Do you have a home renovation project on your to-do list?

Whether you are preparing your home for sale or looking to improve your existing space, renovation financing can help you modernize your kitchen, update your bathroom, add an extra bedroom, and more. Renovation loans can also be obtained when you purchase a home that needs fixing up.

Here in the Shenandoah Valley, local real estate markets are heating up. You may have more equity in your home than you realize. Whether you’re still in the dreaming phase or ready to hire a contractor, let’s explore what renovation loans are and the different types of financing you can obtain.

What are renovation loans?

There isn’t one type of home renovation or home improvement loan. We’ll explore the different options for renovation loans below; for now, all you need to know is that a home renovation loan is any type of financing used to renovate or improve your loan.

Why use a renovation loan?

There are many reasons to finance home renovations. Here are a few examples:

Take out a home renovation loan when you buy your house to make a fixer-upper livable.

It can be cheaper to finance an addition and other improvements to your existing home instead of covering the costs of selling it and buying a new one.

You may be able to sell your home quicker and for a higher price if you do a complete renovation first.

What can renovation loans be used for?

There is almost no limit to what your home renovation financing can be used for. From cosmetic improvements to essential repairs, here are some ideas:

Roof repairs

New siding

Updated windows

New flooring

Installing/updating heating and cooling systems

Solar panels and other energy improvements

Mold remediation/waterproofing

New kitchen or bathroom that would add value to the house

Addition to add square footage/another bedroom

Get rid of termites and other unwanted pests

Home Renovation Costs in the Shenandoah Valley

Overall, the cost of a general home renovation project in Staunton, VA ranges from a minimum of $8,249 to a max cost of $65,998 with an average of $37,123.

In Harrisonburg, the range is $8,850 to $70,807 and the average is $39,828.

Let’s look at average costs for specific types of renovation projects:

Kitchen Remodel

The average cost in Staunton is $20,686.

The average cost in Harrisonburg is $21,283.

Bathrooms

The average cost in Harrisonburg is $9,208.

The average cost in Staunton is $8,242.

Pool Installation

The average cost of inground pool installation is $8,192 in Harrisonburg and $7,242 in Staunton.

The Pros and Cons of Using Renovation Loans

As with any financing decision, there are both benefits and risks to taking on a renovation loan. Our experienced mortgage team can help you weigh the pros and cons of your own situation so you can find the best solution for your home renovation needs.

Pros

Structured payments

Begin your project right away

Home equity loans usually have fixed rates, meaning your monthly payment is likely to stay the same each month.

You can move any unused money from your loan to an interest-bearing account to earn interest.

Interest rates for HELOC are low–and usually lower than personal loans or credit cards.

The flexibility of choosing what renovation projects to use the loan for

Cons

If the market value of your home declines, you may end up owing more on your mortgage and home renovation loan than your house could theoretically sell for. However, this is less of a risk if you plan to stay in your home long-term.

A home equity loan is a secured loan against your house so if you stop making payments the bank can take possession of your house.

The process of applying for a home renovation loan can be as involved and lengthy as applying for a mortgage, depending on the type of financing you choose.

Renovation Loan Options

When it comes to renovation financing, homeowners have many options to choose from. For homeowners in the Shenandoah Valley, F&M Mortgage offers renovation loans with as little as 5% down payment. Are all loan options created equal? Here’s what you need to know:

Home Equity Lines of Credit (HELOC): For homeowners who have ongoing renovation projects. A HELOC is a revolving account that can be used, paid back, and used again. Must have enough equity in your home (the difference between its current market value and any mortgage balances you have).

Home Equity Loan: A term loan, usually with a fixed rate and predictable monthly payments. Best for homeowners who need to finance just one (bigger) renovation project and want to pay off what they owe over a long period of time. Must have enough equity in your home.

Personal Loans: A decent option for homeowners without enough equity to qualify a secured renovation loan. However, an unsecured personal loan will usually have a higher rate. Best for smaller, less expensive projects.

Credit Cards: We don’t recommend using credit cards to fund home renovation projects and purchases unless you can re-pay the amount owed within the same billing cycle.

Cash-Out Refinance: Replace your existing mortgage with a new loan and get up to 80% of your home’s market value back in cash. Recommended for home improvement projects that add value to your house, but can be used for anything, including non-renovation expenses like college tuition.

New Purchase Renovation/Improvement Loans

FHA 203k Rehab Loan: Requires only a 3.5% down payment and you can receive up to $35k for repairs and renovations. Minimum 640 credit score and available for first-time buyers or refinancing.

Fannie Mae HomeStyle Renovation Loan: A combination purchase and renovation loan that provides up to $25k for renovations and improvements.

Freddie Mac Renovation Mortgage: Provides permanent financing to replace Interim Construction Financing. Can be used for land purchases, site-built homes, and renovations/repairs to existing homes.

VA Renovation Loan: No down payment and no private mortgage insurance.

Virginia Laws and Regulations

Check with your local municipality regarding permitting requirements. Here are two statewide rules to keep in mind as well:

Must obtain a permit before starting most large home renovations, and the house must be inspected before obtaining a permit.

Must provide the state with building plans, contractor licenses, and other applicable documentation.

https://www.fmbankva.com/wp-content/uploads/2021/07/FM-Bank-Renovation-Loans-Blog-Images-6-ImagesD1-02.png298848Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2021-07-16 11:04:122024-03-21 13:36:53Guide to Home Renovation Loans in the Shenandoah Valley

If you’re reading this, you’re probably interested in modular homes. Maybe you already know you want to build one or you’re still in the information-gathering stage. Wherever you are in the process, we cover it all in this exhaustive guide. From the benefits of owning a modular home, to what the process looks like, how to obtain financing, and more–F&M Mortgage’s friendly team of knowledgeable advisors is here to help. Our company has a division dedicated to modular construction financing and we have extensive local experience helping Shenandoah Valley residents build modular homes.

In this article, you will also find answers to frequently asked questions from local advisors and builders. If you have additional questions as you read, give us a call!

Modular Home Benefits

Modular Homes offer endless new home designs and most factories will allow you to use your customized plans, which is why modular is a popular way to build a home.

According to the Washington Post, modular homes have many admirers, including top architects and celebrities like Robert Redford. Among everyday home buyers, time is one of the most attractive benefits of going modular. Because the modules are constructed in a factory, the entire process is shorter than traditional construction. Additionally, modular home factories aren’t subject to weather and labor-related delays. Here are some more modular home benefits:

Factory Construction: Modular is just another way to build your home! Individual modules are built in a factory and assembled on site. This could save time and money. It also means the interior of your home is not exposed to the elements, reducing the risks of mold and mildew. Site-built homes are built almost entirely outside on your lot or piece of land.

Permanent Foundation: Similar to site-built homes you can build your modular home on a basement or crawl space.

Endless Design Possibilities: Choose from your builder’s catalog of home plans, add modifications to suit your needs, or ask about your customized home plans.

Appearance:Your modular home doesn’t have to have a “generic,” rectangular or box look. Instead, you can choose from traditional architecture styles and models like Cape Cod, Ranch, Two-Story, Colonial, Victorian, and more.

Quality: Modular construction is subject to its own rules and building codes, which may often be stricter than site-built construction. You can expect the highest quality and safety standards. Your modular home will also be inspected during the construction and after assembly to ensure compliance with local codes and ordinances. It will then be inspected by a state building inspector.

Energy Efficient: Many articles about modular homes tout the environmentally friendly construction process, which results in less waste than site-built construction. That may not be your top priority, but you’ll appreciate the cost savings on utility bills that modular homes often deliver. Because they are built so solidly, they can be more energy efficient than older homes as well as new site-built construction.

Cost: Because the factory-built process is more streamlined, with labor and materials already supplied, you can usually avoid the surprise expenses that often accumulate with site-built construction.

Real Estate Value: Modular and site-built homes are indistinguishable in appearance and both hold their appraisal value. Of course, fluctuations in your local real estate market can drive values up or down, but the modular nature of your home won’t be a factor.

Financing: Obtaining a loan for your modular home is usually as easy as a site-built home or purchase of an existing home. What’s different about modular and what construction lenders like is the limited risk of the build. Since most of the work is done in the factory and inspected, less can happen during the construction period and build of the home. It is important that a lender has a history of providing construction loans since there are a few more moving pieces than a home already built on a lot or in a development. The difference in new construction and what some say end loan or purchase loan, is that you may buy the land, design and build your home using a construction loan before it is really financed into a traditional mortgage loan. F&M Mortgage makes it easy with our unique modular programs. Find the perfect spot, land or piece of property, pick your design or home style and start your construction loan today. We work with your builder to make the entire process as smooth as possible.

