Recently, card skimming has been a hot topic in our area. There is a group of professional criminals placing skimmers on gas pumps along the 1-81 corridor. How can you protect yourself from the agony of a fraud claim? Here are our 6 best tips:

Recently, card skimming has been a hot topic in our area. There is a group of professional criminals placing skimmers on gas pumps along the 1-81 corridor.

F&M Bank has been in contact with the Secret Service in Richmond to help combat this issue and protect our customers. The Secret Service has shared the following information:

Skimmers are placed inside the gas pumps making detection near impossible. There is a Bluetooth device being plugged into the card reader on the inside of the pump that is capturing card and PIN numbers. The criminals have even created stickers that look legitimate in order to convince consumers that the gas pump is secure.

How can you protect yourself from the agony of a fraud claim? Here are our 6 best tips:

1) Pay for your gas inside the store. You will completely avoid the skimming device.

2) Do not use pumps located farthest away from the store. They are hardest for store employees to monitor and most likely to be targeted.

3) If you pay at the pump, ALWAYS run your card as credit. If you enter your PIN, the criminals then have the number which can lead to fraudulent ATM withdrawals and larger losses.

4) Sign up for transaction text alerts. Knowing each time your card is used can give you the power to shut down your card quickly if an unauthorized transaction comes through. We offer this service through our mobile app!

5) Be sure your card issuer has your current phone number and offers 24/7 fraud watch so that you can be contacted when suspicious activity takes place.

6) Finally, fraud losses are covered by the card issuer, and this offers some relief. It may take up to 10 days to get your money back, which is a financial hardship and can be stressful, but you will recover your losses!

We understand that fraud can be an extremely frustrating situation, that is why we’re offering these tips. Help us protect your money and be cautious when paying at the pump!

/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svg00Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2017-12-14 17:46:002023-06-16 12:49:15Protect Yourself from Card Skimming at the Gas Pump

The holidays are supposed to be a relaxing time spent with family and friends reflecting on the current year and looking ahead to the next. However, for most Americans, the holidays invoke feelings of stress and fatigue. According to a poll conducted by the American Psychological Association, nearly a quarter of Americans report feeling extreme stress during the holiday season, and 45% of Americans would prefer to skip Christmas. But, that doesn’t have to be the case. We can’t guarantee a white Christmas, but with proper planning and budgeting, you can make your holiday season the most wonderful time of the year.

The holidays are supposed to be a relaxing time spent with family and friends reflecting on the current year and looking ahead to the next. However, for most Americans, the holidays invoke feelings of stress and fatigue. According to a poll conducted by the American Psychological Association, nearly a quarter of Americans report feeling extreme stress during the holiday season, and 45% of Americans would prefer to skip Christmas. But, that doesn’t have to be the case. We can’t guarantee a white Christmas, but with proper planning and budgeting, you can make your holiday season the most wonderful time of the year. Here are some tips!

Keep it Basic

Your holiday dinner doesn’t have to consist of a cranberry stuffed Cornish game hen and 12 side dishes to turn heads. In our social media driven world, you may look to Pinterest and Facebook for inspiration, but don’t let those platforms set the standard for what is normal. If you want to try a fancy dish, that’s great!

But, if you don’t want to cook a spread suitable for Country Living Magazine, just stick to the basics. You’re guaranteed to save money on groceries, plus, it’s less stressful! And, once you put the essentials on your plate – turkey, potatoes, stuffing, rolls, and green beans – who has room for more?

Before roasting an entire turkey, take a look at your guest list. Is a whole bird really necessary? That’s a lot of food (and a lot of work). Consider serving just turkey breast instead! It cuts down on leftovers, and it’s more affordable.

Coupons and Savings Apps

Coupons are your friend! Often, you can find lots of great deals in the Saturday paper. Try browsing the weekly circulars online to look for sales on items you need. Also, try loading digital coupons to your store discount cards!

There are great savings apps out there as well! Jessica Hartman, Customer Service Representative at our Coffman’s Corner branch, offers the following tip: “I try to pair sales up with my Ibotta and Checkout 51 apps. If you watch the sales, you can purchase a turkey fairly cheap – I ended up getting one for $0.59/lb last year.”

Also, don’t be afraid to ask for help. If you are hosting the holiday dinner at your home, ask family and friends to bring a side dish or dessert. Divide out the responsibility so you’re not drained, both physically and financially.

Plan Ahead and Budget

Spending money on gifts is the most stressful part of the holiday season, according to the APA study. Don’t let it be! Begin planning for the holiday season early in the year. Katie Fulk, Head Teller at our Bridgewater Branch, says, “Some of the girls here like to buy Christmas gifts throughout the year. This helps financially because the cost of gifts can be spread from month to month, and then things are not as overwhelming at Christmas time. Also, if you save $20 a week, you end up with over $1,000.00 in a years’ time of saving.”

