Kate Bray joined our team in the first quarter of 2021 and quickly became a client favorite. She is currently an Investment Relationship Specialist working closely with Matt Robinson. Her positive energy and eagerness to assist clients helped her obtain all her securities licensing within one year of joining our team. We recently sat down with Kate to reflect on her first year with F&M and learn more about what makes her shine.

What makes Kate, Kate?

I grew up here in Harrisonburg and graduated from Turner Ashby (04). I graduated from George Mason (08) and lived outside of DC for a few years after college working as an executive assistant at a large consulting firm. At 25 I decided to move back to town to purchase and run Cinnamon Bear Bakery & Deli, a small local restaurant and did that for 6 years. After that, I worked for two years as a paralegal and have now landed in my true destined field of financial services. I have a husband, Greg, and an energetic, sweet, and wonderful 6-year-old son, Luke. In my spare time, I love to go to local restaurants & wineries, watch Bravo, go to OrangeTheory, play roller derby, and take my son around to his miscellaneous activities. I like food, wine, tv, and laughing, and I find it very difficult to take anything in life too seriously.

Where are you from?

Harrisonburg, VA

What behavior or personality trait do you most attribute your success to, and why?

Positive thinking and adaptability to work with different personalities and understand where people are coming from to accomplish collective goals.

How do you start your day?

Coffee

What’s a work-related accomplishment that you’re proud of?

I am proud of accomplishing all my securities licensing within a year of coming to F&M Financial Services.

What’s your guilty pleasure?

I love the Real Housewives franchise on Bravo.

Do you have a hidden talent? What is it?

I love to cater parties.

What’s the top destination on your must-visit list?

Fiji

If you could choose a superpower, what would it be?

Telepathy

Share the best piece of advice anyone has ever given you.

Don’t apologize when an apology is not needed or apologize for someone else’s mistake. Take accountability to correct any mistakes you’ve made.

Manifest Destiny.

What activities do you participate in over the weekend?

Roller Derby

Exercise / Kickboxing

Get together with friends at fun local places

List three items on your bucket list

Visit every continent

See a bioluminescent bay

Attend Food & Wine classic in Aspen

If you could quickly and easily learn any new skill, what would it be?

Divination

Kate Bray is a Registered Representative, Osaic Institutions, Inc.

Investment and insurance products and services are offered through Osaic Institutions, Inc., Member FINRA/SIPC. F&M Financial Services is a trade name of F&M Bank. Osaic Institutions and F&M Bank are not affiliated.

Securities and Insurance Products:

Not Guaranteed by the Bank | Not FDIC Insured | Not a Deposit | Not Insured by Any Federal Government Agency | May Lose Value Including Loss of Principal

/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svg00Jacob Mowry/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgJacob Mowry2022-05-03 13:26:562023-11-07 14:07:11Meet Our Advisors: Kate Bray

Conventional wisdom says that what goes up must come down. But even if you view market volatility as a normal occurrence, it can be tough to handle when your money is at stake. Though there’s no foolproof way to handle the ups and downs of the stock market, the following common-sense tips can help.

Don’t put your eggs all in one basket

Diversifying your investment portfolio is one of the key tools for trying to manage market volatility. Because asset classes often perform differently under different market conditions, spreading your assets across a variety of investments such as stocks, bonds, and cash alternatives has the potential to help reduce your overall risk. Ideally, a decline in one type of asset will be balanced out by a gain in another, though diversification can’t eliminate the possibility of market loss.

One way to diversify your portfolio is through asset allocation. Asset allocation involves identifying the asset classes that are appropriate for you and allocating a certain percentage of your investment dollars to each class (e.g., 70% to stocks, 20% to bonds, 10% to cash alternatives). A worksheet or an interactive tool may suggest a model or sample allocation based on your investment objectives, risk tolerance level, and investment time horizon, but that shouldn’t be a substitute for expert advice.

Focus on the forest, not on the trees

As the market goes up and down, it’s easy to become too focused on day-to-day returns. Instead, keep your eyes on your long-term investing goals and your overall portfolio. Although only you can decide how much investment risk you can handle if you still have years to invest, don’t overestimate the effect of short-term price fluctuations on your portfolio.

Look before you leap

When the market goes down and investment losses pile up, you may be tempted to pull out of the stock market altogether and look for less volatile investments. The modest returns that typically accompany low-risk investments may seem attractive when more risky investments are posting negative returns.

But before you leap into a different investment strategy, make sure you’re doing it for the right reasons. How you choose to invest your money should be consistent with your goals and time horizon.

For instance, putting a larger percentage of your investment dollars into vehicles that offer asset preservation and liquidity (the opportunity to easily access your funds) may be the right strategy for you if your investment goals are short term and you’ll need the money soon, or if you’re growing close to reaching a long-term goal such as retirement. But if you still have years to invest, keep in mind that stocks have historically outperformed stable-value investments over time, although past performance is no guarantee of future results. If you move most or all of your investment dollars into conservative investments, you’ve not only locked in any losses you might have, but you’ve also sacrificed the potential for higher returns. Investments seeking to achieve higher rates of return also involve a higher degree of risk.

Look for the silver lining

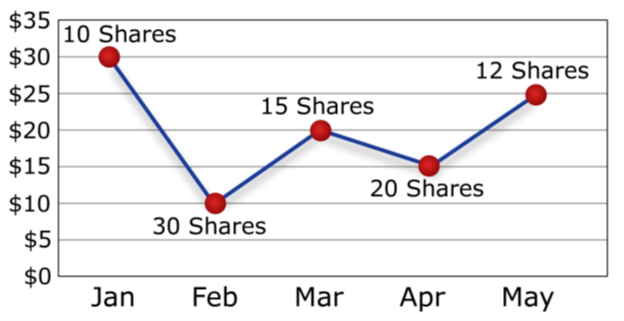

A down market, like every cloud, has a silver lining. The silver lining of a down market is the opportunity to buy shares of stock at lower prices. One of the ways you can do this is by using dollar-cost averaging. With dollar-cost averaging, you don’t try to “time the market” by buying shares at the moment when the price is lowest. In fact, you don’t worry about price at all. Instead, you invest a specific amount of money at regular intervals over time. When the price is higher, your investment dollars buy fewer shares of an investment, but when the price is lower, the same dollar amount will buy you more shares. A workplace savings plan, such as a 401(k) plan in which the same amount is deducted from each paycheck and invested through the plan, is one of the most well-known examples of dollar-cost averaging in action.

For example, let’s say that you decided to invest $300 each month. As the illustration shows, your regular monthly investment of $300 bought more shares when the price was low and fewer shares when the price was high:

Although dollar-cost averaging can’t guarantee you a profit or avoid a loss, a regular fixed dollar investment may result in a lower average price per share over time, assuming you continue to invest through all types of market conditions.