Costs

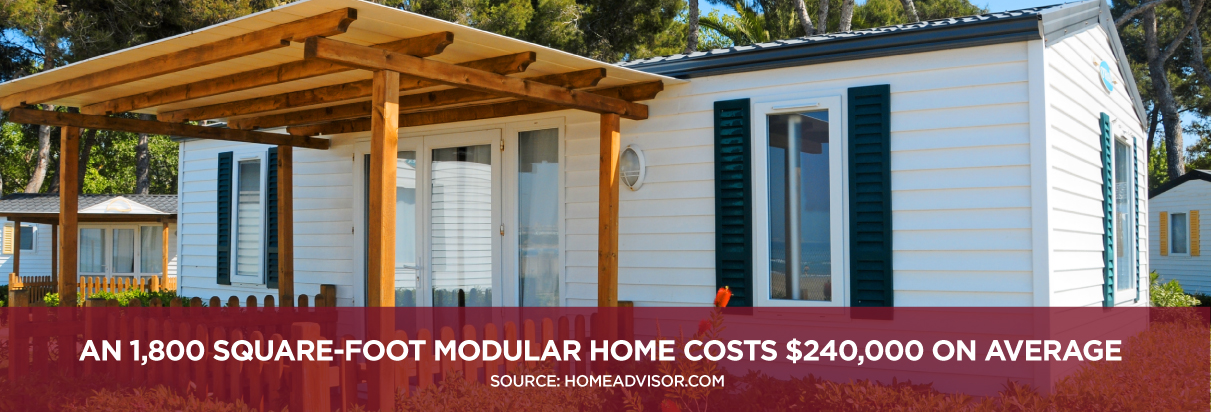

Of course, one of the biggest questions you’ll have when considering a modular home is how much it costs. According to HomeAdvisor, the national average is $240,000 for modular construction, with an overall range of $180,000-$360,000. You can enter your zip code and project details to get a more specific estimate. Harrisonburg-based Valley Homes offers free quotes when you know the style of your home, type of foundation, interest in adding a covered porch or deck, and garage. Here’s a complete list of factors that could contribute to the total cost of your modular home.

Land: As with new construction, you need to own the land or maybe you have land from family where your modular home will be assembled. If you don’t already have a lot or piece of land, you’ll need to buy one. According to a Zillow search of land for sale in the Harrisonburg area, most lots are priced between $100,000-$200,000.

Site Improvements and Permits: Your builder and his contractors build a contract of costs associated with the development of the land for the home. Not only are they licensed to do so they are up to date on building requirements locally.

Home Plan: The size of your home and the number of upgrades to the interior and exterior will factor into the total cost.

Process

Our guide to Building a Home in the Shenandoah Valley contains information that is also relevant to the modular construction and building process. For example, the section on finding a plot of land is the same, as well as some of the interior work (such as drywall) that happens after your modular home is assembled on site.

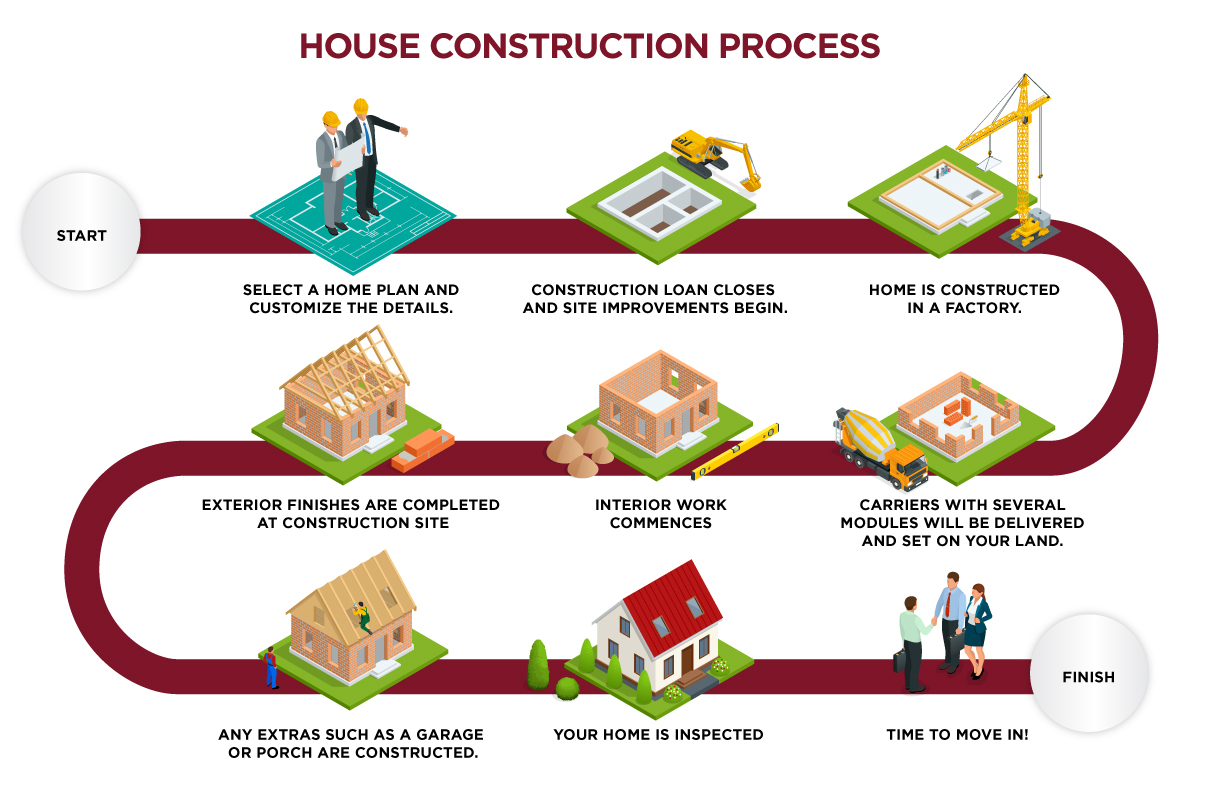

Overall, it takes about three-four months from contract signing to move-in readiness. Watch the entire process unfold, from floor plan to finished home, in this video from Valley Custom Homes. Use our checklist below to plan for each step on your calendar:

Talk to and get approved by a construction loan officer.

Find and hire your builder.

Find a piece of land.

Select a home plan and customize the details.

Sign a contract with your builder.

Construction Loan Closes and site improvements begin.

Home is constructed in a factory.

Portions of the loan, called draws, are disbursed to pay for work completed.

Carriers with several modules will be delivered and set on your land, where they are assembled.

Interior work commences: drywall, electricity, plumbing, and flooring.

Exterior finishes are finished or some are construction at site.

Any extras such as a garage or porch are constructed.

Final Draw is released to builder.

Your home is inspected and you are granted a certificate of occupancy.

Final Draw is released to the builder.

Time to move in!

Questions for an Advisor

What is the difference between construction loans and other home loans?

It’s an entirely different process and risk involved. Construction loans allow you to borrow money before the home is built and funding (draws) is disbursed on completed work to a builder during the construction process. Construction loans allow you to build and make the home yours, and it guarantees new with one owner. Other home loans allow you to borrow money to purchase existing homes.

Does my lot need to be paid off to apply for a construction loan?

A lot loan can be paid off as part of the construction loan. It is actually better to purchase the land at the same time you start your construction loan so you only carry one loan at one time and only have one construction closing. That said, if you do own the lot, construction loans should pay off the lot loan or remainder of what is borrowed at construction closing, to only have one loan.

When in the process is a down payment required for a construction loan?

Most lenders would prefer to have some “skin in the game”, so they will require down payment when the loan closes. If it is a construction to permanent loan, down payment is required at close of the construction loan and before construction begins.

At what point should I consider a construction loan during my home search?

At any point if you have or can find land.

How has the pandemic impacted construction lending?

Prices have increased and materials are more difficult to get. For other home loans, prices are up as well. It is a seller’s market.

What should I consider when deciding to hire a builder?

When a client is asking for specific options or features in the purchase of their new home, it is critical to have a contractor that documents changes and itemizes each particular activity required for the completion of the home. Of course, communication is key! Ask your builder if they utilize an online system to upload documents and facilitate communication. Many builders are adding all comments, documents, contracts, change orders, and the project timeline to an online portal for the client! As we move forward into the 2020s, builders having these available to their client are going to be critical.

What are my responsibilities during the construction process?

Make sure you give your builder as many documents (soil reports), plats, easements (electric, county water, utilities) and requirements (covenants) related to your land as possible. It’s important that we have all the info related to your property so that we can make sure we aren’t missing any details that may come up while building your home!

Do you recommend purchasing a house plan online or working directly with an architect?