Looking for a great way to save throughout the year? Open a Christmas Club! The concept is that customers deposit a certain amount of money each week into a special savings account. Then, receive the money back near year-end for Christmas shopping. It’s a great way to put aside a small amount of money each week lessening the financial burden in December.

Save Money While Shopping

It might be too late to start saving for Christmas this year, but you still have options to save! Black Friday offers a variety of deals. If you hate fighting the crowds, most deals are also offered online, so stay home in the comfort of your pajamas and shop! Cyber Monday also offers great savings!

Charles Halterman, Branch Specialist at our Myers Corner location suggests a Chinese gift exchange to cut down on costs. He says, “My family and I did a Chinese gift exchange one year for the adults. Everyone buys one gift and wraps it. Then, you put numbers in a bowl for however many people are participating. Everyone draws a number, and Number One chooses a gift. Then, Number 2 can steal Number 1’s gift or choose a new gift…and so on, and so on. In the end, everyone gets one gift, you have fun playing a game with friends and family, and everyone saves money!”

Gifts to Please Anyone

Finally, we all have that family member who won’t make a Christmas gift suggestion. If you find yourself not needing anything, consider asking friends and family to make a donation to a charity you support instead of receiving another pack of socks you don’t need (or want). Kristen Huffman, Customer Service Representative at our Craigsville Branch does this every year. She says, “I ask family to send money to a charitable organization instead of buying me gifts. I don’t really need anything especially something that will just clutter up my house even more. Each year my husband gives money to World Vision as my Christmas present.”

Gift cards are also a great option for those family members without a Christmas list. Did you know you can purchase Visa gift cards at any F&M Bank Branch location? Avoid the long lines at Walmart, and pick up a Visa gift card next time you’re making a banking transaction.

/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svg00Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2017-11-17 21:39:002023-06-16 12:49:18Take the Stress Out of Your Holidays

Mobile banking is more than just a convenient way to check your accounts on the go – it’s a toolbox.

In fact, when you log-in to your account, you have dozens of tools at your disposal, and the best part, they’re free! If you’re enrolled in mobile banking, but not taking advantage of various alerts and account preferences, use the below tips to turn your digital banking into an aid for managing your money and monitoring your account activity.

Mobile banking is more than just a convenient way to check your accounts on the go – it’s a toolbox.

In fact, when you log-in to your account, you have dozens of tools at your disposal, and the best part, they’re free! If you’re enrolled in mobile banking, but not taking advantage of various alerts and account preferences, use the below tips to turn your digital banking into an aid for managing your money and monitoring your account activity.

1) Set Up Alerts

In the F&M Bank mobile app, customers can set up various text alerts based on account activity. Here are a few alert options you can access in minutes.

Balance

If you are not proactive at checking your account balance on a regular basis, you can receive a text either daily, or monthly, depending on your preference. This is a great way to ensure your checkbook and online account balances match!

Daily balance – This will send an alert of your daily balance for a particular account.

Monthly balance – This will send an alert once a month of your current balance on a particular day.

Balances Above/Below

You also can set up alerts that notify you when your account balance falls below or goes above and indicated amount. For example, if you establish an alert and indicate $1,000 as your preferred checking account balance, you will be alerted via text if an expenditure drops your balance to $950. This tool can serve as a wake-up call for overspending, or a pleasant surprise for those trying to achieve a savings goal.

Balances above/below – This will send an alert when your balance falls below or goes above the amount you define.

Transaction

This tool alerts you when certain transactions are made. You can select which transactions interest you (ACH, Debit Card, Wires, etc.), or, you can select all. A dollar amount must be established. For example, if you want to receive a text every time a debit card transaction is made greater than $50, you can set up that alert in minutes. This is a great way to monitor fraud, and ensure you are aware of the purchases being made on your account.

Transaction – this will send alerts when particular transactions are applied to your account.

To begin setting up alerts, visit the “Text Banking” tab in the mobile app.

2) Make Savings Automatic

Take advantage of the automatic transfer tool in online banking to build your savings. If you know your paycheck posts to your account every Friday, schedule a weekly transfer from your checking account to savings. If you don’t think you can afford to save a large amount each week, start small. By setting up an auto-transfer, you’re consistently saving, and that is what is important. Just click, the “Transfers” tab in the mobile app to get started.

3) Protect Your Accounts with Touch ID

F&M Bank’s mobile app is extremely secure – it uses 128-bit SSL (Secure Socket Layer) encryption to protect your information and we don’t store any information on your phone. You are required to log in each time you access your account information or bill pay services through Mobile Banking. Instead of entering your username and password every time, use your thumb print instead! Just visit the “User Options” tab to set up this feature.

4) Deposit Checks on the Go

Deposit checks quickly and safely with the F&M Bank mobile app!

Sign in to the app.

Click on “Mobile Deposit Capture”.

Choose deposit checks. Or, click transactions to view recent deposits.

Follow the prompts on your mobile screen.

Confirm the details are correct and press “submit”.

You will come to the final screen – press “I agree”, and you are finished.

