2023.

The reserve for unfunded commitments decreased from $690,000 at December 31, 2023, to $575,000 at June 30, 2024, due to decreases in loan commitments of $10.3 million in commercial and industrial loans and $3.6 million in construction and land loans, which were offset by an increase of $2.1 million in commitments for 1-4 family residential construction and $3.1 million in owner-occupied commercial real estate.

DIVIDEND DECLARATION

On July 18, 2024, our Board of Directors declared a second quarter dividend of $0.26 per share to common shareholders. Based on our most recent trade price of $17.25 per share, this constitutes a 6.03% yield on an annualized basis. The dividend will be paid on August 29, 2024, to shareholders of record as of August 14, 2024.

###

ABOUT US

F&M Bank Corp. is an independent, locally owned, financial holding company offering a full range of financial services through our subsidiary, Farmers & Merchants Bank’s (F&M Bank) fourteen banking offices in Rockingham, Shenandoah, and Augusta counties, Virginia, and the cities of Winchester and Waynesboro, Virginia. The Company also owns F&M Mortgage, a mortgage lending subsidiary, and VSTitle, a title company subsidiary. Founded in 1908 as a community venture to serve the farmers and merchants of the Shenandoah Valley, where both the Company and the Bank are headquartered, F&M Bank remains more committed than ever to the success of the agricultural industry, small business ventures, and the nonprofit sector.F&M’s values, which are gregarious, resolute, original, and wholehearted (G.R.O.W.), combined with our brand pillars of sustenance, security, and enrichment, shape the Company’s decision-making, philanthropy, and volunteerism. The only publicly traded organization based in Rockingham County, we offer a diverse suite of financial products and services and a strong team dedicated to living our mission of being the financial partner of choice in the Shenandoah Valley, both today and tomorrow, as we have been since 1908. Additional information may be found by visiting our website, fmbankva.com.

NON-GAAP FINANCIAL MEASURES

The accounting and reporting policies of the Company conform to U.S. generally accepted accounting principles (“GAAP”) and prevailing practices in the banking industry. However, management uses certain non-GAAP measures, including tangible book value per share, to supplement the evaluation of the Company’s financial condition and performance. Management believes presentation of these non-GAAP financial measures provides useful supplemental information that is essential to a proper understanding of the Company’s operating results. These non-GAAP disclosures should not be viewed as a substitute for operating results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that may be presented by other companies. A definition of GAAP to non-GAAP measures is included in the footnotes to the table accompanying this release.

FORWARD-LOOKING STATEMENTS

This press release may contain “forward-looking statements” as defined by federal securities laws, which are subject to significant risks and uncertainties. These include statements regarding future plans, strategies, results, or expectations that are not historical facts, and are generally identified by the use of words such as “believe,” “expect,” “intend,” “anticipate,” “will,” “estimate,” “project” or similar expressions. These statements are based on estimates and assumptions, and our ability to predict results, or the actual effect of future plans or strategies, is inherently uncertain. Our actual results could differ materially from those contemplated by these forward-looking statements. Factors that could have a material adverse effect on our operations and future prospects include, but are not limited to, changes in local and national economies or market conditions; changes in interest rates; regulations and accounting principles; changes in policies or guidelines; loan demand and asset quality, including values of real estate and other collateral; deposit flow; the impact of competition from traditional or new sources; and other factors. Readers should consider these risks and uncertainties in evaluating forward-looking statements and should not place undue reliance on such statements. We undertake no obligation to update these statements following the date of this press release.

F&M Bank Corp. Summary Consolidated Financial Data (unaudited) Dollars in Thousands, except for per share data

Quarter to Date

Year-to-Date

6/30/2024

3/31/2024

12/31/2023 (3)

9/30/2023 (3)

6/30/2023 (3)

6/30/2024

6/30/2023 (3)

Condensed Balance Sheet

Cash and cash equivalents

$

50,459

$

52,486

$

23,717

$

22,159

$

36,505

$

50,459

$

36,505

Investment securities

355,930

369,744

379,557

383,502

394,868

355,930

394,868

Loans held for sale

3,958

1,385

1,119

2,028

881

3,958

881

Gross loans

826,340

825,872

822,092

805,602

776,260

826,340

776,260

Allowance for credit losses

(7,815

)

(8,408

)

(8,321

)

(9,166

)

(8,769

)

(7,815

)

(8,769

)