(This hypothetical example is for illustrative purposes only and does not represent the performance of any particular investment. Actual results will vary.)

Making dollar-cost averaging work for you

Get started as soon as possible. The longer you have to ride out the ups and downs of the market, the more opportunity you have to build a sizable investment account over time.

Stick with it. Dollar-cost averaging is a long-term investment strategy. Make sure you have the financial resources and the discipline to invest continuously through all types of market conditions, regardless of price fluctuations.

Take advantage of automatic deductions. Having your investment contributions deducted and invested automatically makes the process easy and convenient.

Don’t stick your head in the sand

While focusing too much on short-term gains or losses is unwise, so is ignoring your investments. You should check your portfolio at least once a year —more frequently if the market is particularly volatile or when there have been significant changes in your life.

You may need to rebalance your portfolio to bring it back in line with your investment goals and risk tolerance. Rebalancing involves selling some investments in order to buy others. Investors should keep in mind that selling investments could result in a tax liability. Don’t hesitate to get expert help if you need it to decide which investment options are right for you.

Don’t count your chickens before they hatch

As the market recovers from a down cycle, elation quickly sets in. If the upswing lasts long enough, it’s easy to believe that investing in the stock market is a sure thing. But, of course, it never is. As many investors have learned the hard way, becoming overly optimistic about investing during the good times can be as detrimental as worrying too much during the bad times. The right approach in all kinds of markets is to be realistic. Have a plan, stick with it, and strike a comfortable balance between risk and return.

Contact us today for an assessment.

Calan Jansen

Vice President at F&M Bank

Osaic Institutions Financial Advisor with F&M Financial Services, Inc.

Prepared by Broadridge Investor Communications Solutions, Inc.

Investment and insurance products and services are offered through Osaic Institutions, Inc., Member FINRA/SIPC. F&M Financial Services is a trade name of F&M Bank. Osaic Institutions and F&M Bank are not affiliated.

Securities and Insurance Products:

Not Guaranteed by the Bank | Not FDIC Insured | Not a Deposit | Not Insured by Any Federal Government Agency | May Lose Value Including Loss of Principal

TIMBERVILLE, VA—April 25, 2022—F & M Bank Corp. (OTCQX: FMBM), parent company (the Company) of Farmers & Merchants Bank today reported net income of $2.5 million for quarter ending March 31, 2022.

Mark Hanna, President, commented “First quarter of 2022 has been a strong quarter for F&M bank with net income of $2.5 million. Deposits grew this quarter another 2.96% and have been deployed into $3 million of net loan growth, excluding PPP and $58 million of new investments in bonds to capitalize on the rising rate environment. We continue to focus strategically on improving our infrastructure and enhancing our digital experience as we expand our reach to organically acquire new banking relationships. Our greater scale, coupled with improvements in asset quality, position F&M for continued success.”

Selected financial highlights include:

Net income of $2.5 million for the quarter ended March 31, 2022.

Total deposit increase of $32.0 million (2.96%) and $249.5 million (28.9%), respectively for the quarter and for the trailing twelve months.

Loans held for investment increase of $3.0 million (.46%) and $35.1 million (5.64%), respectively for the quarter and for the trailing twelve months (excluding PPP loans).

Nonperforming assets as a percent of total assets decreased to .39% from .45% at year end and .57% on March 31, 2021.

Past due loans still accruing decreased to 0.36% of loans held for investment (net of PPP) from 0.49% at year end and 0.52% on March 31, 2021.

Recovery of Provision for Loan Losses of $450,000 for the quarter.

Allowance for loan losses of 1.12% of loans held for investment, excluding PPP.

BALANCE SHEET

Loans

Loans held for investment; net of PPP have grown 5.64% since March 31, 2021. The Agriculture, C&I, CRE and dealer portfolios have experienced growth throughout the quarter and year to date, while the Company has seen a reduction in consumer loans specifically in the 1-4 family residential loan area.

LOAN PORTFOLIO

(dollars in thousands)

3/31/2022

12/31/2021

Change

3/31/2021

Change

Commercial

$ 290,452

$ 286,500

$ 3,952

$ 267,792

$ 22,660

Agriculture

82,460

81,879

581

70,556

11,904

Dealer

111,238

107,346

3,892

96,370

14,868

Consumer

169,617

173,556

(3,939)

183,046

(13,429)

Other

3,733

5,205

(1,472)

4,608

(875)

Loans held for Investment, net of PPP

$ 657,500

$ 654,486

$ 3,014

$ 622,372

$ 35,128

Investments

The Company has continued to leverage excess funds into the available for sale (AFS) investment portfolio in the first quarter of 2022 growing $57.9 million to $462 million. The portfolio is a strong mix of U.S. Treasuries, Agencies, Mortgaged-backed securities, Municipals, and Corporate bonds. The average tax equivalent yield on the portfolio is 1.54% which has equated to $1.5 million in income for the first quarter compared to $461 thousand in the same quarter last year.

AFS INVESTMENT PORTFOLIO

(dollars in thousands)

3/31/22

12/31/21

Change

3/31/21

Change

US Treasury

$ 42,868

$ 29,482

$ 13,386

$ 29,421

$ 13,447

Agency

158,540

133,714

$ 24,826

24,877

$ 133,663

Mortgage-Backed Securities

197,594

183,647

$ 13,947

85,406

$ 112,188

Municipals

32,674

34,337

$ (1,663)

20,692

$ 11,982

Corporates

30,146

22,702

$ 7,444

11,307

$ 18,839

Total Securities

$ 461,822

$ 403,882

$ 57,940

$ 171,703

$ 290,119

Securities Quarterly Income

$ 1,497

$ 1,102

$ 395

$ 461

$ 1,036

Deposits

The Company’s deposit growth during the first quarter of 2022 has been in noninterest bearing accounts ($17.6 million) and money market accounts and savings accounts ($21.1 million) with a decline in NOW and other transactional accounts ($3.6 million) and time deposits ($3.2 million). The Company continues to strategically focus on building primary banking relationships.

DEPOSIT PORFOLIO

(dollars in thousands)

3/31/22

12/31/21

CHANGE

3/31/21

CHANGE

Non Interest Bearing

$ 298,676

$ 280,993

$ 17,683

$ 252,265

$ 46,411

NOW & Other Transactional

188,342

191,969

(3,627)

119,076

69,266

Money market and Savings

504,611

483,476

21,135

363,377

141,234

Certificates of deposit

120,666

123,857

(3,191)

128,034

(7,368)

Total Deposits

$ 1,112,295

$ 1,080,295

$ 32,000

$ 862,752

$ 249,543

Asset Quality

Nonperforming loans as a percent of total assets (net of PPP) continue to decline from 0.57% on March 31, 2021 to 0.39% at March 31, 2022. In addition, classified loans and past due loans declined from the previous twelve months from 9.69% to 6.17% and 0.52% to 0.36%, respectively (net of PPP).