/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svg00Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2017-10-11 18:38:002023-06-16 12:53:30Maximize Your Mobile Banking Experience

So you’ve decided to get a pet. Aside from making sure you’re responsible and emotionally prepared to give your new friend a great life — no pressure — it’s crucial to consider the logistics. This means time — and, of course, money.

So you’ve decided to get a pet. Aside from making sure you’re responsible and emotionally prepared to give your new friend a great life — no pressure — it’s crucial to consider the logistics. This means time — and, of course, money.

Here’s what to expect in terms of expenses:

Bringing Fido home

The initial cost of getting a pet, including the necessary equipment, can range from less than $100 to several thousands, depending on the type of animal or breed. For example, a report from Rover.com finds the average one-time cost of getting a dog is $838.

But if you want a purebred puppy, you’ll pay upward of $2,000 at some breeders before going shopping for a dog bed and toys. Adoption is always a low-cost way to get a pet. At most shelters, the one-time fee ($0-$500) covers vaccines, spaying/neutering and a microchip.

Remember that dogs aren’t the only animals waiting for a forever home at shelters. Rabbits, guinea pigs, hamsters, birds, reptiles, and fish are occasionally available for adoption.

Recurring expenses

Your pet’s monthly expenses also depend on its size, age, health and behavior, as well as your location and the brand and type of supplies you buy. Fish are usually the lowest maintenance, requiring only food. Be prepared to shell out a couple hundred dollars for an aquarium when you first get Nemo, though.

For small mammals, budget for food, bedding and occasional toys or treats. This will total about $300 a year, according to the American Society for the Prevention of Cruelty to Animals. Larger mammals, such as guinea pigs and rabbits, love lots of bedding that needs to be changed often and cost closer to $600-$700 annually.

Cats and dogs need food, treats and toys, yearly medical checkups, flea and tick prevention, and sometimes licenses. The ASPCA estimates that caring for a cat costs $670 per year, including an annual vet visit. Rover.com reports the average monthly costs of owning a dog to be $75, with a yearly checkup averaging $120. That works out to $1,020 per year.

Bump up your budget for big dogs that need (a lot) more food, animals that must be groomed often, pets that need walkers or sitters, and, depending on your animal’s health and behavior, medical bills.

Unexpected costs

With pets, accidents happen — and they could cost you thousands.

“Unexpected veterinary bills are the most surprising — and most costly — variables in dog ownership,” says Brandie Gonzales, director of corporate communications and PR for Rover.com. “While preventative care can go a long way, you’ll want to be prepared for any veterinary emergencies, like if a dog were to accidentally eat something he shouldn’t. Consider pet insurance, which will make unforeseeable expenses easier on your wallet.”

Of course, cats and other animals are subject to accidents and surprise vet visits, too.Owners might also be surprised at the cost of pets with behavioral problems, including a trainer. “Another unexpected cost would be replacing any household or personal items that your pet might mistake as a toy,” Bank says.

Add pet-sitting to your vacation budget next time you plan to go out of town, and a walker if you have a pup and are gone most of the day. These services can range from around $15 for a walk to about $65 for a night of boarding.

How to save

You don’t need a $325,000 dog mansion to give your pet its best life. There are plenty of ways to save on the things you need: Buy food and treats in bulk for a discount, search your local Craigslist for hand-me-down equipment such as aquariums and cages — just be sure to sanitize before using — and check for coupons from big-box pet stores online before going shopping. You can also wash your dog at home to cut down on trips to the groomers.

Thoughtful purchases will save you money. “Buy puzzle toys to feed your dog treats instead of giving them easily consumable treats,” Gonzales says. “The toys are a great game for your dog and you’ll spend less on treats.”

Just don’t skimp on high-quality, nourishing pet food; flea and tick medication; and veterinary care. “Preventative treatments, vaccinations and dental care keep your dog healthy and help you save in the long run,” Gonzales says.

/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svg00Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2017-10-04 17:07:002023-06-16 12:49:19How Much Does Owning a Pet Really Cost?

You might share certain spending habits with other millennials — and you might occasionally catch flak for those habits. But some of these patterns are a byproduct of your age and the times we live in: spending less on health care because younger adults are generally healthier, for example, or spending less on magazines and records and more on e-books and streaming music. And if you compare how much of your income you’re spending on, say, entertainment, with what other generations are spending, you might be surprised by how small the differences are.

You might share certain spending habits with other millennials — and you might occasionally catch flak for those habits. But some of these patterns are a byproduct of your age and the times we live in: spending less on health care because younger adults are generally healthier, for example, or spending less on magazines and records and more on e-books and streaming music. And if you compare how much of your income you’re spending on, say, entertainment, with what other generations are spending, you might be surprised by how small the differences are.

By looking at annual spending across generations in the Bureau of Labor Statistics’ Consumer Expenditure Survey, you’ll see how age groups spend differently according to their needs and priorities — and get an idea of how your own priorities and payouts measure up.