I recommend doing what you feel most comfortable with! Most home sales are done directly online. However, with an architect, we can get some specific details down that may be overlooked when selling off of an online version.

Do all decisions need to be finalized before construction begins?

They certainly do not, but you should have 90% of what needs to be done figured out before the construction process begins. If you make too many changes during construction, it could result in a lot of out-of-pocket money for change orders!

On average, how long does the construction process take?

We try to start the foundation 30 days before the home is complete from the factory. After that, there aren’t too many complex items, and it typically takes around 90 days to finish. Of course, this is always contingent on weather, labor, and supply availability as well as building official requirements.

How has the pandemic impacted the construction process?

It has never been a better time to buy a home than today! Interest rates are at all-time lows, and it is hard to get much closer to 0%. The main impacts are time frames of supply. We often find ourselves making sure that certain materials are purchased well in advance because of the backlog, but homes across the commonwealth are going up every day!

Insights from Paul Sofia, Masterpiece Homes of the Carolinas

What should I consider when deciding to hire a builder?

Find out what is included in their pricing and ask about their experience. Address your concerns.

What are my responsibilities during the construction process?

Responsibility lies with the builder during the construction process. The buyer just needs to be patient because it is a process. Delays do happen, especially with weather.

Do you recommend purchasing a house plan online or working directly with an architect?

An architect is extremely expensive. There are thousands of plans online that a manufacturer can duplicate through their engineering department.

Do all decisions need to be finalized before construction begins?

Absolutely, especially when dealing with the agreed price! Changes can be made after the fact if both parties sign an addendum.

On average, how long does the construction process take?

Currently, depending on the manufacturer, 8-12 months.

How has the pandemic impacted the construction process?

Costs have increased as well as turn times.

Insights from Walter Cleaton

What should I consider when deciding to hire a builder?

You should always consider the amount of time a builder has been in construction. Is he licensed and insured to do the work needed? What can your local building official tell you about the builder? A reputable and licensed builder may not always be the cheapest, but should always provide the best work, craftsmanship and experience.

What are my responsibilities during the construction process?

You should take the time to review the home, the options, and all added amenities in person with your builder. Meet with your builder on site, to determine spacing and position of the home. As the buyer, be understanding of weather and unforeseen circumstances, that a builder cannot control. When asked, be prompt in your opinions, documentation, and decision making. Timely communication is the buyer’s greatest responsibility.

Do you recommend purchasing a house plan online or working directly with an architect?

Most plans online will be changed and altered at some point by the buyer. Not all plans online will or can be built to satisfy all codes in every state. If possible, you are usually better served by sitting down with a builder or architect to design your home. Everything done in person is usually better. Nothing beats eye to eye comparison.

Do all decisions need to be finalized before construction begins?

Any decision that can be made prior to construction, and especially a contract, is always better for all parties. Change orders can be discussed and made after construction begins, but if known in the beginning, it will usually save everyone time and money.

On average, how long does the construction process take?

All projects will vary in the time it takes to complete, depending on the size and details of the proposed construction. Weather and the availability of materials can and will play a huge role in the time it takes to complete a project. Basements vs foundations, single story vs two story, etc. Will always be a factor in the time to complete. There is no set time on any project to complete. A builder can only give an approximate timeline, or a worst-case scenario. There is not magical date or timeline that every home should be built or ready by.

How has the pandemic impacted the construction process?

The pandemic has greatly impacted the construction process. Shortages of materials and components, due to depleted work forces, has put the construction industry behind greatly. Companies losing workers due to quarantine has hit the labor force hard. Most construction materials and components have been impacted in some way. The original stockpile of these items have been depleted, and catching up or staying up with demand, with a depleted work force, has caused strain on the construction industry.

Additional Helpful Resources

Ready to start the process of finding a builder and designing your modular home? Here are some local resources.

F&M Mortgage: professional construction lending experts.

Protech Home Builder: A custom Modular Home Virginia builder that specializes in highly energy-efficient home at a great value at an affordable price.

Masterpiece Homes of the Carolinas: Provides both site-built homes and modular homes in Charlotte, NC.

Pats Manor Homes of Harrisonburg: Another local option for modular home construction.

ModCoachBlog: a great national resource with articles, updates and who’s who in the modular world of building.

Financing Options

F&M is your local partner in modular home financing. From purchasing a land lot to construction, and an eventual traditional mortgage, we can help you enjoy a smooth financing process from start to finish. Our Approved Builder Modular Construction Loan Program reduces your construction loan costs and qualified borrowers can take advantage of low down payment options. F&M is proud to be an approved lender for federally guaranteed loans such as FHA, VA, USDA, and VHDA. You may be able to use these home loans to finance part or all of your modular home costs. We also offer bridge loans for people who need to finance a new home purchase while waiting for their existing house to sell. Apply online or contact our lending team with any questions you have about modular home financing.

https://www.fmbankva.com/wp-content/uploads/2019/05/modular-home-guide.jpg2501210Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2021-05-10 13:48:572024-01-19 12:11:162021 Guide to Owning a Modular Home in the Shenandoah Valley

One of the most exciting times in your life can be moving into a new home. You have saved for your down payment and are ready to begin the decision-making process, but now you may have new questions arising. Should I be building or buying my house? How likely is it for me to find my ideal home in today’s housing market? Houses in the Shenandoah Valley tend to be available for only a short time before they are bought, so it can be difficult to find exactly what you are looking for. This guide will help outline the differences between building and buying your house, along with insights from experts on the F&M Mortgage team to help you find your dream home.

Buying a House in Virginia

Advantages of Buying a Home

Some home seekers may want to purchase a home that is already finished and ready to occupy due to their desired timeline for moving in. Buying an existing home can meet this need, along with other advantages. Buying an existing home opens the possibility for price negotiation, depending on the seller and overall market conditions.

Buying a home tends to be a straightforward process, typically requiring a standard mortgage. However, those looking to buy may learn that closing on an already built home in today’s market is not as easy as it may seem.

Disadvantages of Buying a Home

Buying a house is an important financial decision, so many home seekers may find themselves wanting to find their dream home on the market rather than settling for anything less. Compromising for other options may even impact your enthusiasm for moving entirely.

The residential real estate market in the Shenandoah Valley today moves quickly, with many homes being sold before buyers get the chance to plan and decide. Thankfully, building your new home is a viable option for those who are having trouble finding what they’re looking for on the market.

Building a House in Virginia

Advantages of Building your Home

When building your home, you have more flexibility and decision-making influence over the design of your house, down to the little details. This includes the floorplan, cabinets, and paint being aligned with your vision on the day you move in. Also, while those buying an existing house can often run into unexpected maintenance costs soon after they close, having a newly built home will afford you being under warranty for years to come. This includes new appliances, HVAC systems, and roofing. This can help put you at ease without having to worry about additional costs soon after making the financial decision of relocating in the first place.

Disadvantages of Building your Home

While building your home is a great alternative to those struggling to find the right existing home on the market today, it may not be the right fit for everyone. Depending on where you are moving from, you may need to be paying for two homes at once until you are able to sell your previous house. It is also important to consider where you will be living throughout the building process and the related expenses. Construction Loans have their differences among other types of mortgages, so we asked our lending team to provide their expertise below.

Ask An Expert!

Looking for answers to frequently asked questions about construction loans and the home building process? We reached out to contractors and our mortgage advisors to be your resource. You can review the following insights from our team to learn more:

How has the pandemic impacted the construction process?

We have been experiencing an extended lead time on materials due to manufacturing delays. Many plants have been forced to reduce capacity based on various state laws. When COVID hits a plant, they may even shut down for two weeks, all of this on top of increased demand. We have also seen price increases coming more frequently since the onset of the pandemic.

In the early stages of the pandemic, many homeowners started DIY projects like deck additions/replacements or outdoor playhouse construction. This led to a huge spike in pricing for pressure treated lumber. At the same time, the low housing inventory in the Shenandoah Valley drove an increase in new home construction. Some items have become hard to find, or the lead time is 4 times as long pre-COVID. Currently, this is the market condition with no real end in sight.

What should I consider when deciding to hire a builder?

I believe the most important part of deciding on a builder is relationship. It is the largest purchase most people will ever make, and building a home is an extensive process. The ability to converse openly without fear of embarrassment is critical. Start with doing your own research and finish with an interview.

What are my responsibilities during the construction process?

It starts with a complete understanding of the contract details and progresses to regular, onsite review with a particular focus at key milestones. For example, completion of framing, completion of rough-ins, and obviously final walkthrough inspection. Regularly review your contract documents.

Do you recommend purchasing a house plan online or working directly with an architect?