(dollars in thousands)

3/31/2022

12/31/2021

3/31/2021

Non-performing Loans

Non-accrual loans

$ 4,751

$ 5,465

$ 5,755

Over 90 & on Accrual

48

43

28

Total Non-performing Loans

$ 4,799

$ 5,508

$ 5,783

NPL As A % of Total Assets, net of PPP

0.39%

0.45%

0.57%

Watch Total

$ 21,901

$ 24,140

$ 30,681

As A % Of Loans, net of PPP

3.31%

3.67%

4.88%

Substandard Total

$ 18,969

$ 19,713

$ 30,179

As A % Of Loans, net of PPP

2.86%

2.99%

4.80%

Total Watch List

$ 40,870

$ 43,853

$ 60,860

Total Classified As A % of Total Loans, net of PPP

6.17%

6.66%

9.69%

Past Due Loans

30-59 Days Past Due

$ 2,093

$ 2,751

$ 2,730

60-89 Days Past Due

273

432

495

90+ Days Past Due

48

43

28

Total Past Due Loans

$ 2,414

$ 3,226

$ 3,253

Deliquency %, net of PPP

0.36%

0.49%

0.52%

Allowance for Loan and Lease Losses

The allowance for loan losses as a percentage of loans held for investment, net of PPP has declined from 1.56% at March 31, 2021 to 1.12% at March 31, 2022. This decline has been driven by improved asset quality in regard to non-performing, classified and past due loans. Uncertainty in the economy related to the war in Ukraine, inflation and supply chain issues were factored into the allowance for loan losses this quarter as well as growth in the portfolio over the trailing twelve months. The resulting reversal of provision was accretive to quarterly earnings by $450 thousand.

3/31/2022

12/31/2021

3/31/2021

(dollars in thousands)

Provision for Loan Losses

$ (450)

$ (590)

$ (725)

Allowance for Loan and Leases Losses

$ 7,389

$ 7,748

$ 9,704

ALLL as a % of Loans Held for Investment, net of PPP

1.12%

1.18%

1.56%

INCOME STATEMENT

Net Interest Income

Net interest income reflects growth over the year ended 12/31/21 and quarter ended 3/31/21 of $177 thousand and $380 thousand, respectively. As yields on earning assets continue to decline the Company has been able to support net interest income with savings in interest expense and growth in the investment portfolio while seeking opportunities to leverage the growth in liquidity into higher yielding assets. During the quarter the Company was able to purchase bonds as the market yields climbed. This should add to net interest income in future quarters.

Margin compression has reduced the net interest margin from 3.44% on March 31, 2021, to 2.82% on March 31, 2022. To mitigate this compression, the Company has continued to invest excess funds into securities with better yields. The Company has also slightly reduced cost of funds since March 31, 2021 to 34 basis points through maintaining deposit rates, debt reduction and growth in noninterest bearing deposits.

Noninterest Income

Noninterest income of $2.5 million for the quarter was slightly higher than year end 12/31/21 of $2.4 million but a decline from March 31, 2021, which was $3.4 million. Mortgage originations have declined as rates have increased, as a result the Company is focused on expanding mortgage originators into our newer markets, continuing to utilize our title company and growing our wealth management division.

Noninterest expense

Focusing on infrastructure enhancements, digital processes and expanding into our newer markets has resulted in growth in noninterest expense of 11.25% in the trailing twelve months. Some of the growth is attributed to the charitable donation of a property to the local community, disposing of non-income producing properties and eliminating outdated products.

Paycheck Protection Program

The Company processed 1,080 Paycheck Protection Program (“PPP”) & CARES Act loans during 2020 and 2021 totaling $87.1 million. Fees associated with these loans are amortized over the life of the loan or recognized fully when repaid or forgiven. The Company holds $2.1 million in PPP loans as of March 31, 2022 and recognized $169,000 in PPP fee income in the first quarter.

Dividends Declaration

On April 21, 2022, our Board of Directors declared a fourth quarter dividend of $.26 per share to common shareholders. Based on our most recent trade price of $30.00 per share this constitutes a 3.47% yield on an annualized basis. The dividend will be paid on May 30, 2022, to shareholders of record as of May 15, 2022.”

F & M Bank Corp. is an independent, locally owned, financial holding company, offering a full range of financial services, through its subsidiary, Farmers & Merchants Bank’s thirteen banking offices in Rockingham, Shenandoah, and Augusta Counties, Virginia and the city of Winchester, VA. The Bank also provides additional services through a loan production office located in Penn Laird, VA, a loan production office in Winchester, VA and through its subsidiaries, F&M Mortgage and VSTitle, both of which are located in Harrisonburg, VA. Additional information may be found by contacting us on the internet at www.fmbankva.com or by calling (540) 896-1705.

F & M Bank Corp.

Key Statistics

2022

2021

Q1

Q4

Q3

Q2

Q1

Net Income (000’s)

$ 2,528

$ 1,380

$ 2,337

$ 3,220

$ 3,801

Net Income available to Common

$ 2,528

$ 1,379

$ 2,272

$ 3,154

$ 3,736

Earnings per common share – basic

$ 0.74

$ 0.39

$ 0.71

$ 0.98

$ 1.17

Earnings per common share – diluted

$ 0.74

$ 0.40

$ 0.68

$ 0.93

$ 1.11

Return on Average Assets

0.89%

0.46%

0.81%

1.22%

1.56%

Return on Average Equity

10.51%

5.42%

9.18%

13.06%

15.96%

Dividend Payout Ratio excluding Special Dividend

35.14%

66.67%

36.62%

26.53%

22.22%

Net Interest Margin

2.82%

2.48%

2.95%

3.13%

3.44%

Yield on Average Earning Assets

3.17%

3.15%

3.35%

3.56%

3.92%

Yield on Average Interest Bearing Liabilities

0.49%

0.96%

0.57%

0.62%

0.70%

Net Interest Spread

2.68%

2.19%

2.78%

2.94%

3.22%

Provision for Loan Losses (000’s)

$ (450)

$ (590)

$ (235)

$ (1,250)

$ (725)

Net Charge-offs

$ (92)

$ 72

$ 61

$ (272)

$ 45

Net Charge-offs as a % of Loans

-0.01%

0.04%

0.04%

-0.16%

0.03%

Non-Performing Loans (000’s)

$ 4,799

$ 5,508

$ 5,430

$ 5,532

$ 5,783

Non-Performing Loans to Total Assets

0.39%

0.45%

0.46%

0.50%

0.57%

Non-Performing Assets (000’s)

$ 4,799

$ 5,508

$ 5,430

$ 5,532

$ 5,783

Non-Performing Assets to Assets

0.39%

0.45%

0.46%

0.50%

0.57%

Efficiency Ratio

78.68%

82.13%

75.99%

76.07%

68.00%

(1) The net interest margin is calculated by dividing tax equivalent net interest income by total average earning assets. Tax equivalent interest income is calculated by grossing up interest income for the amounts that are nontaxable (i.e. municipal securities and loan income) then subtracting interest expense. The tax rate utilized is 21%. The Company’s net interest margin is a common measure used by the financial service industry to determine how profitable earning assets are funded. Because the Company earns nontaxable interest income from municipal loans and securities, net interest income for the ratio is calculated on a tax equivalent basis as described above.