The Consumer Expenditure Survey measures all annual expenditures, such as housing, health care, food, entertainment, insurance, education, utilities, clothing and transportation.

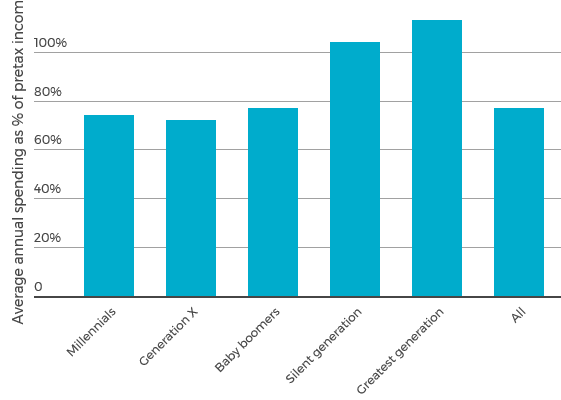

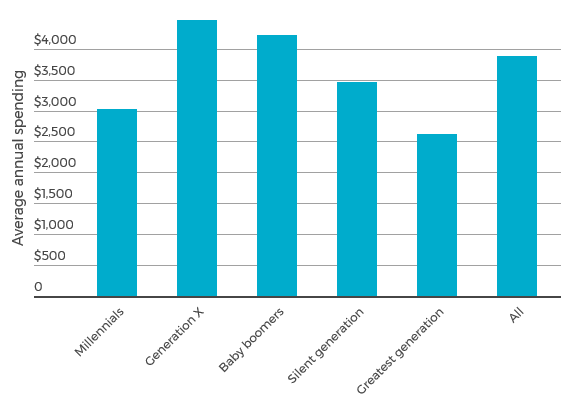

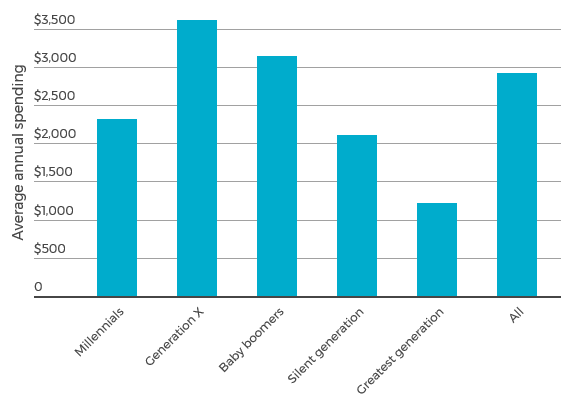

Total annual spending: How do you compare?

$48,576: Average amount millennials spent in 2016

The oldest two generations spent far more of their income last year, but they also earn far less than other groups. The average pretax income for millennials was $65,373.

Food

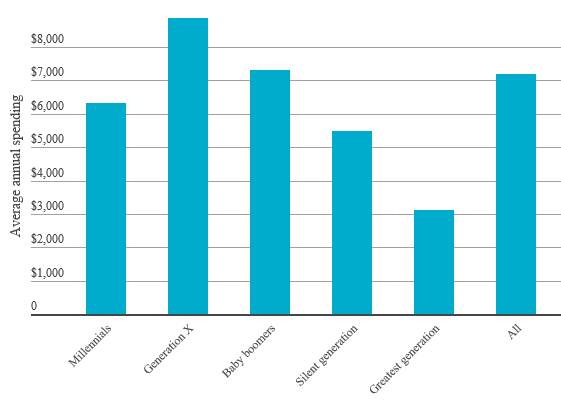

You might enjoy going out for dinner — but so does everyone else — and your overall food spending is well-aligned with nearby generations. Millennials spent an average of $6,316, or 10% of their pretax income, on food in 2016. Members of Generation X spent the highest dollar amount in this category — $8,870 — but it accounted for a similar percentage (9%) of their income.

Food spending: How do you compare?

$6,316: Average amount millennials spent on food in 2016

Millennials spent 47% of their food budgets on food away from home, more than all other groups. Still, their total food spending as a percentage of income (10%) was equal to the average across all generations.

Fun fact: Millennials spent less than any other generation on ice cream last year: $40.34, on average.

Alcohol

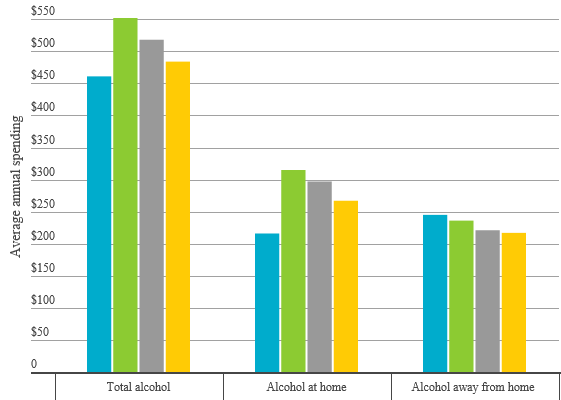

By some measures, you might have spent more than members of other generations on drinking away from home last year — 53% of your alcohol budget if you’re average, according to the data. But all generations spent approximately 1% of their income on alcohol.