Goodwill

3,082

3,082

3,082

3,082

3,082

3,082

3,082

Other assets

77,691

72,053

73,350

75,212

75,543

77,691

75,543

Total Assets

$

1,309,645

$

1,316,214

$

1,294,596

$

1,282,419

$

1,278,370

$

1,309,645

$

1,278,370

Noninterest bearing deposits

$

270,246

$

267,106

$

264,254

$

277,219

$

277,578

$

270,246

$

277,578

Interest bearing deposits

915,011

889,237

868,982

856,691

859,534

915,011

859,534

Total Deposits

1,185,257

1,156,343

1,133,236

1,133,910

1,137,112

1,185,257

1,137,112

Short-term debt

20,000

60,000

60,000

60,000

47,000

20,000

47,000

Long-term debt

6,954

6,943

6,932

6,922

6,911

6,954

6,911

Other liabilities

15,818

15,194

16,105

14,567

15,153

15,818

15,153

Total Liabilities

1,228,029

1,238,480

1,216,273

1,215,399

1,206,176

1,228,029

1,206,176

Shareholders’ equity

81,616

77,734

78,323

67,020

72,194

81,616

72,194

Total Liabilities and Shareholders’ Equity

$

1,309,645

$

1,316,214

$

1,294,596

$

1,282,419

$

1,278,370

$

1,309,645

$

1,278,370

Condensed Income Statement

Interest income and fees on loans

$

13,494

$

13,352

$

13,061

$

12,525

$

11,517

$

26,846

$

22,371

Interest income and fees on loans held for sale

46

18

22

19

25

64

47

Income on cash and securities

2,180

2,207

2,074

2,028

2,092

4,387

4,198

Total Interest Income

15,720

15,577

15,157

14,572

13,634

31,297

26,616

Interest expense on deposits

6,951

6,337

6,108

5,811

5,218

13,288

9,255

Interest expense on short-term debt

454

996

812

702

523

1,450

1,514

Interest expense on long-term debt

116

115

116

115

116

231

228

Total Interest Expense

7,521

7,448

7,036

6,628

5,857

14,969

10,997

Net Interest Income

8,199

8,129

8,121

7,944

7,777

16,328

15,619

Provision for (recovery of) credit losses

(458

)

824

(134

)

620

539

366

539

Noninterest income

2,986

2,342

2,464

2,572

2,907

5,328

5,097

Noninterest expense

8,156

8,431

10,482

8,922

10,335

16,587

19,364

Income tax expense (benefit)

471

(1

)

(220

)

(44

)

(431

)

470

(483

)

Net Income

$

3,016

$

1,217

$

457

$

1,018

$

241

$

4,233

$

1,296

Per Share Data

Earnings per common share – basic

$

0.86

$

0.35

$

0.13

$

0.29

$

0.07

$

1.21

$

0.37

Book Value per Share

23.54

22.11

22.47

19.43

20.75

23.54

20.75

Tangible Book Value per Share (1)

22.62

21.20

21.55

18.50

19.82

22.62

19.82

Key Performance Ratios

Return on Average Assets

0.93

%

0.37

%

0.14

%

0.32

%

0.08

%

0.65

%

0.20

%

Return on Average Equity

15.59

%

6.25

%

2.49

%

5.80

%

1.33

%

10.96

%

3.62

%

Noninterest Income / Average Assets

0.92

%

0.71

%

0.76

%

0.80

%

0.92

%

0.82

%

0.80

%

Noninterest Expense / Average Assets

2.52

%

2.54

%

3.23

%

2.76

%

3.28

%

2.56

%

3.05

%

Efficiency Ratio (2)

71.23

%

78.67

%

96.79

%

82.81

%

94.35

%

74.77

%

91.14

%

Net Interest Margin

2.72

%

2.64

%

2.66

%

2.67

%

2.65

%

2.71

%

2.69

%

Earning Asset Yield

5.19

%

5.07

%

4.96

%

4.87

%

4.64

%

5.18

%

4.57

%

Cost of Interest Bearing Liabilities

3.21

%

3.14

%

3.00

%

2.87

%

2.61

%

3.17

%

2.51

%

Cost of Funds

2.51

%

2.45

%

2.37

%

2.26

%

1.75

%

2.49

%

1.91

%

Net Interest Spread

2.68

%

2.62

%

2.59

%

2.61

%

2.89

%

2.69

%

2.66

%

Net Charge-offs

$

179

$

807

$

770

$

193

$

344

$

986

$

510

Net Charge-offs as a % of Avg Loans

0.09

%

0.39

%

0.38

%

0.10

%

0.18

%

0.24

%

0.14

%

Non-Performing Loans

$

7,586

$

6,246

$

6,469

$

3,586

$

1,997

$

7,586

$

1,997

Non-Performing Loans to Total Assets

0.58

%

0.47

%

0.50

%

0.28

%

0.16

%

0.58

%

0.16

%

Non-Performing Assets

$

7,586

$

6,246

$

6,524

$

3,586

$

1,997

$

7,586

$

1,997

Non-Performing Assets to Total Assets

0.58

%

0.47

%

0.50

%

0.28

%

0.16

%

0.58

%

0.16

%

ACLL as a % of Total Loans

0.95

%

1.02

%

1.01

%

1.14

%

1.13

%

0.95

%

1.13

%

Loans to Deposits

69.72

%

71.42

%

72.54

%

71.05

%

68.27

%

69.72

%

68.27

%

(1) Tangible book value per share is calculated by subtracting goodwill and other intangibles from total shareholders’ equity and dividing the result by the common shares outstanding. Tangible book value per share is a non-GAAP financial measure that management believes provides investors with important information that may be related to the valuation of common stock.

(2) The Efficiency Ratio equals noninterest expenses divided by the sum of tax equivalent net interest income and noninterest income. Noninterest income excludes gains (losses) on securities transactions and low-income housing partnership losses. Noninterest expense excludes amortization of intangibles.

(3) Certain reclassifications have been made in the 2023 financial information to conform to reporting for the 2024. These reclassifications are not considered material and had no impact on prior year’s net income, balance sheet or shareholders’ equity.

FOR MORE INFORMATION, CONTACT

Lisa F. Campbell | EVP | Chief Financial Officer

540-896-1705 fmbankva.com

https://www.fmbankva.com/wp-content/uploads/2023/05/Executive-Team-2023-FINAL-e1684509203761.jpg9352000Jacob Mowry/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgJacob Mowry2024-07-30 11:03:202025-05-22 17:19:05F&M BANK CORP. REPORTS SECOND QUARTER 2024 EARNINGS AND QUARTERLY DIVIDEND