(2) The efficiency ratio is not a measurement under accounting principles generally accepted in the United States. The efficiency ratio is a common measure used by the financial service industry to determine operating efficiency. It is calculated by dividing non-interest expense by the sum of tax equivalent net interest income and non-interest income excluding gains and losses on the investments portfolio and Other Real Estate Owned. The Company calculates this ratio in order to evaluate how efficiently it utilizes its operating structure to create income. An increase in the ratio from period to period indicates the Company is losing a greater percentage of its income to expenses.

This press release may contain “forward-looking statements” as defined by federal securities laws, which may involve significant risks and uncertainties. These statements address issues that involve risks, uncertainties, estimates and assumptions made by management, and actual results could differ materially from the results contemplated by these forward-looking statements. Factors that could have a material adverse effect on our operations and future prospects include, but are not limited to, changes in interest rates, general economic conditions, legislative and regulatory policies, and a variety of other matters. Other risk factors are detailed from time to time in our Securities and Exchange Commission filings. Readers should consider these risks and uncertainties in evaluating forward-looking statements and should not place undue reliance on such statements. We undertake no obligation to update these statements following the date of this press release.

TIMBERVILLE, Va. (April 25, 2022) – On Monday, April 18, F&M Bank continued its growth in Winchester with a new banking center located in historic Old Town Winchester. This is F&M Bank’s 13th branch in Virginia. Later in 2022, a second Winchester branch location is slated to open west of Old Town on Amherst Street.

F&M Bank identified Winchester as a strategic growth opportunity due to its thriving local economy, prospering businesses, robust non-profit network, and a community that’s committed to preserving its history while at the same time looking to the future.

“As a bank with more than 100 years of history we look to do business with people and communities that align with our values – and for us, Winchester is a perfect match,” said Mike Wilkerson, Chief Lending Officer and Winchester Market Executive. “The ‘Top of Virginia’ is thriving and our sweet spots of agriculture, non-profit and business banking reflect the needs of our community. In a world of bank consolidation and branch closures, F&M is committed to organic growth and market expansion. When we expand our ability to serve our customers, everybody wins.”

In January 2021, F&M Bank opened a commercial banking and loan production office in the Winchester market with an experienced banking team that has a 20-year history of working together. This northern Shenandoah Valley market has accrued over $36 million in deposits and $21 million in loans. Mr. Wilkerson leads the team, consisting of John Sargent, SVP, and Jonathan Reimer, SVP, Commercial Relationship Managers; and Gail Pryde, Business Relationship Specialist.

Today, with the announcement of its Old Town location opening, this team is excited to leverage their 150 years of combined banking experience to deliver customized loan, deposit, and cash management solutions to business and personal customers.

Lauren Fravel has been named as Banking Center Specialist for the Old Town Winchester location. Lauren brings over 25 years of experience to the team and is eager to welcome new customers. The banking center will also employ associates for F&M Mortgage and VS Title in the coming months.

The branch is located at 3 South Cameron Street, at the corner of Boscawen and Cameron Streets. Hours are 8:30am am to 5:00 pm with extensive digital offerings available online and on the F&M Bank mobile app.

https://www.fmbankva.com/wp-content/uploads/2021/08/downtown_0.png6201500Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2022-04-25 10:59:042024-03-08 10:22:00F&M Bank Opens Old Town Winchester Banking Center

Are you new to the Shenandoah Valley and having trouble deciding on where to bank? Unhappy with your current financial institution and looking to switch? Whether you’re looking for a financial institution for personal deposit accounts, mortgage financing, or business banking needs, it can be tough to decide whether to choose a large bank that you see across the country or a local bank with roots in your community, such as F&M Bank. In this article, we’ll help you understand what makes local financial institutions stand out, along with some perks of community banks that you may not be aware of.

What are the different types of financial institutions?

Banks are a crucial part of the U.S. monetary system because they move U.S. currency and provide necessary liquidity to personal and business entities. There are two sets of bank regulators, Federal and State. At the federal level, The Office of the Comptroller of the Currency (OCC), part of the Treasury, charters and supervises national banks. At the state level, banks that don’t work across state lines can be state-chartered. The FDIC oversees state-chartered banks that aren’t members of the Federal Reserve System.

F&M Bank can be traced to 1908, when it started its operation as a state-chartered bank; in 1983 F&M Bank was incorporated in Virginia and became a registered bank holding company. As a bank holding company it is a full-service financial institution, offering complete consumer, business, and financial services – including a full array of digital banking capabilities as well as physical branch locations for your banking needs (as opposed to institutions such as Internet-only banks and credit unions). You will even find that F&M Bank’s online services offer the same capabilities as national banks!

Internet banks: No physical branches, just a website and mobile banking app. Online banks may not have national charters themselves, instead partnering with a traditional bank to hold customer deposits.

Credit unions: Financial institutions that are owned by their members and have certain criteria for membership.

Differences between banks and credit unions

Working with a local financial institution like F&M Bank will likely be your best option. When deciding on where to open a bank account, consider some of the key differences between banks and credit unions:

Credit unions typically have fewer branch locations and financial products/services than banks.

Local community banks like F&M Bank benefit their community through local partnerships, events, and volunteer opportunities.

F&M Bank offers the most convenience and resources through digital banking on your mobile or other personal devices, along with a variety of options for nearby, conveniently located physical branch locations.

Local banks like F&M Bank offer unrivaled expertise related to your community, understanding how to resolve your specific needs for personal and business banking and lending that credit unions or nationwide banks are unable to provide.

Benefits of banking local for your personal deposit accounts

When it comes to your checking and savings accounts, it’s nice to have branch locations conveniently located near your house or job. And not just any branch, but one staffed with friendly employees who live and work in the same community as you. For example, F&M Bank has developed a lot of local expertise over the years. We’ve been supporting personal banking needs in the Shenandoah Valley since 1908. Local banks like F&M also offer branch services like on-site safe deposit boxes and in-house notary services.