Alcohol spending: How do you compare?

$461: Average amount millennials spent on alcohol in 2016

All generations spent approximately 1% of their income on alcohol. However, millennials spent the greatest portion of their alcohol budget (53%) and the most money overall on booze away from home.

Shelter

If you’re like most of your peers, you spent relatively little on shelter in 2016 — second only to the silent generation, who might live in mortgage-free homes or with other family members. Shelter spending includes many of the costs of keeping a roof over your head: rent or costs to own, maintenance and repairs, and homeowners or renters insurance, for example.

Shelter spending: How do you compare?

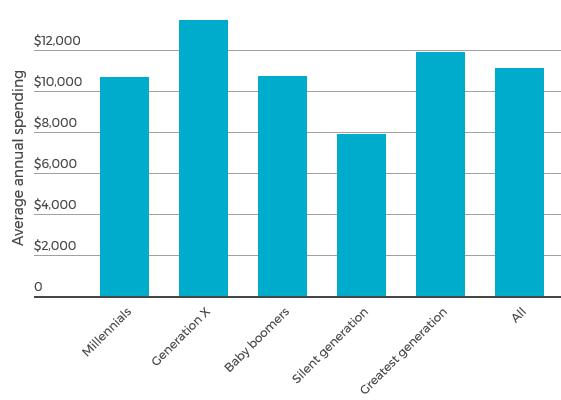

$10,678: Average amount millennials spent on shelter costs in 2016

Millennials spent fewer dollars, on average, than Generation X and baby boomers, but shelter costs accounted for 16% of their pretax income. Generation X spent 14% of their income on shelter, and baby boomers spent 13%.

Utilities

Nearly everyone spent less on residential phone service than cellular phone service in 2016, and you’re among the generation that spent the least. Millennials, Generation Xers, and baby boomers all spent an average of about 5% of their annual income on utility costs. Considering you’re likely to have a lower income than an older adult, you might be doing some strategic budgeting to keep those bills under control.

Utility spending: How do you compare?

$3,020: Average amount millennials spent on all utilities in 2016

Millennials, Generation X and baby boomers spent an average of 5% of their annual salary on utilities last year.

Not all utilities measured in the Consumer Expenditure Survey are portrayed in this chart.

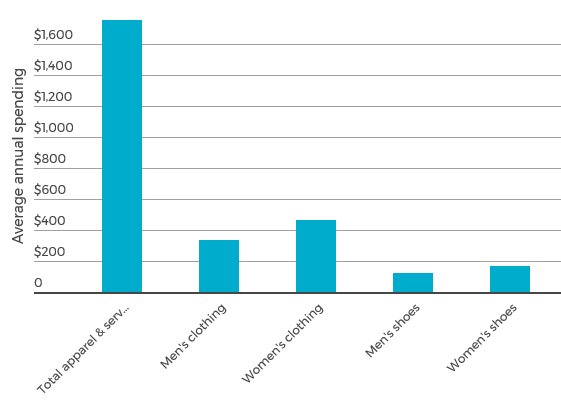

Clothing

Your generation might get a bad rap for frivolous spending, but you probably spent less than many older adults on clothing in 2016. Members of Generation X spent far more — $2,577, on average — but Gen Xers and millennials both spent 3% of their pretax income on apparel and related services.

Clothing spending: How do you compare?

$1,753: Average amount millennials spent on apparel and related services in 2016

All groups spent an average of between 2% and 3% of their total income on apparel. Compare total spending across generations in the second tab below.

Not all apparel and services expenses within the Consumer Expenditure Survey are illustrated in this chart.

Transportation

If 2016 expenditures are an indication, you’re more likely to buy a used vehicle than new. And you probably spent more on public transportation — including buses, taxis, subways and commuter rails — than members of older generations.

Because millennials are slightly less likely to own vehicles than other generations, the data on vehicle purchases, gas and related car-ownership expenses are slightly skewed by those who answered $0 to those questions.

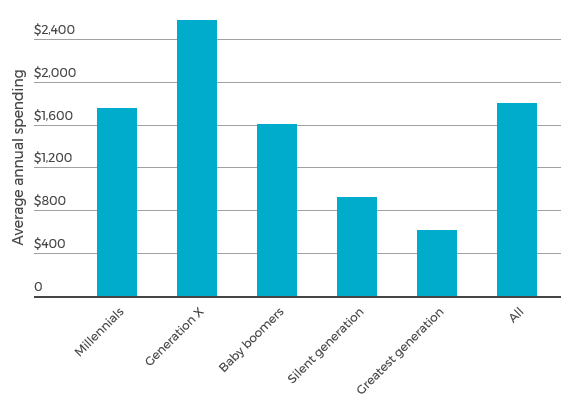

Transportation spending: How do you compare?