If you find a plan online from a reputable source that is perfect as drawn, it will be the less expensive route. If the plan you find online isn’t quite right, you are better off doing a design with an architect or builder that offers design build.

Do all decisions need to be finalized before construction begins?

No, BUT realize that changes often result in additional work and expense. The more you can finalize your selections for the original contract, the better. Do your homework by shopping and educating yourself about key concepts that will save money over the life of the home. For example, insulation levels above code requirements, SEER rating on heating/cooling equipment, hot water recirc with insulated pipes, gray water systems, etc.

On average, how long does the construction process take?

Pre-contract negotiation can easily be a month without design time, and the permit process is generally a month. From permitted to completion without changes can be at minimum a 23-week schedule.

What should I consider when deciding to hire a builder?

You should find a builder who builds to the level of quality that you expect. Different builders build to different quality levels. The best way to find a builder is by word of mouth. Ask your neighbors and friends for recommendations. You will find that one or two names are consistently mentioned. Also, keep in mind that the better builders are busy, so you should plan ahead to allow them to make time for your home in their schedule.

What are my responsibilities during the construction process?

Homeowners should try to make decisions in a timely manner to not impede progress. It is also important that the homeowner convey their vision and expectations to the contractor before the work is done.

Do you recommend purchasing a house plan online or working directly with an architect?

I recommend beginning the process by looking at plans online. This is less expensive provided you can find one that meets your needs and style. Your builder should be able to make minor changes to the plan. However, if you are unable to find a plan you like, you will need to have plans custom drawn by a local draftsperson.

Do all decisions need to be finalized before construction begins?

Major decisions should be finalized before construction begins. Items that a homeowner selects, such as floor coverings, light fixtures, etc., do not have to be final before construction begins, but those decisions need to be made in a timely manner to not delay the progress. Even with the goal of making all decisions upfront, it is realistic to expect that a few changes will occur along the way. Be sure you address how changes will be handled with the builder.

On average, how long does the construction process take?

Construction of a new home can take 7 to 9 months to complete.

What is the difference between construction loans and other home loans?

A construction loan is any loan that provides for turning raw land into a completed home. This term encompasses site-built homes as well as manufactured and modular homes. Your initial construction loan is an interest-only mortgage loan, whereby you make monthly payments of only interest, based on the amount that has been paid out to the builder at the time of billing. At completion of construction, F&M Mortgage will update the credit, income, and asset documents to refinance the interest-only mortgage into a final 30-year fixed mortgage.

On at traditional purchase loan, the home is ready for you to move in as soon as closing occurs. The processing and underwriting of construction or traditional purchase loans is the same.

Does my lot need to be paid off to apply for a construction loan?

Our construction loan can roll the payoff of the land loan (or the purchase of the land) into the construction loan closing. Any down payment made on the land is credited toward the down payment required on the construction loan, provided the value of the land itself exceeds the amount owed. Additional down payment requirements may apply, based on borrower qualification.

When in the process is a down payment required for a construction loan?

Down payment is due at or before closing on the construction loan, which occurs prior to any work beginning on the project.

At what point should I consider a construction loan during my home search?

You can investigate both construction and traditional purchase simultaneously as you are looking for your perfect home. The decision to go with construction over traditional purchase is a personal decision and is impacted by your timeline for getting from your current living situation into your new permanent home. I would recommend investigating both loan scenarios initially, so you can gather all the information you need to make informed decisions.

How has the pandemic impacted construction lending?

We have seen a significant increase in the cost of building materials, timelines for appraisals and title work, and factory backlogs for modular and manufactured homes due to increased demand and occasional labor shortages as a result of the pandemic. F&M Mortgage is committed to keeping you informed and providing proper expectations during the approval process. We work diligently to keep you moving forward as quickly as possible.

When in the process is a down payment required for a construction loan?

When the construction loan is closed, your down payment is required, unless the land has enough equity to be accounted for down payment.

At what point should I consider a construction loan during my home search?

When your realtor recommends that what you are looking for is not going to be available.

Contact F&M Mortgage

F&M Mortgage works with builders and home buyers directly to ensure a seamless and user-friendly construction loan process, helping you and your clients build dreams into reality. From Harrisonburg to Staunton and across Augusta, Page, Rockingham, and Shenandoah counties, F&M Mortgage and F&M Bank are your local home construction lenders, offering construction loans for as little as 5% down. Learn more or apply now for your new construction loan!

Flexible lending options from a team of local lenders familiar with your community make F&M Mortgage the ideal lender for your home loans. In-house decision making simplifies the process and competitive rates get you the most for your money. Get started now!

https://www.fmbankva.com/wp-content/uploads/2021/04/Stock-header.jpg295845Jacob Mowry/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgJacob Mowry2021-04-12 12:59:552021-04-12 12:59:55Building vs. Buying a Home in the Shenandoah Valley

Are you thinking of buying a home? If you’re a veteran or active military personnel, you may be eligible for a VA loan. And the great news is, for those who qualify, VA loans offer some of the most enticing and flexible benefits available. Whether you’ve been researching this mortgage option for months or you are just getting started, here are 6 facts about VA loans that you may not know.

1. VA loans allow veterans to buy a home with little or no money down

VA loans require no down payment, making it easier for veterans to become homeowners. Perhaps just as importantly, the VA limits what fees and costs veterans can pay at the time of closing (they will not pay an “underwriting” lender fee for example). For other allowable closing costs like title insurance or appraisal fees, the veteran homebuyer can ask the sellers to pay all of their closing costs totaling up to a maximum of 4 percent of the purchase price. This can even include things like prepaid taxes and insurance, collections, and judgments. – Choice One Mortgage

2. Closing costs for VA loans are lower compared to other mortgage types

As mentioned above, one of the biggest benefits of a VA loan is that the VA limits the amount veterans have to pay in closing costs. Some financial institutions even offer closing cost reductions for qualified applicants. – F&M Bank

3. You can still get a VA loan while serving overseas

One of the more interesting facts about VA loans is that military members serving overseas can grant power of attorney (POA) to a spouse or someone else to sign the loan documentation for them. There is a 60-day occupancy rule, but only a spouse can satisfy that. Otherwise, an extension of up to 12 months is granted to the borrower. – Park Place Finance

4. If you have full entitlement, you won’t have a home loan limit

If the veteran has full entitlement, there is technically no limit on the loan amount and there will be no down payment required. It is important to note that if you do not have full entitlement (either through compromise or another VA loan) then the “old school” rules apply and down payments will potentially be required based on the loan amount. – Jennifer Guidry

5. There are a variety of VA loan products available

From purchase, refinance, and home construction options to financing for manufactured homes (including singlewides), there are a wide variety of VA loan products to choose from. The VA even offers a streamlined refinance product (called an IRRRL), which provides a fast refinance from one VA loan to another, lowering monthly payments. Additionally, under this “IRRRL” program, some lenders do not require an appraisal, income, or credit check. – eLEND

https://www.fmbankva.com/wp-content/uploads/2021/02/Blue-House.jpg14402160Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2021-02-10 15:53:222023-05-04 10:26:296 Facts About VA Loans That You May Not Know

Before you can make the transition from renting to owning your home, you might need to have a substantial down payment, typically 5 to 20 percent of the home’s value. The American Bankers Association suggests the following tips to help save for it:

Develop a Budget & Timeline

Start by determining how much you’ll need for a down payment. Create a budget and calculate how much you can realistically save each month – that will help you gauge when you’ll be ready to transition from renter to homeowner.

Planning ahead, it’s a good idea to play with numbers and calculate what your estimated monthly payment might be. F&M Mortgage offers a Mortgage Loan Calculator that helps simplify the budgeting process.

Establish a Separate Savings Account

Set up a separate savings account exclusively for your down payment and make your monthly contributions automatic. By keeping this money separate, you’ll be less likely to tap into it when you’re tight on cash.

Shop Around to Reduce Major Monthly Expenses

It’s a good idea to check rates for your car insurance, renter’s insurance, health insurance, cable, Internet or cell phone plan. There may be deals or promotions available that allow you to save hundreds of dollars by adjusting your contracts.

Monitor Your Spending

With online banking, keeping an eye on your spending is easier than ever. Track where most of your discretionary income is going. Identify areas where you could cut back (e.g. nice meals out, vacations, etc.) and instead put that money into savings.

Look Into State and Local Home-Buying Programs

Many states, counties and local governments operate programs for first-time homebuyers. Some programs offer housing discounts, while others provide down payment loans or grants.

Eligible first-time homebuyers may qualify for one of the many low to no down payment loan options through VHDA. Additionally, ideal for first-time home buyers, and open to all qualified borrowers, F&M Mortgage offers a no-PMI mortgage without income limits. If you’re looking for a no down payment mortgage, F&M’s Spark Loan might be perfect for you.