Of course, web-based banking tools mean you don’t have to visit a branch just to deposit a check or transfer money between accounts. Local banks have embraced technology in recent years and now offer the same tools as the bigger banks. Enjoy the convenience of banking where and how you want with online banking, mobile banking, person to person payments, and mobile wallet. F&M Bank’s rating in the App Store is 4.8 out of 5 stars – higher than you will find for other options both nationally and locally.

Benefits of banking local for your lending needs

Applying for a loan can be stressful, especially if it’s your first time. The friendly loan officers at your local bank can guide you through the process, turning it from stressful to smooth and pleasant. Whether a home, car, or personal loan, they’ll help you review your options to find the right loan with a payment plan you can afford.

Mortgage Lending

While there are national trends in real estate, it’s still a very local business. The housing market can vary widely from community to community, so working with a local mortgage lender gives you access to local expertise, as well as more flexible lending options. Learn more about the mortgage loans offered by F&M Bank.

Personal Loans

Whether you need an Auto Loan to finance the purchase of your next vehicle, or a general consumer loan to use for a variety of expenses, local decision-making helps you get the right loan. Enjoy swift and local application processing, and greater flexibility in approving loans, from your local bank. When you come to a local lender like F&M Bank, we aim to put you at ease with the loan application process. Learn more about our personal loans.

Benefits of staying local for Wealth Management

Choosing a financial advisor is all about trust. Will they put your best interests first? Do they have experience working with clients who share your background, such as small business owners, blended families, etc.? Whether you are in Harrisonburg or closer to Broadway and Edinburg, you can find local financial advisors who will offer a higher level of service and possess a wealth of local knowledge.

Staying local for Wealth Management means working with a financial advisor who understands your community and can recommend local investment opportunities such as those on our Local Market Dashboard.

Investment and insurance products and services are offered through Osaic Institutions, Inc., Member FINRA/SIPC. F&M Financial Services is a trade name of F&M Bank. Osaic Institutions and F&M Bank are not affiliated.

Securities and Insurance Products:

Not Guaranteed by the Bank | Not FDIC Insured | Not a Deposit | Not Insured by Any Federal Government Agency | May Lose Value Including Loss of Principal

Bank local with F&M!

Now that you understand the benefits of banking locally, you probably want to find a local financial partner who understands your needs. At F&M Bank, you’ll find personalized attention with customizable solutions for your personal banking needs. In-house decision-making simplifies loan applications and local financial planners understand the community they serve. Get started now! Contact us or visit your nearest branch location in Harrisonburg, Augusta County, or Staunton in the Shenandoah Valley.

https://www.fmbankva.com/wp-content/uploads/2022/04/845x295-Header-drop-shadow.png295845Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2022-04-12 12:40:202024-09-24 09:05:44Should I Bank Local in Virginia? What to Consider When Choosing a Financial Institution

National Ag Day is March 22, 2022! Virginia’s agricultural production is one of the most diverse in the nation. Many Virginia commodities and products rank in the top 10 among all U.S. states. Our local farmers, and other agriculture experts, represent a leading group of industry movers and shakers that support our economy and sustain life for our region, and beyond.

Virginia is home to over 43,000 farms that cover nearly 8 million acres across the Commonwealth. 98% of all farms in the United States are family-owned and operated. These families sacrifice a lot to feed our communities and sustain life throughout our region. F&M strives to thank farmers throughout the year and we encourage our community to take a moment next week to thank a local farmer as we celebrate our farming community!

F&M has been supporting local farmers for over 100 years. We’ve helped farmers navigate several economic cycles from recessions and droughts to boom periods with flourishing production. These experiences and partnerships have helped us develop tailored products that include equipment financing, land expansion, cattle purchases, waste management funding, and lines of credit.

https://www.fmbankva.com/wp-content/uploads/2020/05/Farming-image-1-scaled.jpg14762560Jacob Mowry/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgJacob Mowry2022-03-18 10:12:232023-09-29 12:33:37National Ag Day with F&M Bank

Looking for investment help in the Shenandoah Valley? You’ve come to the right place. At F&M Financial Services, we know that investing can feel intimidating when you’re not familiar with the various investment options and terminology. In this article, we’ll cover the basics of building a diversified investment portfolio. From defining common terms to explaining different approaches to investing, you’ll have a better understanding of your investment portfolio. Of course, if you have specific questions or need advice about your portfolio, contact one of our Osaic Institutions Financial Advisors in Harrisonburg, Rockingham County, and Shenandoah County.

Where can I monitor stock values?

Local investors in the Shenandoah Valley can find a real-time market report and see our 14 most popular stocks on the Local Market Dashboard page. Looking for local investing help? Consider investing in local publicly-owned businesses with roots in the Shenandoah Valley. The dashboard provides a bird’s eye view of current share prices on the most popular local stocks, as well as important national indicators such as the Dow Jones Industrial Average, S&P 500, and NASDAQ Composite.

How to diversify your investments

Generally, diversifying* your investment portfolio is a reasonable approach to realizing steady long-term growth of your finances. Understand your various investment options and how they could support your investment goals:

What is a stock?**

Individual stocks represent a share of ownership in a publicly-traded company. Investors can buy stocks ‘a la carte” in the hope that they will increase in value over time. For example, investors who purchased individual Apple stock in 1980 would have seen their bet pay off very well in the years since, if they held onto it.

However, not every bet pays off and it’s hard to know at the Initial Public Offering which companies will become wildly successful like Apple or Tesla, and which will flame out. That’s why many investors prefer to mitigate the risk of individual stock values by investing in index funds or ETFs.

For example, the Dow Jones is a stock market index tracking 30 of the largest blue-chip companies on the stock exchange. You could choose an ETF (Exchange-Traded Fund) that tracks the Dow Jones. ETFs provide broad market exposure to potentially give your portfolio more stability and less risk.

Similarly, the S&P 500 is a stock market index following 500 of the top publicly traded U.S. companies. You can invest in index funds and ETFs that track the S&P.

Lastly, the Nasdaq Composite Index features stocks that are exclusively listed on the Nasdaq stock exchange. It is more tech-heavy than the Dow or S&P and the total number of stocks in the Nasdaq can change often.

What is a bond?

A bond is a unit of corporate debt that can be traded as an asset. Bonds are considered less risky than stocks to invest in because bonds have a fixed interest rate. However, the trade-off for that stability is usually a lower rate of return. That’s why building a diversified portfolio means having both higher-risk/higher-rate-of-return assets like stocks as well as more reliable/lower-rate-of-return assets like bonds.