$8,426: Average amount millennials spent on all transportation costs in 2016

These costs accounted for 13% of millennials’ income, on average, while Generation X spent 11% and baby boomers spent 12%. Compare total transportation expenditures across all generations in the second tab below.

Not all transportation expenses included within the Consumer Expenditure Survey are displayed in this chart.

Fun fact: Millennials spent more on new motorcycles than any other generation ($64.65, on average), and spent far more on new motorcycles than used ($13.92, on average).

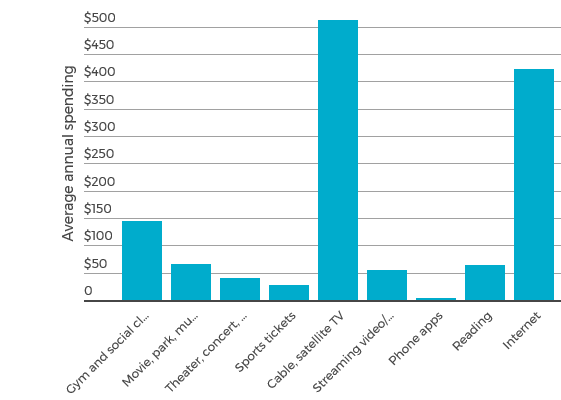

Entertainment

You might have spent less than members of some older generations on entertainment. Still, you likely spent more on streaming audio and video, and television probably took the biggest chunk out of your entertainment budget, with home internet services a close second.

Entertainment spending: How do you compare?

$2,311: Average amount millennials spent on all entertainment costs in 2016

All but the silent generation, who spent 5%, spent an average of about 4% of their income on entertainment. See how total entertainment spending compared across age groups in the second tab below.

Not all entertainment expenses included within the Consumer Expenditure Survey are displayed in this chart.

Fun fact: Millennials spent more on musical instruments than any other generation: $25.04, on average.

Notes on the data

The data are from the Consumer Expenditure Survey, released Aug. 29, 2017. It’s based on questions the Bureau of Labor Statistics asks households across the U.S. about their spending habits throughout each year. When numerous people answer $0 for any single expense on the Consumer Expenditure Survey, the data are skewed and the average amount spent seems low. For example, few millennials pay for a home landline. So, in 2016, the average amount millennials spent on residential phone service was $90, or approximately $7.50 per month, far lower than most residential phone bills. There are similar patterns in vehicle and home ownership costs among millennials, as well as throughout the survey data.

The survey is asked of “consumer units,” not individuals. This means, in most cases, that the expenses are attributed to a single person in the household. So, for instance, if a 19-year-old millennial lives at home with his 45-year-old father, the household expenditures will appear under the father, or in the Generation X category of the generational tables.

00Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2017-09-26 20:54:002023-06-16 12:49:19Millennials: How Much Are You Really Spending?

Identity theft and consumer fraud can happen in an instant, so it’s important to protect yourself. Learn about simple tips and tools you can use to reduce your risk of identity theft and protect your financially sensitive information.

Identity theft and consumer fraud can happen in an instant, so it’s important to protect yourself. Learn about simple tips and tools you can use to reduce your risk of identity theft and protect your financially sensitive information. Our short interactive course will equip you with important knowledge regarding:

00Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2017-09-08 19:32:002023-06-16 12:49:21Safeguard Your Identity with These Helpful Resources

Getting a job, buying a car, buying a home — all of these milestones are both exciting and at times stressful for young adults just getting started. For many people, these are wonderful goals that help push them forward. But as millennials build their careers, start families and consider their futures, it’s important to remember that true success has little to do with your job title, the type of car that you drive or the size of your house. Success is about having peace of mind.

Getting a job, buying a car, buying a home — all of these milestones are both exciting and at times stressful for young adults just getting started. For many people, these are wonderful goals that help push them forward. But as millennials build their careers, start families and consider their futures, it’s important to remember that true success has little to do with your job title, the type of car that you drive or the size of your house.

Success is about having peace of mind. And you cannot feel successful or have a sense of true accomplishment when you are worried about money. Millennials must be comfortable with their finances to achieve long-term success.

To have peace of mind as well as peace in your finances, you must prepare for and practice the keys to financial wellness:

Invest in yourself

This is about investing in your future by seeking the highest education that you desire intellectually and can afford financially. Your knowledge and education will open doors that would have otherwise remained closed. Education has a major influence on your earning power. It can propel you when the economy is good and sustain you when it’s bad. You can lose your job but not your education.

Save, save, save

The most essential rule of saving is to pay yourself first. You should contribute to your personal savings and your retirement savings with every paycheck. The simplest way to accomplish this goal is through direct deposit. For your personal savings, you can have a set amount deposited into a savings account and then have the balance go into your regular checking account, which is used to pay for your living expenses. By doing this, you are assured that you have emergency savings. For your retirement savings, you should start contributing to a 401(k) or individual retirement account as early as you can. Start contributing in your 20s so you have even more time to take advantage of compound interest (in which your earnings are added to your principal).