Celebrate Savings Milestones

Saving enough for a down payment can be daunting. To avoid getting discouraged, break it up into smaller goals and reward yourself when you reach each one. If you need to save $30,000 total, consider treating yourself to a nice meal every $5,000 saved. This will help you stay motivated throughout the process.

Contact F&M Mortgage

Flexible lending options from a team of local lenders familiar with your community make F&M Mortgage the ideal lender for your home loans. In-house decision making simplifies the process and competitive rates get you the most for your money. Get started now!

https://www.fmbankva.com/wp-content/uploads/2020/06/iStock-588394696-scaled-e1591735944471.jpg12922560Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2020-06-09 17:07:112020-06-09 17:07:116 Tips for Saving for Your Down Payment

Homeownership is woven into the fabric of the American dream, but the process can seem daunting to first-time homebuyers. As your community bank and mortgage lender, F&M Bank and F&M Mortgage are here to help. In this comprehensive guide we break down everything you need to know about buying your first home in Virginia, from costs to mortgage loan options and the major steps in the process. If you have questions as you read, feel free to reach out to our friendly and experienced team of mortgage lenders. We’re here to help!

How Much Does It Cost To Buy and Own a Home In Virginia?

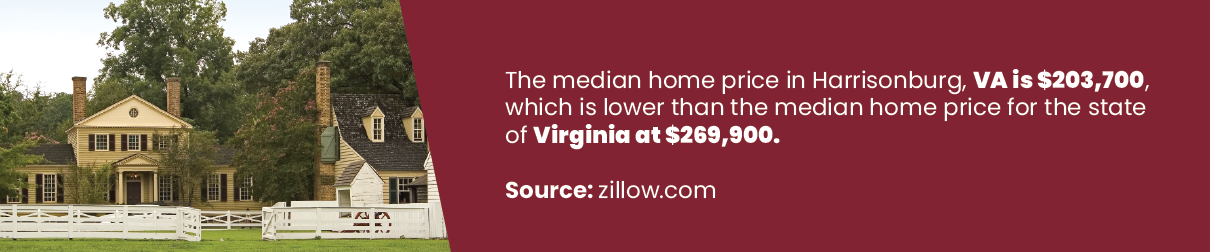

Real estate has always been a local business, and this is especially true in Virginia, where home costs vary widely depending on the region and metro area. Here in the Shenandoah Valley, the median home price for Harrisonburg is $203,700. Your down payment will depend on the type of home loan you apply for. At F&M Mortgage, we offer everything from no-down-payment mortgage loans to low-down-payment options and conventional mortgages with a 10-20 percent down payment. In general, the more you can put down, the lower your monthly payment will be. For most home loans, you’ll need to pay Private Mortgage Insurance premiums each month if you put less than 20 percent down. However, there are plenty of options for aspiring homeowners who can’t come up with a big down payment.

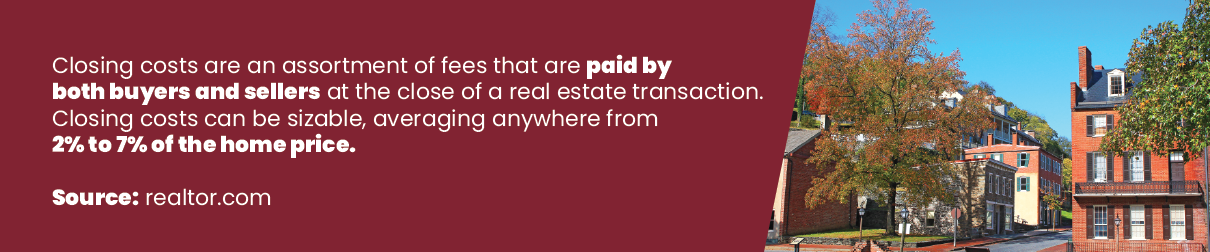

Closing costs are the second expense associated with buying a home. These vary as well, but in general, you can expect to pay between $4,000-$9,000. Your lender will share a breakdown of closing costs with you beforehand so you know how much you need. If you have concerns about coming up with both a down payment and closing costs, don’t worry. We’ll cover closing cost assistance programs below.

Once you’ve bought your home, your biggest expense will be your monthly mortgage payment, which encompasses the loan payment of principal and interest, as well as your property tax and home insurance premium. To continue with our Harrisonburg example, the real estate tax rate is .86 cents per hundred of assessed value. This works out to fairly low property taxes; for example, if you need to pay $1,253 in annual real estate taxes, this is only about an extra $100 each month added to your mortgage payment. Remember that the assessed value of your home is usually less than what you bought it for. When it comes to home insurance premiums, you can expect to pay about $35 per month per $100,000 of home value.

Now that you understand the basic costs of buying and owning a home, it may be more affordable than you thought. Let’s look at federal and state programs to help first-time buyers obtain home loans and down payment or closing cost assistance.

Federal Programs for First Time Buyers

Since 1934, when the Federal Housing Administration (FHA) was created to help Americans obtain home financing in the aftermath of the Great Depression, the federal government has launched a variety of initiatives to make homeownership more accessible.

Within the context of federal home loan programs, a first-time buyer doesn’t necessarily have to be someone who has never owned a home before. We’ll cover the eligibility requirements for each program below. As you’ll see when we get to Virginia programs for first-time buyers, there are instances where federal and state home loans and home buying assistance work in tandem.

FHA Loans This is the original federal home loan program and it is open to anyone who meets the eligibility requirements. An FHA mortgage is a great option if you’re looking for a low-down-payment home loan. Depending on your FICO credit score, you may qualify for the maximum 96.5 percent financing, meaning you’d only need to make a 3.5 percent down payment. For our $203,700 median home price, 3.5 percent would be $7,130. That’s much easier to save for than a full 20 percent down payment of $40,000.

FHA Loans and Mortgage Insurance FHA loans are great for homebuyers who can’t afford a larger down payment or whose credit score might disqualify them from obtaining a conventional loan. In return for this flexibility, FHA borrowers pay an upfront mortgage insurance premium of 1.75 percent of the loan amount. You’ll also pay an annual mortgage insurance premium of 0.45 percent to 1.05 percent, divided by 12 and paid each month as part of your mortgage payment. The FHA mortgage insurance premium is for the life of your loan unless you refinance into a conventional mortgage.

VA Loans Established in 1944 with the GI Bill of Rights, VA loans are available to current service members, veterans, and certain surviving spouses. The VA home loan program is very generous, with up to 100 percent financing, no mortgage insurance premiums, and low closing costs. The only added cost is a VA fee of 1.25 percent to 2.4 percent of the home’s value.

USDA Loans USDA mortgages fall under the US Department of Agriculture and are intended to encourage home purchases in rural and semi-rural areas. Depending on your credit score, you may not have to make a down payment on a USDA loan. USDA loan eligibility is also based on your household income, which can’t be more than 115 percent of the median income in your county. USDA borrowers must also first try and fail to obtain a conventional mortgage.

Benefits of a USDA Loan

No or low down payment

Flexible credit approval

Some suburban areas count as “semi-rural”

HUD’s Good Neighbor Next Door Program If you are a law enforcement officer, primary school teacher, firefighter, or EMT, you may be eligible to purchase a single-family home in a designated revitalization area at a 50 percent discount off the list price. As long as you live in the property for at least three years, you won’t have to pay back the 50 percent discount. You can also sell the house for its full market value and keep the profit. Search for current listings here.

Fannie Mae HomeReady Designed for creditworthy low-income borrowers, the HomeReady mortgage permits down payments as low as 3 percent. Also, your down payment and closing cost money can come from a variety of sources, including grants. There is no minimum requirement for personal funds. And while you’ll need to pay for Private Mortgage Insurance (PMI), you can cancel it once you have at least 20 percent equity in the home.

Freddie Mac Home Possible Loan Like the HomeReady mortgage, the Freddie Mac Home Possible Loan offers a down payment as low as 3 percent. You also have flexibility with the sources of your down payment and closing cost funds. Home Possible borrowers can even have a co-borrower on the loan who doesn’t live in the same residence. Overall, the Home Possible mortgage is great for self-employed individuals as well as those working in the gig economy.

Virginia-Specific Programs for First Time Home Buyers

The Virginia Housing Development Authority (VHDA) offers 30-year fixed-rate mortgages, forgivable down payment grants, and federal tax breaks to first-time homebuyers in the state. In this case, the first-time buyer simply means that you haven’t owned part or all of another house in the past three years.

VHDA loans come with income and purchase price limits that are set by county. To qualify, you need a minimum 620 credit score, must be willing to make the house your primary residence and have to finish a homeownership education course first.