What is a Mutual Fund?***

Unlike index funds and ETFs, which are not actively managed and only follow stocks, a mutual fund is defined by the U.S. Securities and Exchange Commission as:

A mutual fund is a company that pools money from many investors and invests the money in securities such as stocks, bonds, and short-term debt. The combined holdings of the mutual fund are known as its portfolio. Investors buy shares in mutual funds. Each share represents an investor’s part ownership in the fund and the income it generates.

Because mutual funds already contain a diversified portfolio of stocks, bonds, and short-term debt, buying shares in a mutual fund can be an easy way to diversify your own portfolio.

When it comes to index funds and ETFs vs. mutual funds, one of the main differences is that the cost of management fees tends to be lower for ETFs on average when compared to Mutual Funds. Mutual funds are sold by prospectus only, which may be obtained from a financial professional and should be read carefully before investing. Investors should consider the risks, investment objectives, fees, expenses, and charges disclosed in the prospectus.

CDs, Savings Accounts, and Money Market Accounts

As you approach retirement age, you’ll want to keep a portion of your investment portfolio in a more liquid account where you can earn some interest while having access to the next year or two of cash for living expenses. F&M Bank offers Certificates of Deposit (CDs), Free and Premium Savings Accounts, and Money Market to meet your liquidity needs.

Should I include Real Estate in My Investment Portfolio?

During your investment research, you may have heard of the 20% rule. If you are unfamiliar, the idea is that some investors find value in allocating at least 20% of your portfolio into investments that are outside of the stock market itself. It is popular for many investors to fill this 20% with real estate. This is not a hard and fast rule, however. Some investors may be more comfortable with a smaller or larger percentage of their funds being in real estate. Regardless, it can be a good idea to consider this as a piece of your overall investing strategy. Our financial advisors can help you understand what allocation would be the best fit for you. You also can learn more about F&M Bank’s mortgage lending options to get started with funding a real estate purchase.

Consider Your Risk Tolerance

We’ve covered the risk levels of various investment vehicles such as stocks, bonds, and mutual funds. But you also need to consider your personal tolerance for risk when deciding how much of your portfolio to allocate to different types of investments.

How much time do you have?

Generally, the younger you are the more aggressive you can afford to be with risk. A temporary setback can be overcome with time, while someone close to retirement will want to be more moderate or conservative. However, age isn’t the only factor to consider. Your comfort level with risk, long-term investment goals, and current income are also important.

As a general rule of thumb, a portfolio for each risk level would look like:

Aggressive: About 80% stocks and 20% bonds

Moderate: About 50% stocks and 50% bonds

Conservative: About 20% stocks and 80% bonds

Contact our financial advisors in the Shenandoah Valley to discuss your personal risk tolerance and how to diversify your portfolio accordingly.

Build your investment portfolio with a team you trust!

If you’re looking for Wealth Management services in Virginia, our financial planners guide you through your options for how to invest your money in VA to ensure you understand your investment portfolio and are comfortable with our strategy. Schedule an appointment with an Osaic Institutions Financial Advisor with F&M Financial Services at any of our locations today!

*Diversification is a method of helping to manage risk. It does not assure a profit or the avoidance of loss.

**Past performance is not a guarantee of future results.

*** Mutual funds are sold by prospectus only, which may be obtained from a financial professional and should be read carefully before investing. Investors should consider the risks, investment objectives, fees, expenses, and charges disclosed in the prospectus. Investment objectives, fees, expenses, and charges disclosed in the prospectus.

Investment and insurance products and services are offered through Osaic Institutions, Inc., Member FINRA/SIPC. F&M Financial Services is a trade name of F&M Bank. Osaic Institutions and F&M Bank are not affiliated.

Securities and Insurance Products:

Not Guaranteed by the Bank | Not FDIC Insured | Not a Deposit | Not Insured by Any Federal Government Agency | May Lose Value Including Loss of Principal

https://www.fmbankva.com/wp-content/uploads/2022/02/Building-a-Diverse-Portfolio.png218624Jacob Mowry/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgJacob Mowry2022-02-25 12:05:132023-11-07 14:21:41Building a Diverse Investment Portfolio: A Guide for New Investors in the Shenandoah Valley

Fishersville, February 16, 2021– As the premier business organization serving Augusta County, Staunton, and Waynesboro, the Greater Augusta Regional Chamber of Commerce represents over 550 diverse businesses that work together to stimulate the economy for this outstanding community. Through the annual Business Excellence Awards, the Chamber is able to recognize the outstanding success of exemplary businesses and individual leaders. Courtney Thompson, President & CEO of the Chamber said, “We are so excited to announce our Business Excellence award winners. We had numerous excellent businesses, organizations and individuals nominated this year and these winners really represent the best of the best.”

The Chamber is very proud to announce the winners of the 2022 Business Excellence Awards:

● New Business of the Year: RX Coffee & More

● Small Business of the Year: Staunton Innovation Hub

● Large Business of the Year: F & M Bank

● Woman Owned Business of the Year: SweetNanaCakes

● Nonprofit of the Year: Blue Ridge Area Food Bank

● Young Professional of the Year: Debbie Irwin, Shenandoah Community Capital Fund

● Citizen of the Year: Dan Layman, Community Foundation of the Central Blue Ridge

The Chamber will honor each of these winners and deliver its year in review at the Business Excellence Awards on March 10 at Hotel 24 South. For more information about the winners or the event, contact Courtney Thompson at (540) 324-1133 or courtney@augustava.com.

https://www.fmbankva.com/wp-content/uploads/2022/02/274156027_5453686581326141_6009974913926141155_n.png400700Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2022-02-18 13:54:232022-09-28 15:38:49F&M Bank Receives Greater Augusta County Chamber of Commerce’s Business Excellence Award

The third Tuesday in March was declared Bank Day by the Virginia General Assembly in 1991 and F&M Bank has been proud to host students for this important program. Each year this scholarship program awards local Virginia high school rising seniors the opportunity to spend time learning about the banking industry. F&M Bank members will educate these students on their job roles and the various bank departments; including the loan process, the importance of good credit, the profile of a qualified borrower, and how F&M Bank is involved in the community.

From their experience, participating students will write an essay for the chance to win a scholarship. Six regional scholarships of $2,500 each will be awarded, and from those six winners an overall statewide winner will be chosen. The statewide winner will receive an additional $5,000 scholarship – $7,500 in total. There will also be six honorable mention scholarships of $1,000 each. In all, twelve students will receive scholarships totaling $26,000.

If interested in signing up for the program, click here.