Limit your use of credit

Spend your money in a way that minimizes your debt. You should use cash to pay for small-ticket items, those things you can afford to pay for outright. Expensive purchases such as a house, car and furniture understandably might not be bought for cash. But you can still be mindful of your spending habits by asking yourself key questions: Is this a need or a want? If it is a want, can it wait, or is it something that you should purchase immediately? In addition, do some comparative shopping. Be sure that you’re getting the best price for the items you buy — and for the credit you use. Are you receiving the lowest available interest rate on your credit cards? If you’re paying 21% while you could be paying 12%, you are doing yourself a disservice and throwing away your money.

Protect your family financially

If you’ve started a family, be sure that you have adequate life insurance to protect them in the event of your death. This is especially important if you have small children, because you want to provide for their future. Your children’s financial needs will continue, and they’ll need money for their everyday expenses such as housing, clothing and food. You may also want to help ensure opportunities for a brighter future by providing enough money to assist with endeavors such as going to college, buying a car or starting a business.

You can find affordable term life insurance policies. These are basic, no-frills policies with a set duration of coverage, usually up to 30 years. You could also purchase policies for an indefinite term or with additional features. For instance, a whole life policy remains in force until death, but can be significantly more expensive than a policy that lasts for a specific number of years. Talk to your financial advisor and/or insurance agent to determine the type and amount of coverage you need.

Consider homeownership

Owning a home has long been considered a foundation of wealth creation. It’s one of the most important steps you can take toward financial wellness. If you plan on living in an area for over five years and you can afford to buy a home, it’s something you should certainly consider. As a homeowner, you can build equity and take advantage of tax benefits such as mortgage interest and property tax deductions. But homeownership isn’t for everyone. If you prefer flexibility and don’t plan to live in the same place or you don’t want the responsibility of owning a home, it may not be right for you.

Start early

The earlier you establish these practices and pillars of financial security, the more possibilities and freedom you will have later in life. Developing sound financial principles now will ensure that you and your family can weather financial storms and achieve true success.

Pursuing a master’s degree is exciting, but it can also be expensive, even after scholarships and financial aid are factored in. If you’ve been burning to hit the books, these tips will make it easier to pay for grad school.

Pursuing a master’s degree is exciting, but it can also be expensive, even after scholarships and financial aid are factored in. If you’ve been burning to hit the books, these tips will make it easier to pay for grad school.

Give yourself time

It’s tough to accumulate the average $30,000 to $40,000 needed for grad school tuition. Allow a year or two to save, budget and plan rather than jumping right in.

Save smart

Establish a grad school fund and commit to depositing a set amount at regular intervals. Some sound education investment choices include:

529 savings plans: Money grows tax-free but must be used for qualified educational expenses.

529 prepaid tuition plans: These tax-free plans allow you to pay tuition in advance to avoid future rate hikes. Money must be used for tuition at the chosen school.

Certificates of deposit: These federally insured certificates offer higher returns than traditional savings accounts in return for leaving funds on deposit for a specified term. The money can be used for anything.

Savings and money market accounts: This choice offers the most liquidity, but rates tend to be lower than other options. There are no restrictions on how the money can be used.

Take advantage of tax breaks

Once you’re enrolled, Uncle Sam can help in two ways:

Lifetime learning credit: This tax credit refunds 20% of qualified educational expenses up to $10,000 for a maximum student benefit of $2,000 annually.

Tuition and fees deduction: Deduct up to $4,000 of qualified educational expenses annually.

Boost your cash flow

To create a cash surplus while saving for and attending grad school:

Enjoy more home-cooked meals and dine out less frequently.

Reduce entertainment expenses by exploring local parks, free concerts and neighborhood sporting events.

Sell unwanted items online or at yard sales.

Turn hobbies and interests into side income.

Shop around for the best deals on insurance, mobile phone, bank accounts and utilities.

If things are still tight, remember that you aren’t limited to choosing between full-time studies or none at all. Attending school part time over a longer period could make budgeting and work-study balance easier.

/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svg00Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2017-08-09 20:29:002023-06-16 12:49:22Budgeting and Planning for a Master’s Degree

Shopping for school supplies, electronics and clothing can be a chore — and an expensive one at that.

Families with children in grades K-12 plan to spend an average of $687.72 on back-to-school shopping, about $14 more than last year’s average of $673.57, according to the National Retail Federation. College students and their families plan to spend an average of $969.88, or about $82 more than last year’s $887.71 average.

Here’s a lesson on saving when back-to-school shopping online.

Shopping for school supplies, electronics and clothing can be a chore — and an expensive one at that.

Families with children in grades K-12 plan to spend an average of $687.72 on back-to-school shopping, about $14 more than last year’s average of $673.57, according to the National Retail Federation. College students and their families plan to spend an average of $969.88, or about $82 more than last year’s $887.71 average.

Incentives such as discounts and free shipping make online shopping an attractive option.