VHDA Fannie Mae HFA Preferred No MI This mortgage loan offers a low down payment of 3 percent and there is no mortgage insurance requirement. You can also use a VHDA Down Payment Assistance grant and Mortgage Credit Certificate to reduce the cash you need to pay upfront.

“The VHDA has struck a special deal with Fannie Mae with this program, which is designed for first-time and repeat homebuyers with a credit score of at least 640. Down payment requirements start at just 3 percent. The affordable monthly payment and discounted upfront cost is great, but it’s the insurance benefit that really shines.”

VHDA FHA Plus Loan If you’re interested in a standard FHA loan, but don’t have enough cash for the down payment, the VHDA FHA Plus Loan might be the best option for you. Obtain up to 100 percent financing with a second mortgage that covers your upfront closing costs and down payment. County income limits apply and the combined loan total cannot exceed VHDA’s home price limits.

VHDA Rural Housing Services (RHS) This is the VHDA’s version of a USDA mortgage. If you wish to buy a single-family house in a qualified area, you can take advantage of 100 percent financing, low mortgage insurance premiums, and a discount on your federal tax bill.

VHDA Down Payment Assistance Grant This grant can be used in combination with a variety of mortgage loans. Get up to 2.5 percent of your home’s value to put toward your down payment. Qualified home buyers don’t have to repay the down payment assistance grant.

VHDA Mortgage Credit Certificate If you qualify for the VHDA’s down payment assistance grant, you can also file for the Mortgage Credit Certificate, which lets you claim 20 percent of your annual mortgage interest as a federal tax credit for the life of the loan.

From Pre-Qualification to Closing: Understanding the Homebuying Process

One of the most important decisions you’ll make at the beginning of this process is finding the best lender. You want to look for local expertise, a long history of mortgage lending, and friendly service. This will help ensure a smooth and timely mortgage and home buying process. As a local lender serving the Shenandoah Valley, F&M Mortgage has been helping first-time buyers become homeowners since 1999. We offer a complete suite of conventional, VHDA, VA, USDA, FHA, and zero-down-payment Spark Loans.

Get pre-qualified for a home loan. Pre-qualification letters carry more weight with sellers than pre-approvals. They demonstrate the seriousness of your intentions and vouch for your ability to get a mortgage.

Find a buyer’s agent to help in your home search.As with mortgage lenders, we recommend looking for someone with experience in the local real estate market and a specialization in working with buyers.

Fall in love with a house and make an offer. Once your offer is accepted, you will be “under contract” with the seller. Your mortgage lender will appraise the house and work through the underwriting process. You may be asked to provide additional documentation during this stage.

Get a home inspection. While this isn’t a requirement, it’s highly recommended. Paying for a home inspection will give you a complete and thorough report on the condition of just about everything in your house. If repairs are needed, you can renegotiate the purchase price with the seller.

Go to closing. The entire process can take anywhere from 4-6 weeks between the contract and the closing. Once the big day arrives, you can expect to sign a lot of paperwork and walk away with the keys to your new home. Congratulations!

Learn more about buying a home in the Shenandoah Valley!

https://www.fmbankva.com/wp-content/uploads/2019/12/FM-Bank-Blog-Images-First-Time-Home-Buyers-Guide-for-Virginia-01-02.png298848Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2019-12-23 10:52:122025-06-17 08:41:05First Time Home Buyers Guide For Virginia

Are you a veteran, service member, or surviving spouse? Perhaps you’ve heard that the VA can help you get a mortgage loan, but you’re not sure where to start. As a longtime community bank serving the residents and military veterans of the Shenandoah Valley, F&M Bank created this education guide to VA Loans to help you understand what they are, how to apply, and what the process looks like. You can also visit our VA Mortgage Loans page.

What is a VA Loan?

The VA Home Loan Benefit offers eligible homebuyers more favorable terms on a mortgage from a bank or other private lender. You must use your VA loan for a primary residence. The VA guarantees a portion of the loan against loss.

There are 3 types of VA-guaranteed home loans:

Purchase Loan: Helps you buy a new home at competitive interest rates.

Streamline Refinance: Obtain a lower interest rate.

Cash-Out Refinance: Access your home equity to pay off debt or finance a major expense like college or home renovations.

Who is Eligible?

To be eligible for a VA loan, you must meet credit and income requirements and receive a Certificate of Eligibility (COE). Eligibility extends to servicemembers and veterans, spouses, and certain beneficiaries. Browse the list below to see if you might qualify:

Veterans of WWII and the Korean or Vietnam Wars.

Gulf War service

Service during peacetime

Separated from service (other than dishonorable discharge)

Active-duty service personnel

Selected Reserve or National Guard

Un-remarried spouses of veterans who died while in service or from a service-connected disability.

Spouses of missing in action or prisoner of war servicemembers

Surviving spouses who receive Dependency and Indemnity Compensation (DIC) benefits.

Certain U.S. citizens who served in the armed forces of a government allied with the U.S. during WWII.

Service members of certain organizations, such as Public Health Service officers, cadets at the U.S. Military, Air Force, or Coast Guard Academy, midshipmen at the U.S. Naval Academy, officers of National Oceanic & Atmospheric Administration, merchant seaman with World War II service, and others.

The VA Home Loan program is designed to help eligible veterans and service members achieve the dream of homeownership. With an experienced VA loan lender like F&M Bank, you can move through the process in a smooth and efficient manner. Here are the primary benefits of applying for a VA loan:

You don’t need to make a down payment unless:

The lender requires it.

The purchase price is greater than the property’s appraised value.

Unlike other mortgages with less than 20 percent down, Private Mortgage Insurance (PMI) is not required for a VA Loan.

Rates may be lower.

Limited closing costs

You can use a seller’s assist (when the seller pays some or all of the closing costs).

There are no penalty fees for paying the loan off early.

If you have trouble making loan payments, the VA may be able to help.

You don’t have to be a first-time home buyer to qualify for a VA Loan.

The VA Loan benefit can be re-used (more on that later).

VA-guaranteed home loans are assumable.

Disabled veterans are exempt from the one-time VA funding fee.

What does the process look like?

Here’s what you can expect to do during the VA loan application process.

Determine your eligibility.

Apply for a Certificate of Eligibility (COE) through the eBenefits portal. Your lender can also request a COE for you.

Select a VA-approved lender to originate your VA home loan.

Review the loan origination fee, if applicable. Some lenders charge a one percent flat fee to cover the costs associated with your VA loan, such as the appraisal and inspection, recording fees, your credit report, prepaid items, hazard insurance, flood zone determination, survey, title examination and insurance, special mailing fees, VA funding fee, and the Mortgage Electronic Registration System.

Consider how you will cover closing costs. As mentioned above, you can submit an offer on a home that has the seller paying the closing costs.

Take a home buyer education workshop. This isn’t a mandatory step, but it can be very helpful, especially for first-time homeowners. Here in Virginia, the Department of Housing and Community Development facilitates free events and webinars.

Find a real estate agent to act as a buyer’s agent for you and start the home browsing process. If you need recommendations, our friendly and Shenandoah Valley-based employees can help you find local real estate agencies to work with.

Once you find a house you love and make an offer, be sure to include a “VA Option Clause” in your contract (which your real estate agent will draw up for you). This contingency, along with clauses for the VA appraisal and home inspection, protects you against contractual obligation in the event that your VA financing doesn’t come through.

If the VA-appraised value is not enough to cover the purchase price of the home, you can request a Reconsideration of Value (ROV), try to renegotiate the sale price, or pay the difference at closing with your own funds.

The process ends with closing, where you sign the loan and title paperwork and collect the keys to your new home. Congratulations!

Where can you get a VA loan in the Shenandoah Valley?

To obtain a VA loan in the Shenandoah Valley (or anywhere else in the country), you must find a lender that is approved by the U.S. Department of Veterans Affairs to originate VA mortgages. Of course, that only narrows your options somewhat. Ultimately, you want to choose a VA-approved lender with extensive VA loan experience in Virginia.

For example, F&M Mortgage has been offering full-service home mortgages to the Shenandoah Valley and beyond since 1999. With offices in Woodstock, Harrisonburg and Staunton, Va., our Mortgage Advisors also have expertise with other government-insured loan programs like FHA. We can help you evaluate all of your options to ensure the VA loan is the best fit. Then we’ll put our experience to work for you to get you to closing as soon as possible.

VA Loan Limits in the Shenandoah Valley by County

VA loan limits reflect the maximum qualified veterans with full entitlement can borrow without making a downpayment. Limits vary by county due to varied real estate markets. You can view the complete list of counties and loan limits. Below, we’ve listed the loan limits for each Shenandoah Valley county we serve.