For more information, or if you have any questions, please contact Nicole Davis, Marketing Specialist, at ndavis@fmbankva.com or 540-437-3471.

https://www.fmbankva.com/wp-content/uploads/2022/02/iStock-973279516.jpg14142121Jacob Mowry/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgJacob Mowry2022-02-04 11:07:322022-09-28 14:54:16F&M Bank to Participate in the 2022 VBA Bank Day Scholarship Program

TIMBERVILLE, VA / ACCESSWIRE / January 26, 2022 / F & M Bank Corp. (OTCQX:FMBM), parent company (the Company) of Farmers & Merchants Bank today reported net income available to common shareholders of $10.5 million and diluted earnings per common share of $3.12 for the year ending December 31, 2021.

Mark Hanna, President, commented “We are pleased with December 31, 2021 year to date earnings of $10.5 million. These results represent the most profitable year in our 114-year history. Our deposit growth of 68.3% over the last two years is significantly higher than our peers and indicative of our ability to create organic growth. We continue to focus strategically on improving our infrastructure and enhancing our digital experience as we expand our reach to acquire new banking relationships. Our greater scale, coupled with improvements in asset quality, position F&M for continued success.”

Selected financial highlights include:

Net income of $1.3 million for the quarter ended December 31, 2021, and $10.5 million year to date.

Total deposit increase of $50.0 million (4.85%) and $261.7 million (31.97%), respectively for the quarter and for the year.

Total loan increase of $13.6 million (2.11%) and $31.9 (5.09%) million, respectively for the quarter and for the year (excluding PPP loans).

Nonperforming assets decreased to 0.45% of total assets at the end of the quarter from 0.68% at year end 2020.

Past due loans still accruing decreased to 0.48% of loans held for investment at the end of the quarter from 1.07% at year end 2020 (excluding PPP loans).

Recovery of Provision for Loan Losses of $590,000 for the quarter and $2,821,000 year to date.

Allowance for loan losses of 1.16% of loans held for investment (1.18% excluding PPP loans).

Balance Sheet

The Company has experienced significant deposit growth during the year. This growth enabled the Company to expand the investment portfolio as well as make strategic reductions in its long-term debt.

The Company’s deposit growth has continued to exceed peer performance going back to 2019. The growth has been in noninterest bearing accounts ($33.3 million), interest bearing demand ($71.6 million) and savings and money market accounts ($163 million) with a decline in time deposits ($6.2 million). The Company continues to strategically focus on building primary banking relationships.

The investment portfolio has expanded to a balance of $413.2 million at the quarter ended December 31, 2021, which reflects growth of $295.3 million since December 31, 2020. The portfolio is a strong mix of U.S. Treasuries, Agencies, Municipals, Corporate bonds and other investments. The Company recognized $525,000 in security losses in fourth quarter of 2021, as lower yielding securities were sold and replaced with higher yielding securities to position the Company for future success.

The Company prepaid several long term FHLB borrowings to leverage our liquidity and reduce our cost of funds in future periods. These borrowings were paid down $11.3 million year to date and have a remaining balance of $10 million.

Loans held for investment; net of PPP have grown 5.09% since December 31, 2020. The Agriculture, C&I, CRE and dealer portfolios have experienced growth throughout the quarter and year to date, while the Company has seen a reduction in loan balances on 1-4 family residential secured loans during this low-rate environment.

Improvements in nonperforming loans and past due loans, as well as economic stability and improved underwriting have allowed the Company to reduce the Allowance for Loan Losses from 1.64% on December 31, 2020, to 1.18% on December 31, 2021, excluding PPP loans.

These strategies have positioned F&M for future growth in our current footprint as we continue to evaluate opportunities for expansion.

Income Statement

The 2021 earnings are driven by growth in net interest income, strong non-interest income due to our subsidiary organizations, improved asset quality and fees earned under the Paycheck Protection Program.

Net interest income reflects year over year growth. As yields on earning assets continue to decline the Company has been able to support net interest income with savings in interest expense and growth in the investment portfolio while seeking opportunities to leverage the growth in liquidity into higher yielding assets.

Margin compression has reduced the net interest margin from 3.61% on December 31, 2020, to 3.00% on December 31, 2021. To mitigate this compression, the Company has decreased its cost of funds by 24 basis points through rate adjustments, debt reduction and growth in noninterest bearing deposits.

Noninterest income of $11.8 million for the year was primarily driven by mortgage originations, growth in our wealth management division, and title division. These entities have performed well and are preparing to expand into additional areas within our Company footprint in the near future.

As stated above, continued improvements in asset quality and economic conditions resulted in the ability to reduce the allowance for loan losses to 1.16% of loans held for investment (1.18% excluding PPP loans) which was accretive to income by $2.8 million year to date, and $590 thousand in the fourthquarter.

Fees recognized under the Paycheck Protection Program (see below) totaled $212,000 for the quarter and $2.10 million year to date.

This year the Company disposed of non-income producing properties creating a loss of $333,000 and renegotiated contracts with vendors resulting in one time increases in noninterest expense of $500,000 for 2021. These moves will better position the organization for the future.

Paycheck Protection Program

The Company processed 1,080 Paycheck Protection Program (“PPP”) & CARES Act loans during 2020 and 2021 totaling $87.1 million. Fees associated with these loans are amortized over the life of the loan or recognized fully when repaid or forgiven. The Company holds $7.9 million in PPP loans as of December 31, 2021 and expects to recognize approximately $225,000 in PPP fee income from these loans in 2022.

Preferred Stock Redemption

On September 1, 2021, the Company gave notice to preferred shareholders that it would redeem all Series A Preferred Stock on October 29, 2021. As a result of this announcement, 180,261 shares of the 205,327 shares of preferred stock converted to common shares and 25,066 shares were redeemed for cash.

Dividends Declaration

On January 21, 2022, our Board of Directors declared a fourth quarter dividend of $.26 per share to common shareholders. Based on our most recent trade price of $31.38 per share this constitutes a 3.31% yield on an annualized basis. The dividend will be paid on March 1, 2022, to shareholders of record as of February 14, 2022.”

F & M Bank Corp. is an independent, locally owned, financial holding company, offering a full range of financial services, through its subsidiary, Farmers & Merchants Bank’s thirteen banking offices in Rockingham, Shenandoah, and Augusta Counties, Virginia and the city of Winchester, VA. The Bank also provides additional services through a loan production office located in Penn Laird, VA, a loan production office in Winchester, VA and through its subsidiaries, F&M Mortgage and VSTitle, both of which are located in Harrisonburg, VA. Additional information may be found by contacting us on the internet at www.fmbankva.com or by calling (540) 896-1705.