“Retailers are trying to cater to everything that will make the consumer happy,” says Ana Serafin Smith, senior director of media relations at the NRF.

Here’s a lesson on saving when back-to-school shopping online.

Go bargain hunting

You wouldn’t want to buy a pack of notebooks only to spot the same item elsewhere for half the cost. Fend off buyer’s remorse by shopping around before you click the “order” button. Google Shopping can help you compare the costs of items on your list between retailers, or find coupons with a browser extension like Honey. Remember to factor shipping costs into the comparison.

Ask for a price match

If you find separate retailers selling an identical item at different prices, or if there’s a discrepancy between the same retailer’s prices in store and online, ask the site with the higher price for a reduction.

Retailers with price-matching policies — including Target, Best Buy and Newegg — will honor a competitor’s lower advertised price or reimburse you the difference on eligible items if you can provide proof of the amount within a specific time frame. At Staples, you’ll get the lower price plus 10% of the difference. Call the retailer’s customer service number for help price matching your online order.

Pursue student discounts

Students — and sometimes parents, faculty and staff — can save or score freebies by shopping on sites with student discounts or promotions. For example, Apple is discounting select Macs by up to $300 and the iPad Pro by up to $20, plus throwing in wireless Beats headphones for free with eligible purchases through Sept. 25. Check other retailers or student discount networks like Unidays for deals on electronics, supplies, clothing and more.

Buy online, pick up in store

If you order back-to-school supplies online and pick them up in store, many retailers will give you free shipping or order discounts, or will send you a coupon for a future purchase. On Walmart’s website, look for items marked “free pick up and discount”: At the time of this writing, we spotted an Acer touchscreen laptop for $251.65 with a $67.93 pickup discount, lowering the price to $183.72.

Rent materials or buy used

Newer isn’t necessarily better, at least not for your wallet. You can save on textbooks, calculators, clothing and other back-to-school staples by renting or buying them used. Explore options and pricing on sites such as Chegg, Amazon and Poshmark.

Bypass sales tax

This year, more than a dozen states are waiving sales tax on eligible back-to-school items — such as clothing, books and laptops under a certain amount — during sales tax holidays. Some areas waive local sales tax, too. These events typically last for a few days in late July or early August, both in stores and online. For example, Ohio and Virginia both offer tax-free weekends Aug. 4-6. If you live in a participating state, consider timing your back-to-school purchases around the holiday, and check the list of tax-exempt items and cost limits first.

You can still strategically time back-to-school purchases if your state doesn’t take part or you miss the window. The shopping season’s peak savings usually last through August into September, closer to the start of the school year.

The article Save More When Back-to-School Shopping Online originally appeared on NerdWallet.

/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svg00Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2017-08-01 13:55:002023-06-16 12:49:22Save More When Back-to-School Shopping Online

Think about the effort it takes to search for the right new car and to negotiate the lowest price. Here are a few things to consider while looking for the best financing option.

Think about the effort it takes to search for the right new car and to negotiate the lowest price.

Unless you plan to pay cash in full, the third leg of the stool is finding the best possible financing. Because loans typically come in 12-month increments, we’re talking about a decision that will affect your household budget a minimum of two years and probably more like five or six.

Here are a few things to consider while looking for the best financing option:

Assess your credit

Your credit score is likely the single biggest factor a lender will consider in determining what interest rate to offer you. Your score is based primarily on your credit reports, which you can get for free by visiting AnnualCreditReport.com.

Check the reports for errors and take action to dispute any that you find, because a higher credit score usually leads to a lower interest rate on a loan.

Get preapproved for a loan

Borrowing options usually boil down to working with a financial institution or with the dealership. Too many people assume the latter is their only option. But you can find a loan at banks as well.

For customers with excellent credit, dealerships sometimes offer low- or even no-interest rates. On the other hand, dealers’ rates can be markedly worse than those available elsewhere.

If you go through a bank, ask for a preapproval letter. Walking into the dealership with that in hand gives you more bargaining power to negotiate a better price.

Decide what to do with your old car

If you have a vehicle already, trading it in may be enough to cover a down payment or at least serve as a credit against the cost of your new ride. Sites such as Kelley Blue Book and Edmunds can help you appraise the trade-in value.

The dealer may well offer less — sometimes substantially less — than you could get by selling your old car privately. The tradeoff is you’ll have the inconvenience and uncertainty of dealing with strangers.

Figure out how much you can afford

Take a look at your financial situation to determine how much vehicle you can afford. What other living expenses, such as mortgage or rent, utilities and other recurring payments already have a claim on your income?

When calculating costs, you might also check with your insurance agent about rates. Why? Because in addition to your driving record, insurance rates can vary depending on a vehicle’s maintenance costs as well as the history of claims tied to your specific make and model.

Buying a new car is a major financial commitment, typically second only to purchasing a home. Taking time to figure out how much car you can afford and finding the smartest financing are well worth the effort.

/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svg00Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2017-06-29 15:21:002023-06-16 12:53:31Financial Steps to Take Before Buying a Car