Rockingham County: $484,350

Shenandoah County: $484,350

Page County: $484,350

Augusta County: $484,350

City of Harrisonburg: $484,350

City of Staunton: $484,350

Closing Cost Assistance for VA Loans in Virginia

In 2018, the Virginia Housing Development Authority (VHDA) launched its Closing Cost Assistance (CCA) Grant program. Receive up to 2 percent of either the purchase price or appraised value (whichever is less) of your home. The CCA grant is for first mortgage loans only and must be used for closing costs, including the VA Funding fee. Talk to your lender about reserving grant funds for your VA mortgage loan.

How does the VA Loan Compare to Other Home Loan Types?

No down payment: Only VA and USDA loans offer 100 percent financing. You may be able to make a low down payment on a conventional mortgage, FHA loan, or VHDA loan, but you will pay private mortgage insurance (PMI) until you have 20 percent equity in your home (FHA loans require mortgage insurance for the life of the loan).

No mortgage insurance requirement: As mentioned above, FHA borrowers will pay mortgage insurance through the life of the loan. Conventional borrowers must pay it until they reach 20 percent equity. Even USDA loans have (albeit low) mortgage insurance. Only the VA loan waives the PMI requirement for borrowers.

Conforming Loan Limits: VA loans have the same limits as other types of mortgages. The conforming loan limit is set by Fanny Mae/Freddie Mac. If you want to borrow more you’d need a jumbo loan.

Home Inspection: Government-backed loans like the VA and FHA programs have quality standards that a home must meet to qualify for financing. With conventional mortgages, a home inspection is not required by the lender. However, it is always recommended that buyers schedule a private home inspection before closing to uncover any potential issues.

Appraisal: Lenders always appraise the home before approving a mortgage. This is true regardless of the loan program you choose. It is usually difficult or impossible to borrow more than a house’s appraised value.

What can VA Loans be used for?

VA Home Loans can be used for purchasing a primary residence, purchasing and making improvements to an existing house, financing the construction of a new home, or refinancing an existing loan. Eligible properties and uses include:

Existing single-family homes and condominiums

New construction

Simultaneously purchase and improve

Refinance an existing non-VA loan

Refinance an existing VA loan to reduce the interest rate

Manufactured homes and lots

Energy-efficient improvements

VA loans cannot be used to purchase an investment property, finance a business, buy farmland without a residence, buy property abroad, or purchase a vacation home. Recreational vehicles (RVs) and boats are also ineligible.

Surviving spouses who remarry before age 57, as well as divorced spouses, lose their VA loan eligibility.

Restoration of Entitlement

You can use your VA loan benefit again as long as your prior VA loan has been paid in full (and the property sold). You can re-use your benefit just once if you pay off your first VA loan but do not sell the associated home. You can also find a qualified Veteran-transferee to buy your home and assume your VA loan by substituting their entitlement for yours.

F&M Mortgage is your local VA loan lender in the Shenandoah Valley

F&M Mortgage, a division of F&M Bank, has been helping Virginia’s military veterans and their families become homeowners since the VA home loan program was introduced. Our Mortgage Advisors pride themselves on offering friendly, personalized service with local expertise.

Ready to apply for a VA loan? Use our online mortgage application or apply in person at your nearest F&M Bank office. We have locations across the Valley, including dedicated mortgage offices in Harrisonburg, Staunton, and Woodstock, VA. Have questions about choosing the right mortgage loan for you? Give us a call today!

Check out our Loans for Local Heroes Home Loan Program, which provides up to $500 off your closing costs, and visit our VA Mortgage Loans page.

https://www.fmbankva.com/wp-content/uploads/2019/09/va-loan-guide.png4231210Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2019-09-03 11:04:342023-03-13 11:20:02A Comprehensive Guide to VA Loans

Who are the best mortgage lenders? This article will help you choose, but the answer ultimately depends on your particular circumstances and preferences. While tech savvy consumers may have no qualms about working with an online-only lender, other people prefer the kind of personalized service only a lender with physical locations can offer. Of course, here at F&M Bank, we have a lot to say about small bank vs big bank mortgages. We also break down the differences between online mortgage lenders vs banks, cover mortgage broker vs bank pros and cons, and provide the rest of the information you need to make an informed choice.

Digital Mortgage Lenders and Brokers: What are the Pros and Cons?

If you’ve done any mortgage research online, chances are you’ve seen ads for one or more “mortgage tech” companies, digital lenders and brokers that claim to provide the same services as their “bricks and mortar” forebears but with greater efficiency, speed, and customer service.

The biggest strength of these non-bank digital lenders is their technological innovation. Instead of faxing, mailing, or hand-delivering the required paperwork, you can complete the entire process online, perhaps even through a mobile app. Some borrowers may find this approach more convenient, and digital lenders also claim to offer faster processing times.

However, technology has its downsides, as Wells Fargo’s latest scandal demonstrates. If a “computer glitch” can lead to foreclosure, what else can go wrong? Also, you’ll want to read the fine print carefully and shop around before committing to an online mortgage lender. They aren’t always cheaper than traditional lenders – some digital loan companies have higher-than-average lending rates. And while they may bend over backward to provide superior customer service during the application process, you don’t know who will ultimately end up servicing your loan. It’s entirely possible to end up with a loan servicer who doesn’t have cutting-edge technology or great customer service. Then you’re stuck with that company until you sell your home or refinance the loan.

Additionally, a mortgage loan is a bigger investment and a more complicated process than applying for a personal loan online, for example. The “efficiency” promised by online lenders can translate to an impersonal approach with multiple points of contact and a lack of familiarity with local rules and regulations. You may find yourself, after it’s too late, wishing for a local office you could step into with a friendly loan officer to speak to in person.

Mortgage Brokers and Direct Lenders

If you’re already working with a buyer’s agent for your home search, you’ve probably been referred to the realtor’s “preferred lender.” This usually ends up being a non-bank, direct lending mortgage company. You can also seek out a private mortgage broker who, like an insurance broker, will shop around for you to find the best home loan for your situation. However, in exchange for outsourcing the comparisons you could do on your own, you’ll usually pay an extra fee or fees. If you’re wondering, should I use a mortgage broker or go direct to a bank or private lender, here are the pros and cons of brokers and non-bank lenders.

The main benefit of working with a private mortgage company or mortgage broker is their singular focus on home loans. Since mortgage loans are all they do, they may have additional expertise. And unlike their digital counterparts, private mortgage lending companies and brokers will usually offer a dedicated point-of-contact and physical locations you can visit for in-person help. Depending on the company, you may be able to find some of the same technological convenience that online lenders offer.

On the other hand, you still don’t know who will end up servicing your loan and what kind of customer service or technology they will have. You may also find higher rates and/or fees if you choose a private company or broker. Conflicts of interest can arise with brokers who work on commission from lenders or mortgage companies affiliated with the realtor, who may be more motivated to close the deal than to look out purely for your best interests. While some private mortgage companies have a regional focus, many are national chains that may lack the same local expertise as community bank lenders.

Megabanks

Most people are aware that national banks offer mortgage loans–in fact they might be the first thing you think of when you ask yourself, where do I go for a mortgage loan? That’s why Wells Fargo and Bank of America are the second and third largest mortgage lenders in the country. However, we’re all familiar with the dark side of being so big. Overall, the main benefit of working with a national bank on your mortgage loan is the infrastructure: 24/7 customer service support, online applications and other tech innovation, a potentially larger selection of loan programs and products. If you are a “cookie cutter” home buyer, meaning you have good credit and a standard employment history, you’re likely to have a smooth experience obtaining a mortgage from a megabank.

However, megabanks are a lot less flexible with people who are self-employed or whose credit isn’t perfect. Since they are already so big, they have little incentive to work with someone outside that cookie cutter shape they’re looking for. Megabanks often have higher fees as well, and you’ll find the same kind of impersonal service as with a digital lender: long hold times to speak to someone on the phone, fluctuating contact points, and possibly longer processing times. Even if you’re happy with their service, you’ll probably find that your loan is quickly sold or transferred to another lender, whose service you may or may not like. Finally, unlike with community banks and credit unions, megabanks’ profits flow back to Wall Street instead of your local economy.

Local Banks

Last but not least we have local banks, which are often overlooked but actually an excellent choice for your mortgage lender. Borrowers may worry that their community bank can’t provide the same 24/7 customer service or technology as national brands, but those assumptions aren’t always true. Many local banks offer online mortgage applications, for example, and extended hours for customer support by phone. You may also be able to contact your loan officer quickly via email or their personal cell phone number. This is the level of personalized service that community banks typically offer.