This press release may contain “forward-looking statements” as defined by federal securities laws, which may involve significant risks and uncertainties. These statements address issues that involve risks, uncertainties, estimates and assumptions made by management, and actual results could differ materially from the results contemplated by these forward-looking statements. Factors that could have a material adverse effect on our operations and future prospects include, but are not limited to, changes in interest rates, general economic conditions, legislative and regulatory policies, and a variety of other matters. Other risk factors are detailed from time to time in our Securities and Exchange Commission filings. Readers should consider these risks and uncertainties in evaluating forward-looking statements and should not place undue reliance on such statements. We undertake no obligation to update these statements following the date of this press release.

F & M Bank Corp. Key Statistics

2021

2020

Q4

Q3

Q2

Q1

YTD

YTD

Net Income (000’s)

$

1,380

$

2,337

$

3,220

$

3,801

$

10,738

$

8,788

Net Income available to Common

$

1,379

$

2,272

$

3,154

$

3,736

$

10,541

$

8,525

Earnings per common share – basic

$

0.39

$

0.71

$

0.98

$

1.17

$

3.25

$

2.66

Earnings per common share – diluted

$

0.40

$

0.68

$

0.93

$

1.11

$

3.12

$

2.56

Return on Average Assets

0.46

%

0.81

%

1.22

%

1.56

%

0.98

%

0.92

%

Return on Average Equity

5.42

%

9.18

%

13.06

%

15.96

%

10.84

%

9.46

%

Dividend Payout Ratio excluding Special Dividend

66.67

%

36.62

%

26.53

%

22.22

%

32.00

%

39.10

%

Net Interest Margin

2.48

%

2.95

%

3.13

%

3.44

%

3.00

%

3.61

%

Yield on Average Earning Assets

3.15

%

3.35

%

3.56

%

3.92

%

3.41

%

4.27

%

Yield on Average Interest Bearing Liabilities

0.96

%

0.57

%

0.62

%

0.70

%

0.60

%

0.94

%

Net Interest Spread

2.19

%

2.78

%

2.94

%

3.22

%

2.81

%

3.33

%

Provision for Loan Losses (000’s)

$

(590

)

$

(235

)

$

(1,250

)

$

(725

)

$

(2,800

)

$

3,300

Net Charge-offs/(recoveries)

$

72

$

61

$

(272

)

$

45

$

(94

)

$

1,215

Net Charge-offs/(recoveries) as a % of Loans

0.04

%

0.04

%

-0.16

%

0.03

%

-0.01

%

0.18

%

Non-Performing Loans (000’s)

$

5,508

$

5,430

$

5,532

$

5,783

$

5,508

$

6,537

Non-Performing Loans to Total Assets

0.45

%

0.46

%

0.50

%

0.57

%

0.45

%

0.68

%

Non-Performing Assets (000’s)

$

5,508

$

5,430

$

5,532

$

5,783

$

5,508

$

6,537

Non-Performing Assets to Assets

0.45

%

0.46

%

0.50

%

0.57

%

0.45

%

0.68

%

Efficiency Ratio

82.13

%

75.99

%

76.07

%

68.00

%

75.44

%

67.51

%

The net interest margin is calculated by dividing tax equivalent net interest income by total average earning assets. Tax equivalent interest income is calculated by grossing up interest income for the amounts that are nontaxable (i.e. municipal securities and loan income) then subtracting interest expense. The tax rate utilized is 21%. The Company’s net interest margin is a common measure used by the financial service industry to determine how profitable earning assets are funded. Because the Company earns nontaxable interest income from municipal loans and securities, net interest income for the ratio is calculated on a tax equivalent basis as described above.

The efficiency ratio is not a measurement under accounting principles generally accepted in the United States. The efficiency ratio is a common measure used by the financial service industry to determine operating efficiency. It is calculated by dividing non-interest expense by the sum of tax equivalent net interest income and non-interest income excluding gains and losses on the investments portfolio and Other Real Estate Owned. The Company calculates this ratio in order to evaluate how efficiently it utilizes its operating structure to create income. An increase in the ratio from period to period indicates the Company is losing a greater percentage of its income to expenses.

F & M Bank Corp. Financial Highlights

For Twelve Months

Ended December 31,

Unaudited 2021

Audited 2020

INCOME STATEMENT

Interest and Dividend Income

$

35,576,485

$

36,792,403

Interest Expense

4,301,238

5,728,482

Net Interest Income

31,275,247

31,063,921

Non-Interest Income

11,828,813

12,190,916

Provision for Loan Losses

(2,800,000

)

3,300,000

Loss on sale of securities

524,772

–

Impairment of long lived assets

171,109

19,193

Other Non-Interest Expenses

33,147,451

29,938,920

Income Before Income Taxes

12,060,728

10,035,110

Provision for Income Taxes

1,323,015

1,141,742

Less Minority Interest (Income)/Loss

–

(105,193

)

Net Income

$

10,737,713

$

8,788,175

Dividend on preferred stock

196,344

262,642

Net Income available to common shareholders

$

10,541,369

$

8,525,533

Average Common Shares Outstanding

3,414,306

3,199,883

Net Income Per Common Share

3.09

2.66

Dividends Declared

1.04

1.04

Unaudited

December 31, 2021

Audited

December 31, 2020

BALANCE SHEET

Cash and Due from Banks

$

8,579,007

$

11,181,164

Interest Bearing Bank Deposits

2,874,772

1,243,519

Federal Funds Sold

76,667,000

65,983,000

Loans Held for Sale

4,886,534

58,753,055

Loans Held for Investment

662,421,694

661,328,888

Less Allowance for Loan Losses

(7,747,792

)

(10,474,960

)

Net Loans Held for Investment

654,673,903

650,853,928

Securities

413,216,778

117,897,486

Other Assets

58,443,571

61,018,331

Total Assets

$

1,219,341,565

$

966,930,483

Deposits

$

1,080,294,540

$

818,581,503

Long Term Debt

21,772,052

33,201,631

Other Liabilities

16,819,462

19,517,664

Total Liabilities

1,118,886,054

871,300,798

Preferred Stock

–

4,558,298

Common Equity

100,455,511

91,071,387

Stockholders’ Equity

100,455,511

95,629,685

Total Liabilities and Stockholders’ Equity

$

1,219,341,565

$

966,930,483

Book Value Per Common Share

$

29.42

$

28.43

Tangible Book Value Per Common Share

$

29.96

$

28.42

CONTACT:

Carrie Comer EVP/Chief Financial Officer

540-896-1705 or ccomer@fmbankva.com

https://www.fmbankva.com/wp-content/uploads/2021/03/Farmers-and-Merchants-Photos-7-26-2018-1006.jpg10671600Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2022-01-27 15:13:042022-09-28 15:25:07F & M Bank Corp. Announces Record Annual Earnings For 2021