Instead of being bounced around from person to person, you can depend on a consistent point of contact who knows you and will work with you through the entire process. This makes applying for a mortgage less stressful–after all, you are making a purchase that is likely the biggest of your life, so a friendly voice and familiar face can go a long way in easing your nerves. Local banks also typically provide a faster response time due to their local decision-making. They also frequently service the loan after closing, so you won’t experience the unpleasant situation of having your mortgage sold or transferred to a lender you didn’t choose and don’t know.

Local banks can also compete with megabanks in terms of selection. In addition to specialized or local homebuying programs they may offer, community banks give you access to the same set of major loan programs including FHA, VA, etc. They are also much more willing to work with, and offer flexibility to, “nontraditional” borrowers such as the self-employed and those with an imperfect credit history.

Discover The Local Bank Difference

If you’re considering buying a home in Harrisonburg, Staunton, or elsewhere in the Shenandoah Valley, talk with a trusted local lender who has been helping people buy homes since 1908. Learn more about the different types of mortgage loans F&M offers and start your application online or give us a call to start the process with one of our friendly loan officers.

https://www.fmbankva.com/wp-content/uploads/2018/09/lenderspost.jpg284750Holly Thorne/wp-content/themes/fmbank-enfold-child/images/FandMBank_whitelogo.svgHolly Thorne2018-09-25 20:40:002023-06-16 12:43:26How To Choose A Mortgage Lender: Community Banks vs Big Banks vs Brokers vs Digital Lenders

Buying a home is one of the biggest decisions a person or couple can make. As a realtor, clients trust you to guide them through this important process. While potential buyers focus on the appearance of the kitchen, or whether there are enough bedrooms for the kids they hope to have, you work behind the scenes to crunch numbers and make sure the necessary paperwork is completed on time. Your clients may not care to read every word, but it’s your responsibility to make sure they understand all aspects of the closing paperwork, including title insurance. Here at F&M, we care about local communities and we know that the state of the housing market is an important part of a town’s overall vibrancy. We created this guide to title insurance to support realtors and home buyers in the Shenandoah Valley. We hope it helps you make an informed decision about title insurance policies.

What exactly is title insurance?

Most homebuyers, even repeat ones, have heard of title insurance but don’t really know what it is. They may think it’s just another requirement that adds to their closing costs without providing any tangible benefits. This view is common but decidedly wrong. The truth is, homeowners are lucky if their title insurance never comes in handy, but they could get into a lot of trouble without it. Simply put, title insurance guarantees that the seller is legally within their rights to sell the home to the buyer. Therefore, title insurance policies protect mortgage lenders and home buyers from ending up with a defective title.

3 Types of Potential Title Issues

If you’re wondering what a defective title looks like, we’re not referring to water damage or any other kind of printing/paper damage. Title issues are past events that affect ownership of the house and are not as readily apparent to buyers as, say, outdated bathroom tile.

Lien: a public record that money–as in unpaid taxes, a mortgage loan, or contractors’ fees–is owed on the house. If these creditors are not paid at the time of the closing, the buyer will be responsible for any remaining liens.

Encumbrance: A right to the property that decreases its value. A lien could also be classified as encumbrance, as well as local restrictions and easements.

Defect: Any other type of error or complication, such as a person besides the seller who has a legal claim to the property.

Distinguishing Title Insurance From Other Insurance Policies

Sometimes the most helpful approach to understanding something is to distinguish it from other, more familiar items. There are three important differences between title insurance and other insurance policies:

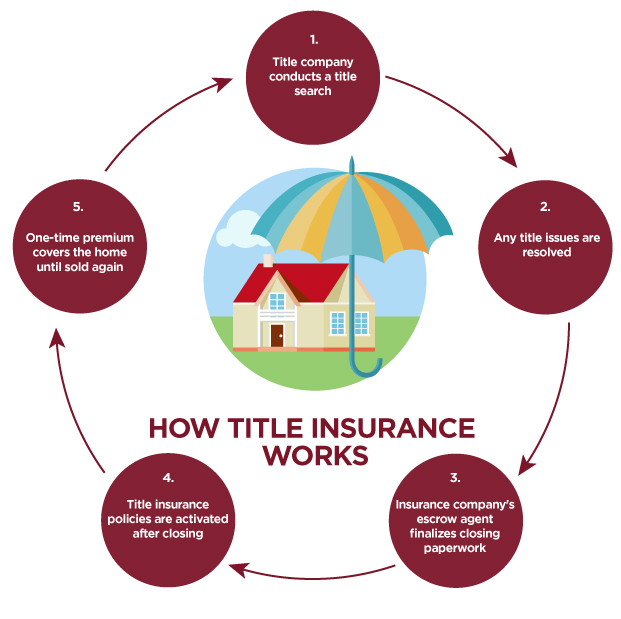

Payment schedule: With automobile policies and other types of insurance, you make regular premium payments as long as you’re insured. But with title insurance, you only pay once (at closing) and are protected for as long as you or your heirs own the property.

Responsibilities of the insurance company: When you sign up for car, health, or life insurance, the company asks you for basic information and provides a quote on a specific policy. That is the extent of your interaction with the insurance company, until you need to use the policy. With title insurance, the company fulfills most of their responsibilities upfront. They don’t just give you a piece of paper describing the benefits you’re entitled to, but take an active role in your closing process, from conducting a research-intensive title search to serving as an escrow agent and preparing essential paperwork.

Past vs future events: Most of the time, people buy insurance policies to protect themselves from things that haven’t happened yet, but could occur at any time, such as car accidents and major illnesses. Title insurance protects you against what has already happened, such as a contractor putting a lien on the property for unpaid work. As part of your title insurance policy, you’ll receive a report of any title issues before closing, and your policy will protect your equity in the home against future legal and other costs stemming from title issues.

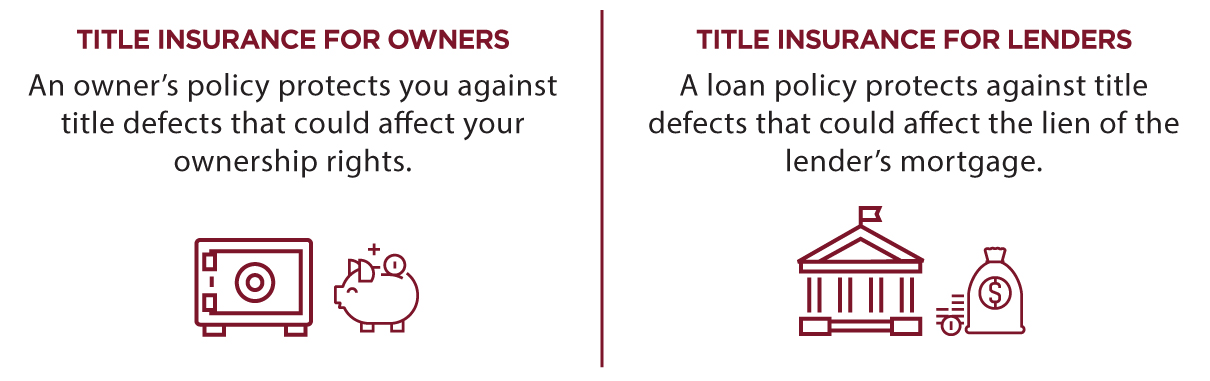

What are the two types of title insurance?

Title insurance for lenders: Covers mortgage lenders’ legal fees if the title fails or if the priority of their lien is different than expected. Usually a buyer must pay for lender’s title insurance in order to get a mortgage.

Title insurance for owners: Covers legal fees and costs of clearing a defective title if the owner’s legal right to the house is challenged.

Because owner’s title insurance is optional, some people may ask why they should pay for it. It’s tempting to cut a little bit off the total closing costs, but forgoing title insurance could end up being a major headache, both financially and otherwise.

Even new construction should be covered by an owner’s title insurance policy.

If your client is buying a new home (see our home building guide for Shenandoah Valley) , they may especially question the value of title insurance. However, while the house is new, the land could be subject to liens. And even a new home could have a lien on it from an unpaid subcontractor. The bottom line is that owner’s title insurance is an essential protection for every home purchase.

How much does title insurance cost and who pays for it?

The price of a lender’s policy is based on the amount of the loan. Owner’s policies are calculated from the purchase price of the house. There are different policy levels to choose from, so read the coverage details carefully to make the best choice. Some companies may offer a discount if both policies are purchased at the same time. In Virginia, the home buyer typically pays for both title insurance policies. It may be possible to include a credit from the seller in your contract.

Your realtor or mortgage lender will probably refer you to the title insurance company they usually work with. That doesn’t mean you have to work with them, however. You can (and should) shop around for the best quote and policy, just as you would with other purchases. Virginia’s Bureau of Insurance provides a database of licensed insurance companies.

How Title Insurance Works